First 2024 U.S. Presidential Debate, Canada and U.S. Inflation Data: Macro Week Ahead

First 2024 U.S. Presidential Debate, Canada and U.S. Inflation Data: Macro Week Ahead

By:Ilya Spivak

Stock markets, Treasury bonds and currencies are looking for fresh fuel. Where will the first U.S. presidential election and PCE inflation data leave them?

Canadian dollar may rise if CPI data tops expectations, dilutes BOC rate cut bets

First presidential debate may help traders frame how to trade the U.S. election

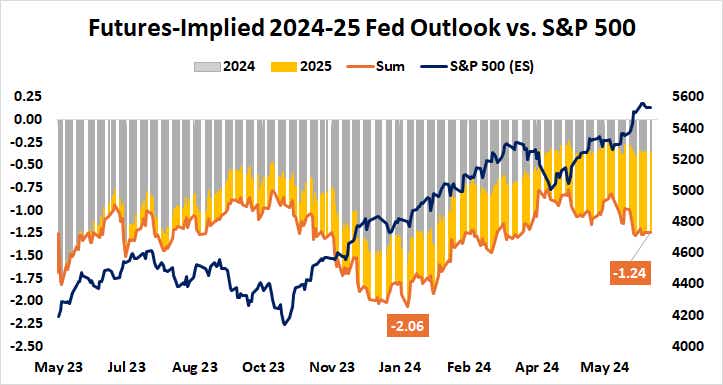

U.S. PCE inflation data may be more impactful in its passing versus the substance

Last week, the financial markets struggled for a clear direction. Upward progress all but stalled on Wall Street, with the bellwether S&P 500 adding just 0.6% and the tech-tilted Nasdaq 100 at near-standstill with a gain only 0.2%. Treasury yields managed slight gains having tumbled in the prior week.

Gold prices held to a narrow range and the U.S. dollar inched higher for a fifth consecutive week, though its gain of a mere 0.1% against the euro was hardly a commanding performance. Crude oil and bitcoin prices continued to march to the beat of their own drum. The former extended higher and the latter lower, but at a slower pace than the prior week.

Will the markets find greater conviction ahead?

Here are the macro waypoints that are likely to shape price action.

Canada consumer price index (CPI) data

Inflation in Canada is expected to cool have cooled to 2.6% year-on-year in May, the lowest since March 2021. The core rate, which aims to factor out temporary volatility to get at the central trend in price growth, is seen holding at 1.6% for a second consecutive month. That too is the lowest in over three years.

The Bank of Canada (BOC) began to lower interest rates this month, lowering its target lending rate by 25 basis points (bps) from 5% to 4.75%. Futures markets are pricing in a rate of 4.29% by the end of the year, implying 46bps in further easing. That amounts to at least one more 25bps cut and a commanding 92% probability of a second one.

Leading purchasing managers index (PMI) data from S&P Global points to improving economic conditions, with May marking the first expansion in private sector output in a year. That came alongside a pickup in employment and in prices. Meanwhile, analytics from Citigroup suggest Canadian data outcomes have been improving relative to forecasts.

If this sets the stage for an upside surprise on the CPI release, traders may mark down scope for BOC easing. That is likely to push up the Canadian dollar.

.png?format=pjpg&auto=webp&quality=50&width=1000&disable=upscale)

First 2024 U.S. presidential debate

U.S. president Joe Biden will face rival Donald Trump in the first face-to-face debate of the 2024 election cycle. This year’s contest is a rematch of the 2020 election, which left Mr. Trump without a second consecutive term in office after he defeated Hillary Clinton in 2016 and brought Mr. Biden to the White House.

Since both candidates have already occupied the top post in the U.S. executive branch, it is tempting to conclude that they are known quantities and dismiss the face-off as little more than a spectacle. Furthermore, both administrations have shown a penchant for expansionary fiscal policy and a combative stance on trade, especially with China.

Nevertheless, there remains the potential for important differences on economic policy, including the fate of the Federal Reserve. For instance, policy ideas tipped to be on the menu for another Trump term have included curbing the central bank’s independence in setting interest rates.

With that in mind, the debate may turn out to be an important framing exercise. It ought to be instructive to see how Treasury yields and the U.S. dollar behave in response to what is discussed and which candidate is perceived to have outperformed, if only to establish whether the contest merits active monitoring from investors.

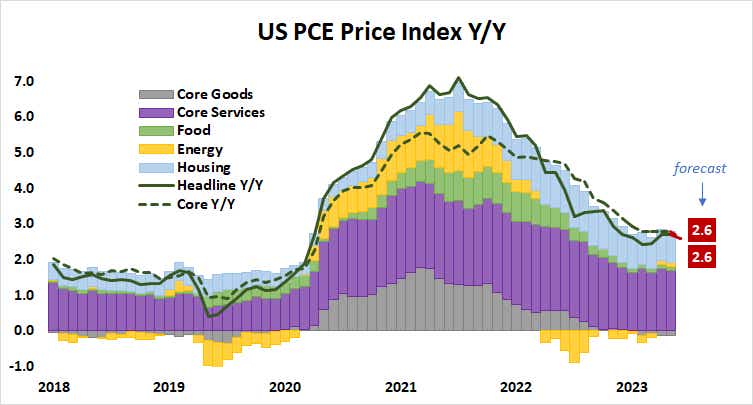

U.S. personal consumption expenditure (PCE) inflation data

The May edition of the Fed’s preferred measure of U.S. inflation is expected to tick lower to 2.6% year-on-year, the lowest in three months. The core rate excluding volatile food and energy prices – the number most closely watched by central bank officials – is penciled in at the same reading, ending three months of standstill at 2.8%.

Market economists are usually quite good at forecasting the PCE number once the consumer and producer price indexes (CPI and PPI, respectively) have been published for the same period. This means that scope for a meaningful, market-moving surprise is relatively limited.

Still, traders’ acute focus on where the U.S. central bank is steering might make for an attention-worthy response from price action. The passing of event risk can unlock trading activity held back ahead of potential event risk, revealing the markets’ disposition in the absence of a barrier to directional conviction.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices