Why Are Stocks Struggling Even as Oil Falls Amid US-Iran Talks?

Why Are Stocks Struggling Even as Oil Falls Amid US-Iran Talks?

By:Ilya Spivak

Crude oil is tumbling as the US-Iran war winds down, yet stocks can’t rally, bonds keep sliding, and the dollar is breaking out. Has the inflation story outgrown the war that started it?

- Crude fell to its lowest since the war began in March, but equities stalled near their highs instead of cheering

- Bonds slid and the US dollar punched through a year-long range, both pointing to higher-for-longer rates

- A heavy week of data — PMIs, GDP, and the Fed’s favored inflation gauge — may confirm that tightening is imminent

Markets have heard that the war is ending. They do not seem to care. The bellwether S&P 500 climbed back above 7600, near the highs it set before June’s meltdown, then stalled and began to consolidate — the makings of a possible double top rather than a launchpad for new gains. The striking part is what it shrugged off to do it.

Oil is falling, and it isn’t helping

The stall comes on the same fading volume and negative momentum divergence on the relative strength index (RSI) that preceded the last breakdown, hinting the rally is running out of steam. And it is happening even as crude oil breaks down through its wartime range to the lowest since the conflict began in March — unambiguous evidence that the geopolitical risk premium is draining out of prices. If the war scare were what ailed stocks, this should be a green light to push upward. Apparently, it is not.

Markets beyond equities tell the same story. Gold kept sliding, brushing off headlines about an open Strait of Hormuz that might have lifted it. Treasury bonds were turned back from the top of their range and resumed the steady stair-step lower that has defined them since the war began. The US dollar went further still, punching through the top of the range that had contained it for the better part of a year and accelerating the uptrend it has built since April. Every one of these moves speaks to the rising cost of credit, and every one of them persisted while oil, the original trigger, went the other way.

The inflation story has outgrown the war

For months the market’s anxiety ran in a straight line: the war spiked crude, crude fed inflation expectations, which in turn meant that the Federal Reserve could not satisfy traders’ hopes for rate cuts. With oil now retreating and the higher-rates trade barreling on regardless, the inflation story has seemingly taken on a life of its own. That is because the deeper driver was never just the oil price. It is the lopsided shape of growth itself.

Recent data has shown the energy shock seeping beyond fuel into core inflation, and into stickier service-sector costs in particular — visible in both consumer and producer price readings. But underneath sits a more durable problem: growth is increasingly powered by manufacturing and capital investment, the economy’s smaller engines, while the larger service sector and the consumers that power it fade. Forcing lesser output engines to spin faster to offset sluggishness from greater ones churns money at high velocity, which is inherently inflationary. That price impulse that owes nothing to the Strait of Hormuz.

A week of data built to confirm it

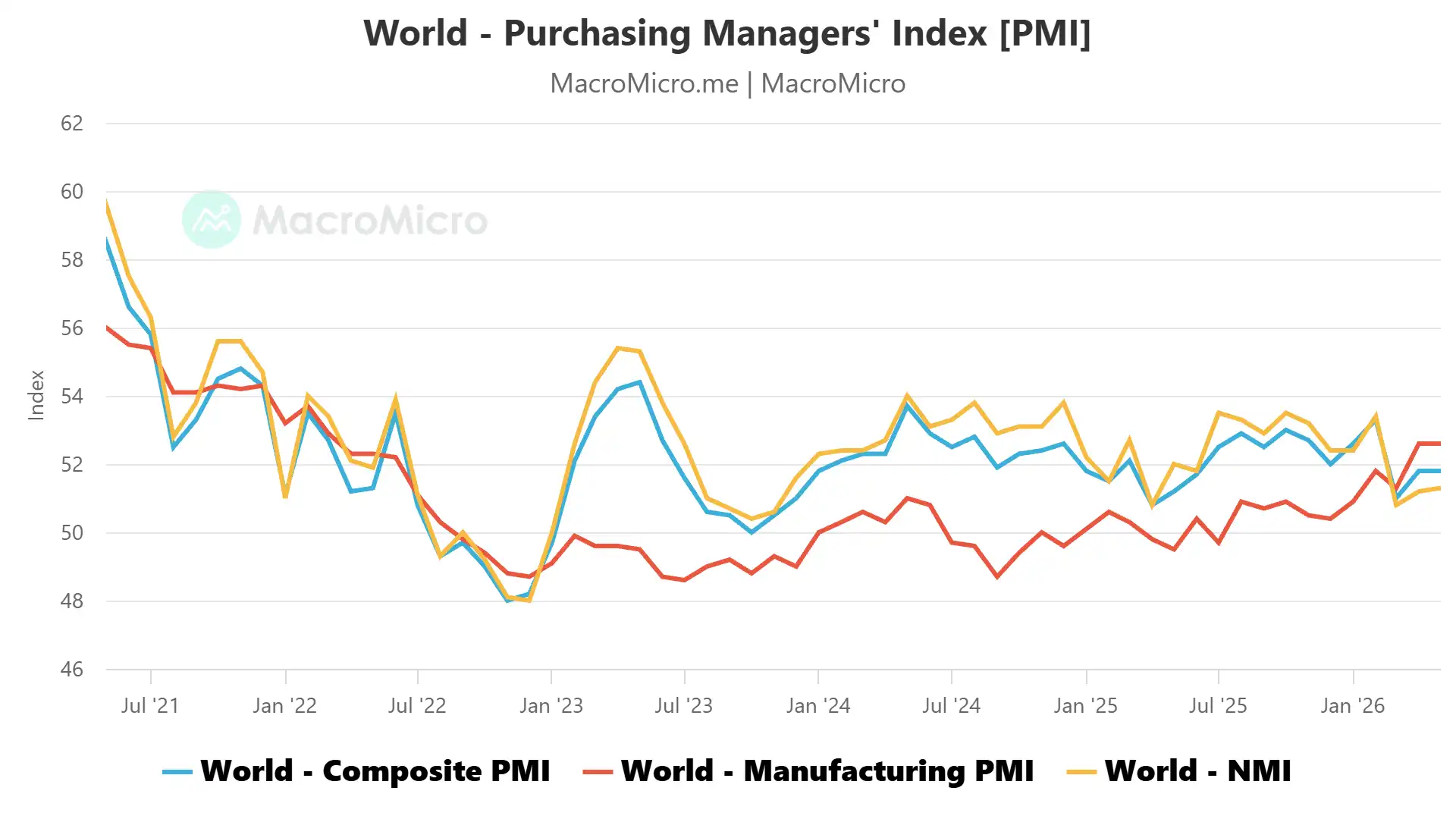

This week’s calendar should sharpen the picture. The June S&P Global flash purchasing managers indexes (PMIs) lead off, with the US figures front and center. The most recent global survey already captured the pattern: the service sector slowed to its weakest in about 11 months while manufacturing, long stuck in contraction, is now growing faster than the overall economy — and that lopsided mix produced the most aggressive jump in input and output prices in three years. The same arrangement shows up across Australia, the eurozone, and the UK, where manufacturing has held up but service-sector activity is either stalling or shrinking.

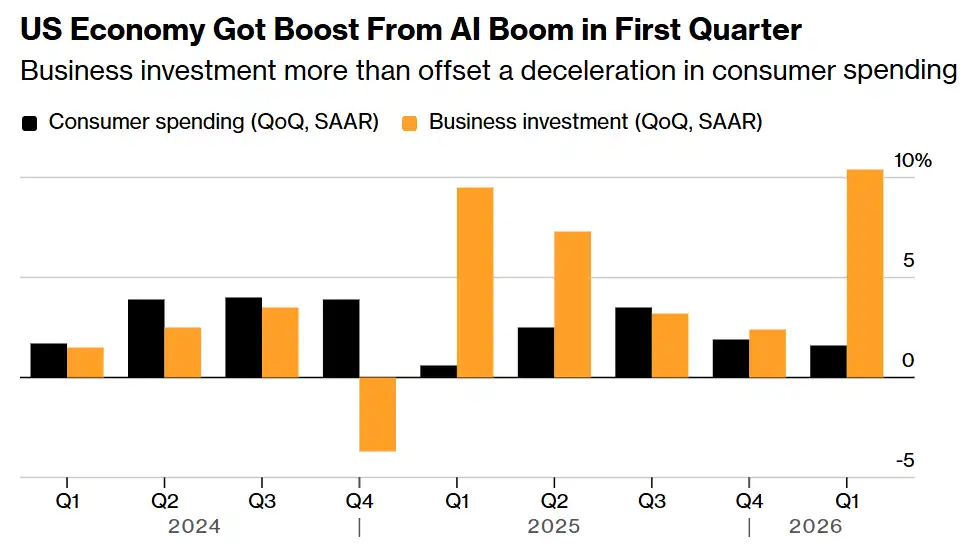

The US – where the artificial intelligence (AI) data center buildout is booming even as consumers retrench – is a loud case in point. This week brings the final revision of first-quarter gross domestic product (GDP) data, expected to confirm growth of 1.6% — a rebound from the 0.5% government-shutdown quarter, but barely halfway back to the roughly 4% pace of last year’s middle quarters. It arrives with the personal consumption expenditures (PCE) price index, the Fed’s preferred inflation gauge, seen climbing to 4% year-on-year, the highest since May 2023.

Why the Fed won’t blink

That fragile growth mix has driven inflation beyond the lingering scars of the wartime energy shock. It helps explain last week’s hawkish turn at the Federal Reserve. First-quarter GDP grew only because business investment — about 14% of the economy — expanded at a scorching 10.4% annualized clip and out-contributed consumption, which is 68% of output and decelerated for a second straight quarter. New Fed chair Kevin Warsh, nominated as a supposed dovish convert, instead delivered a terse statement, scrapped forward guidance, and repeated one line without fail: the Fed will deliver price stability. With inflation set to print near 4% against a 2% target, that is not a pledge that leaves room to ease.

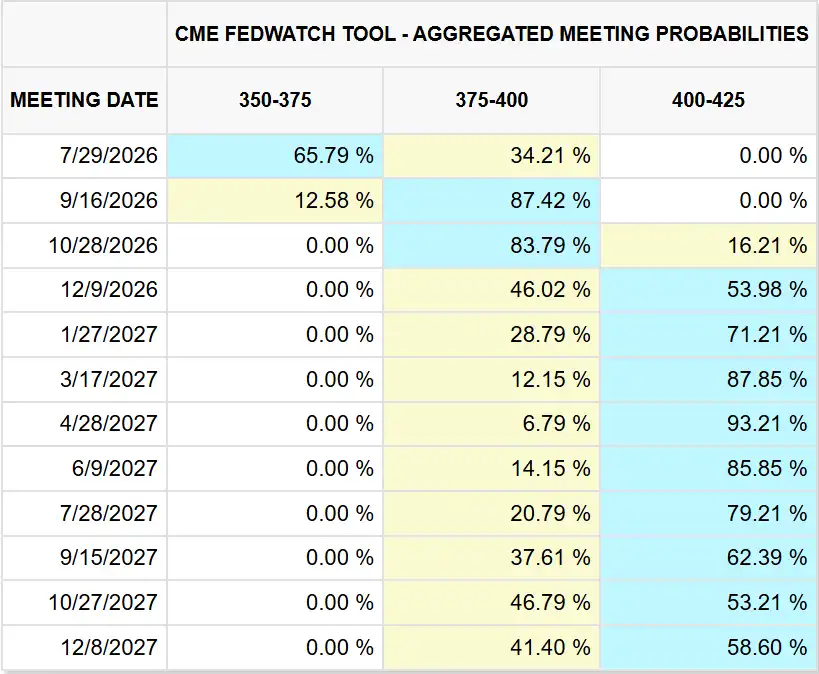

Markets have taken the message. Fed funds futures price one rate hike this year as a near-certainty, with roughly even odds of a second. On a cumulative basis, the probability of at least one hike reaches 87.4% by September, with a second more likely than not by December. The path runs one way — toward tightening — and oil’s retreat is doing nothing to divert it. So as the week’s data rolls in, the question is not really what is happening in the Strait of Hormuz. It is whether anything can pull the Fed off a tightening path while the economy overheats beneath a placid surface. If the answer keeps coming back no, the relief that carried stocks to the top of the range will have nothing left to feed on, making the current moment across markets precarious indeed.

Ilya Spivak, tastylive Head of Global Macro, has over 15 years of experience in trading strategy. He specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices