Macro Week Ahead: Will Stocks Get a Helping Hand from Central Banks?

Macro Week Ahead: Will Stocks Get a Helping Hand from Central Banks?

By:Ilya Spivak

The S&P 500 and Nasdaq 100 have recovered nearly 65% of the losses they suffered since mid-February

- U.S. stock markets are rebounding, but bonds and the dollar still wobble.

- PMI data boils down to a U.S. slowdown, threatening global growth.

- Interest rate moves at the Federal Reserve and Bank of England are now in focus.

Stock markets continued to recover last week. The bellwether S&P 500 rose 2.9% while the tech-tilted Nasdaq 100 added 3.4%. Both benchmarks have now recovered nearly 65% of the losses suffered since mid-February, the last time either one traded in close proximity to major highs. Gold prices fell back 1.7%, echoing a calmer mood across markets.

However, the bond market wobbled with interest rates creeping higher across the Treasury yield curve. The 10-year rate ticked up 1.3% while the two-year advanced 1.8%. The U.S. dollar continued to struggle, slipping 0.7% against the euro. It managed a narrow rise against the yen, but the Bank of Japan (BOJ) was at work as it cast doubt on rate hike plans.

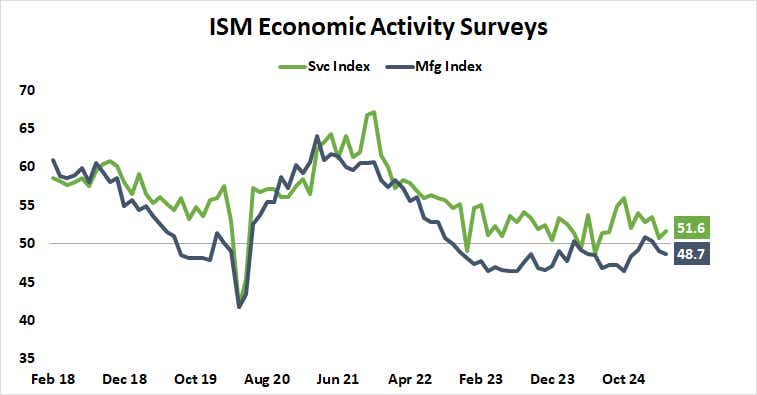

PMI data says the U.S. economy is slowing

U.S. economic data has painted a somewhat confounding picture as the new week gets underway. Competing purchasing managers’ index (PMI) data from S&P Global (SPGI) and the Institute of Supply Management (ISM) offered somewhat different perspectives on the state of the service sector, the most important engine of U.S. growth.

SPGI suggested growth of economic activity ground to near-standstill in April—the weakest performance since September 2023—as services expanded at the slowest pace in 17 months. A forward sentiment gauge fell to its lowest in 2.5 years and prices rose. The bottom line is “a heightened risk of … stagflation,” the report concluded.

The ISM version of the figures was a bit rosier, at least at the headline. It showed service sector activity picked up a bit in April after posting its weakest reading in nine months in March. A look under the surface offered a less forgiving view, however. Employment shrank for a second month straight as prices rose at the fastest rate in 26 months.

Will central banks ride to the rescue?

Last week, manufacturing PMI updates diverged in the opposite direction: The SPGI version reflected weak but positive growth in April, while ISM said activity contracted for a second consecutive month and at the fastest pace since November 2024. On balance, both data providers reveal a U.S. economy that has worryingly slowed this year.

That’s a glaring problem for global growth, which has relied on the U.S. to offset anemic performances in Europe and China since the middle of last year.

Against this backdrop, all eyes turn to monetary policy announcements from the Federal Reserve and the Bank of England (BOE) amid hope for a monetary uplift.

For its part, the U.S. central bank is widely expected to sit on its hands this month as it waits for “hard data” to show it whether to prioritize employment or inflation. The markets price in 69 basis points (bps) in cuts this year, implying at least two standard 25bps reductions and a 24% probability of a third one. The first move is expected to appear in July.

Across the Atlantic, the BOE is penciled in for a 25bps cut. That is slated to be the first of four cuts that markets have priced in for 2025. If markets walk away from these announcements with the sense that policymakers have not dialed up their sense of urgency even as growth trends turn more ominous, stocks may decline as bonds rise in “risk-off” trade.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices