Macro Week Ahead: Are Stock Markets Really as Strong as They Seem?

Macro Week Ahead: Are Stock Markets Really as Strong as They Seem?

By:Ilya Spivak

Stock markets are charging to record highs, but tech earnings and central bank hawks may reality-check the rally.

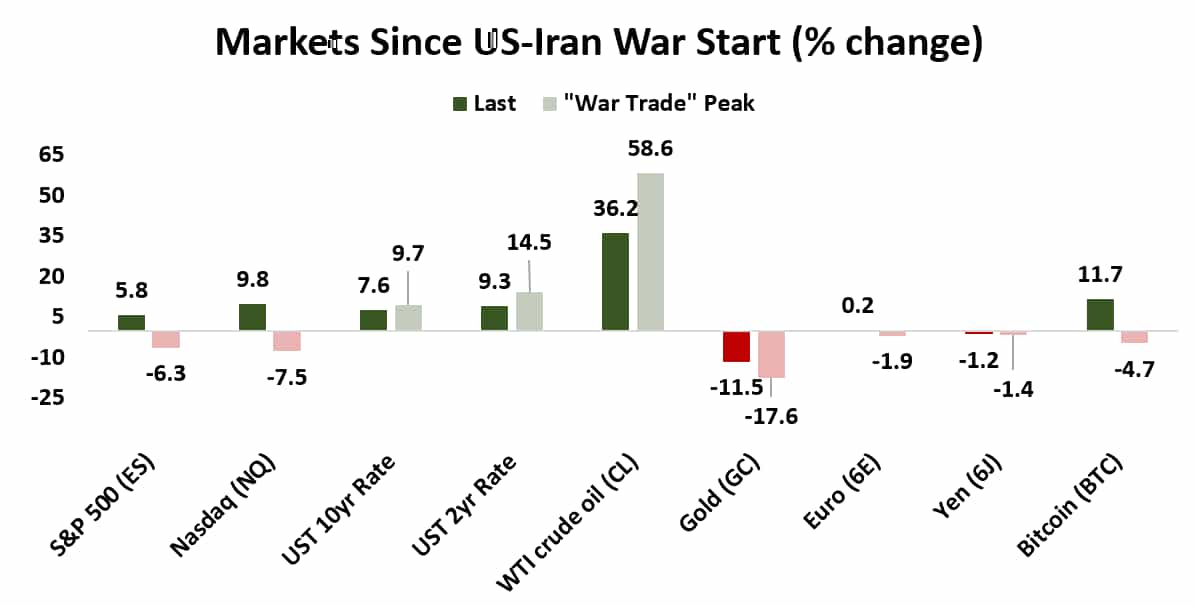

- Wall Street has erased its entire US-Iran wartime selloff, and then some

- Blended S&P 500 earnings look strong but PMI data hides warning signs

- Central banks from the Fed to the ECB face high-stakes rate decisions

Wall Street is pushing to record highs as earnings season gets underway in earnest, with traders seemingly content to treat the Iran war as old news. However, most other markets did not get the memo. A week of marquee tech earnings and back-to-back central bank decisions will put both narratives to the test.

Stocks are rallying but conviction may be fading

The S&P 500 is tracking up just over 4.5% since the US first struck Iran in late February, having been down as much as 6.3% during the fighting. The Nasdaq 100 has done even better. At face value, Wall Street has moved on.

Look under the surface and the picture is less convincing. Volumes have trended lower throughout the wartime rebound. They’ve started with is week at their lowest since the Easter Monday lull.

The relative strength index (RSI) momentum indicator is flashing a negative divergence: price is setting higher highs while the momentum reading is not. The capacity for prices to close higher relative to lower is fading even as new nominal records are set. That is not always a precursor to a reversal, but it often is.

Gold, oil, and bonds are still fighting the war

Crude oil remains more than 35% above pre-war levels, near the middle of its wartime range. Treasury bond prices have resumed sliding after a brief recovery, sending yields creeping higher again. The 10-year breakeven inflation rate has hit its highest since September 2025, erasing the disinflation narrative that defined the fourth quarter.

Gold is drifting lower as rising yields make non-interest-bearing assets less attractive. The US dollar has retraced only about half its wartime gains. Outside of stocks, markets are still trading the war.

Earnings look good. The inflation pipeline does not.

There is a genuine case for optimism. Blended S&P 500 earnings growth for the first quarter is tracking at 15.1% year-on-year, up from 13.1% a month ago. For the high-flying tech sector, it is running at 46.3%. Net profit margins are on pace for their highest in years at 13.4%.

Global growth indicators have also improved at the margin. S&P Global composite PMI readings for April show most major economies either stabilizing or recovering modestly from March’s soft patch. The eurozone is a notable exception, slipping back into contraction. Japan continues to meander. But in aggregate, the growth picture looks less alarming than it did a few weeks ago.

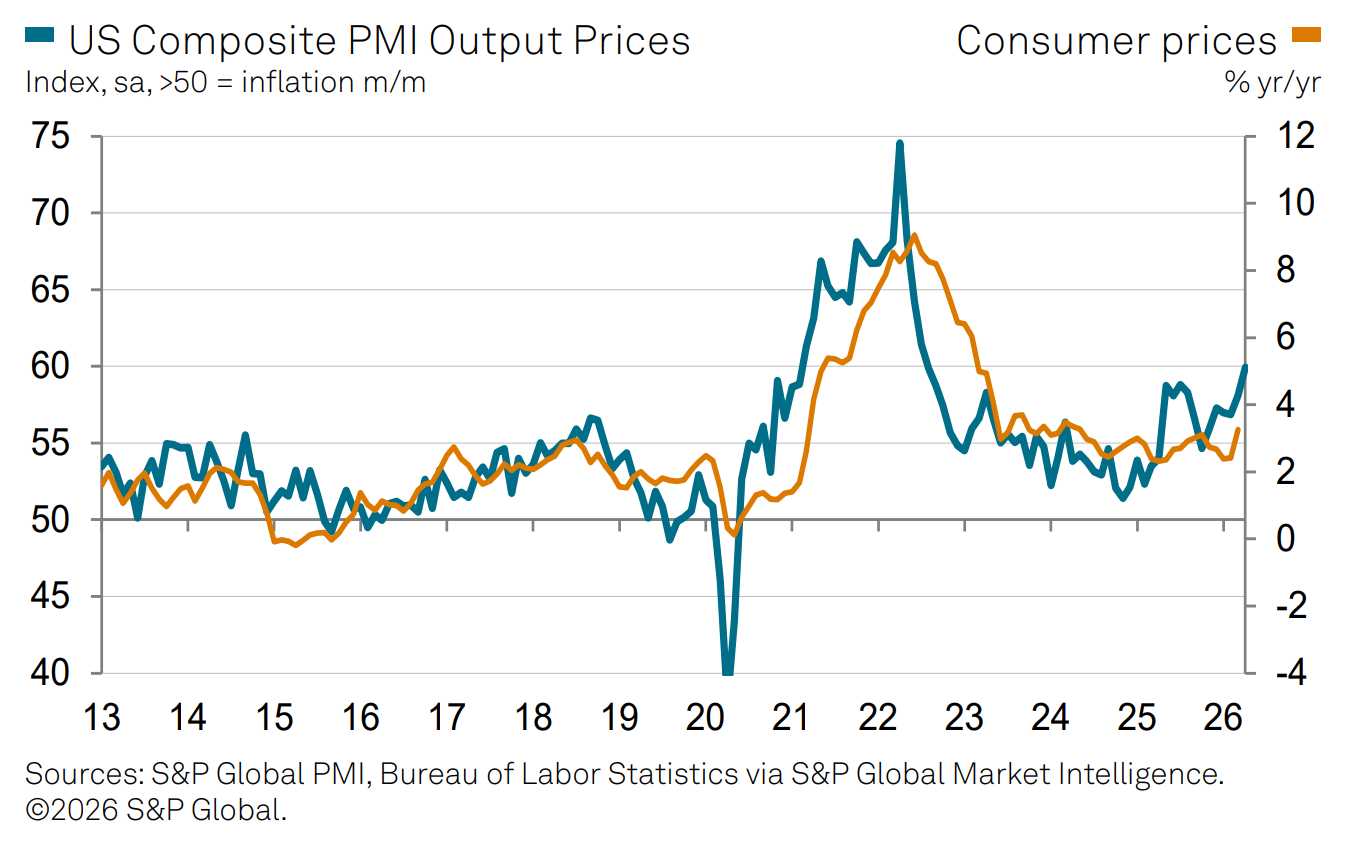

The problem is what those same PMI surveys show beneath the headlines. Input cost pressures are surging, with US implied inflation readings at their highest since 2022. The story is similar in the UK and the Eurozone.

This has been building before the Iran war oil shock has fully reached hard data: with the typical one-month lag from crude prices to the headline US consumer price index (CPI) inflation gauge, the worst of the surge is still ahead. Core goods, services, and housing inflation were all already rising before the war.

Central banks face a high-stakes week

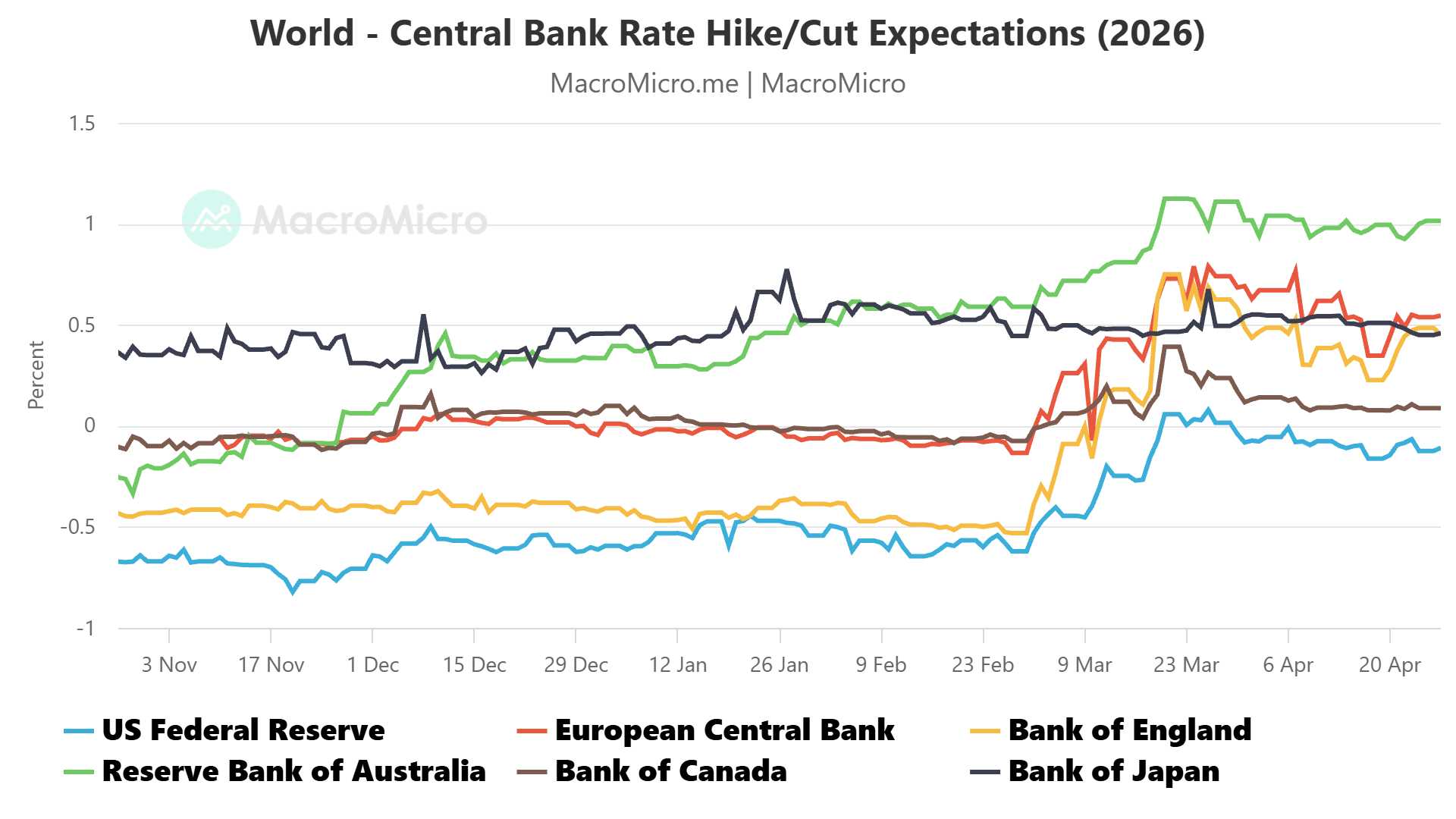

The recalibration in policy expectations has been dramatic.

The Federal Reserve has gone from a pre-war 50 basis points (bps) of priced cuts to zero. The Bank of England (BOE) has swung from 50bps of expected cuts to 50bps of hikes. The European Central Bank (ECB) has shifted from no change for the year to 50bps in tightening. Only the Bank of Japan (BOJ) and Bank of Canada (BOC) have escaped a major repricing.

All of these central banks are expected to hold policy rates unchanged this week. That is almost beside the point, however. What matters is the guidance that officials offer about what is coming next. If officials validate what bond and commodity markets are signaling, that may be the catalyst that snaps stocks back in line with other markets.

There is a bit of added intrigue at the Fed: with the Department of Justice (DOJ) investigation into Chair Jerome Powell dropped, the nomination of Kevin Warsh as his replacement can proceed. A lame-duck Powell with an inflation problem to explain could prove unusually candid.

If stellar tech results are already priced into stocks at record highs, the upside from a strong earnings batch may be limited. Disappointment could accelerate what the momentum indicators already suggest.

The war may not have ended, and inflation may not have been contained, but the stock market is behaving as though both are settled. This week may determine whether that confidence is warranted.

Ilya Spivak, tastylive head of global macro, has over 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices