Iran War and Markets: A Trade Hiding in Plain Sight?

Iran War and Markets: A Trade Hiding in Plain Sight?

By:Ilya Spivak

Away from the jumpy price action in stocks and bonds amid the US-Iran war, a trade may be hiding in plain sight.

- Stocks and bonds struggle to rebound as Iran war fears persist

- The markets expect a forceful central bank response to inflation

- The US dollar may rise as traders rethink hawkish policy pivot

The hopeful mood on display across financial markets at the start of the trading week seems to have fizzled. US stock markets traded mostly weaker, though the small-cap Russell 2000 managed a narrow rise while the tech-tilted Nasdaq 100 and the catch-all S&P 500 finished the day in the red.

Treasury bonds turned lower right on cue, with the parallel rise in yields helping to arrest a slide in the US dollar. Up to that point, the markets appeared to be replaying the now-familiar “Iran war = inflation = higher rates” dynamic in play for most of the month.

Gold prices pointedly decoupled however, shrugging off early intraday losses to finish the session with modest gains. That snapped a nine-day losing streak, the longest since October 2023 and only the third such run in 30 years. Crude oil – the would-be vector for transmitting the impact of events in Iran into asset prices – was curiously noncommittal.

Markets think rate hikes are ahead as inflation jumps. Really?

On one hand, this echoes what price action has telegraphed since last week: an inflationary shock is now on autopilot, whatever oil prices do next in the near term. On the other, it beckons a closer look at where the markets have landed after all of the fast-and-furious repricing of expectations since the Iran war began.

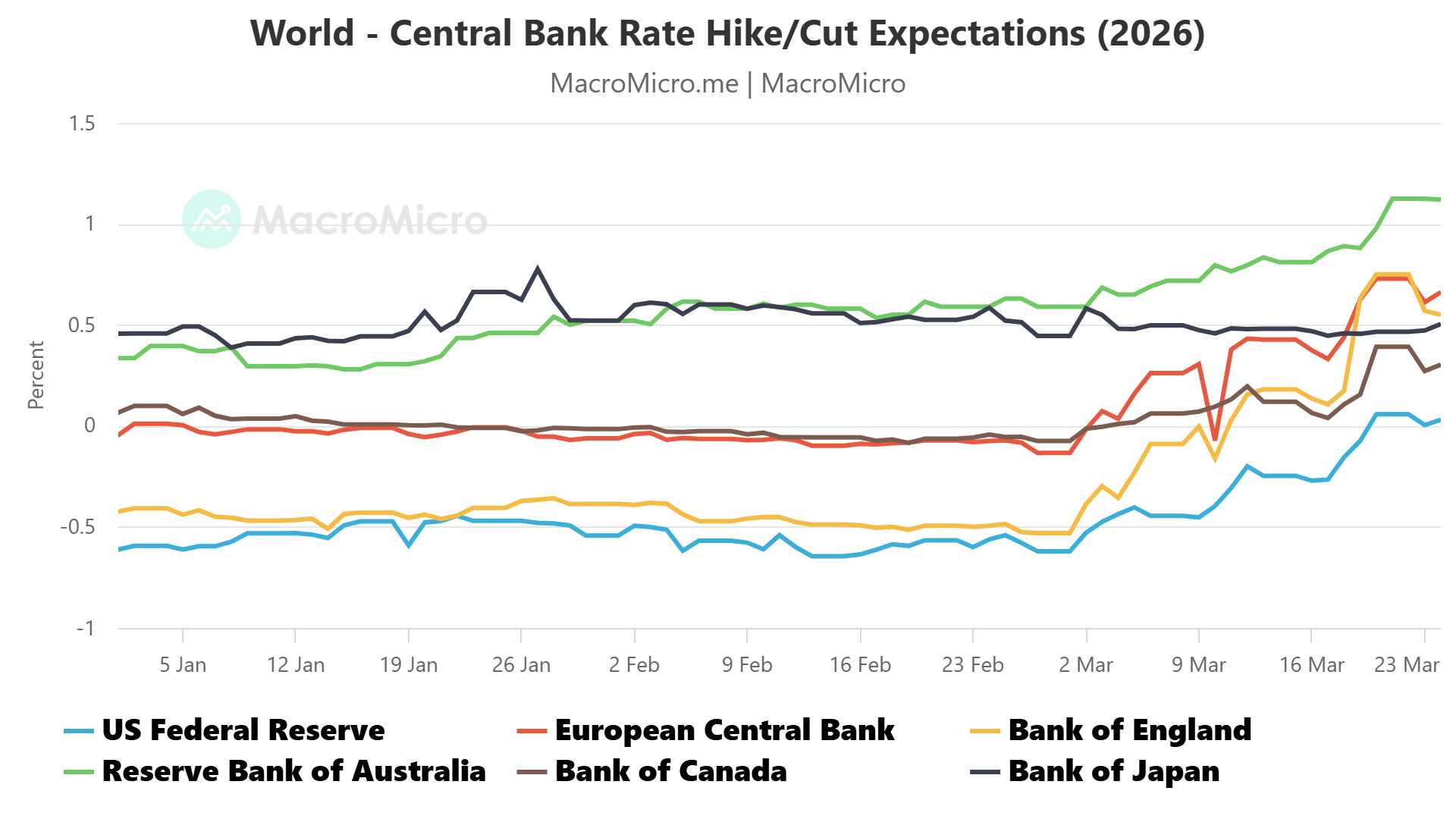

A striking new vision of global monetary policy has appeared. Traders have abandoned hopes for rate cuts from the Federal Reserve this year. Meanwhile, the European Central Bank (ECB) is seen hiking rates by 50-75 basis points (bps), having been set for a year at standstill just three weeks ago.

Similar changes have appeared for most major central banks. Year-end policy expectations priced into futures markets for the Bank of Canada (BOC), the Reserve Bank of Australia (RBA), and the Bank of England (BOE) have swung in a more hawkish direction by 30bps, 50bps, and 125bps respectively.

At face value, this might feel like it makes sense. The markets’ response to the Iran war has focused on its inflationary risks. Central bankers would surely be reluctant to cut rates against such a backdrop, lest they allow backsliding on their efforts to bring prices to heel after the Covid-19 pandemic.

Is the US dollar too cheap?

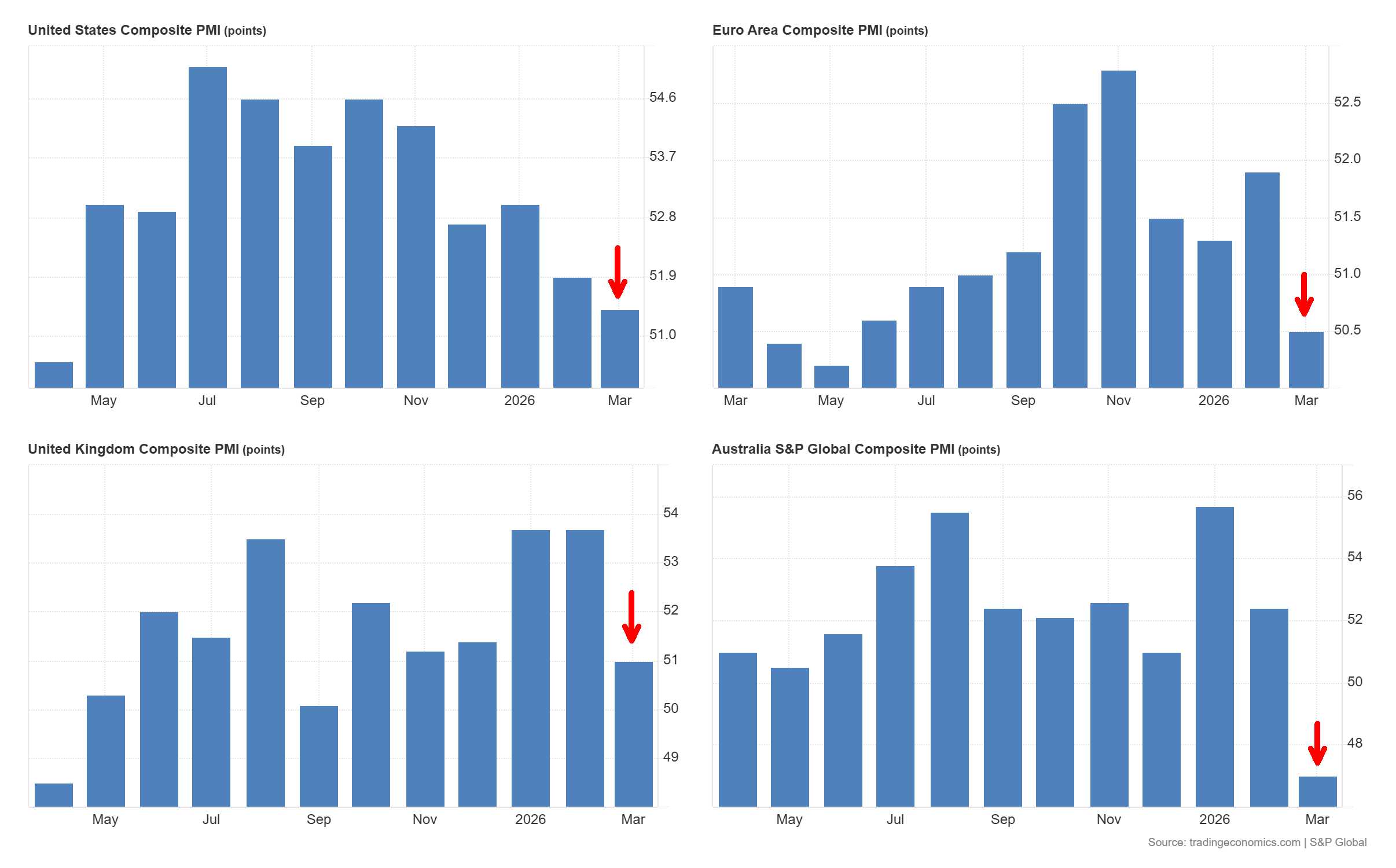

That makes the pivot in the markets’ outlook for the Fed appear sensible, at least for now. However, rate hikes from the likes of the ECB and the BOE seem implausible after the March edition of purchasing managers index (PMI) data from S&P Global revealed a sharp slowdown in economic activity growth in both the Eurozone and the UK.

“Cost push” inflation is the kind that comes from a sudden rise in the cost of some key input for economic activity, like energy. “Demand pull” inflation is the sort that accompanies rapid economic growth, where the supply of goods and services is struggling to keep up with voracious spending.

Interest rate hikes are the textbook response to the latter problem, but the Iran war presents policymakers with the former one. Slamming the brakes on a fragile Eurozone economy with rate hikes may well trigger recession, and so the ECB is unlikely to do it. Today’s inflation risk may paralyze central banks rather than turn them hawkish.

The US dollar may find a potent reason to trade higher if the markets come to the same conclusion. The currency’s present level implies a policy outlook that puts it at a disadvantage of between 25bps and 100bps against its top counterparts. If those gaps narrow as markets rethink the feasibility of rate hikes, a tailwind for the greenback will emerge.

Ilya Spivak, tastylive head of global macro, has over 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices