Stock Market Meltdown: Time to Buy the Dip? | Macro Week Ahead

Stock Market Meltdown: Time to Buy the Dip? | Macro Week Ahead

By:Ilya Spivak

A brutal market rout no longer needed an Iran headline to ignite it. With US inflation data on deck, was that the end of the damage or just a pause?

- A single brutal session erased a nine-day rally, and today’s attempted bounce fizzled into the close

- The selloff struck even as crude oil fell for a third day, signaling the inflation trade has gone self-sustaining

- Will this week’s US CPI report, seen jumping toward 4.2%, pour fuel on the fire?

After a brutal end to last week, markets tried but struggled to steady today. The bellwether S&P 500 attempted a bounce that fizzled into the close, leaving open the question that matters: was last week’s plunge the end of the damage or just a pause before more? Friday alone erased a nine-day grind to record highs, the kind of single-session destruction that tends to mark a change of character rather than a passing dip.

The selloff that didn’t need a fresh headline

The technical warning had been building for weeks: the melt-up came on steadily diminishing volume while the relative strength index (RSI) flashed negative divergence, with price setting higher highs that the momentum gauge would not confirm. Friday delivered the resolution. The S&P now sits back at the base of the range set nearly a month ago, a secondary top in place. If it breaks, the next downside target near 7100 is in view for the next leg lower.

The most telling part is what did not drive it. Crude oil fell for a third straight day on Friday, yet the “inflation trade” roared anyway. Treasury bond prices extended their slide toward the May lows, pushing yields higher. Gold broke major support and looks headed toward $4100/oz. The US dollar surged — and the manner of it was revealing. When nearly every asset falls and the greenback outperforms, the market is prizing cash over returns. That is the hallmark of genuine risk aversion rather than ordinary repositioning. If that mindset persists, the US currency’s breakout from its months-long range may only be getting started.

The inflation trade has detached from the war

That crude could fall while the inflation trade surged points to something structural. The disruption to the Strait of Hormuz is not the sort that reverses on a single hopeful headline. Output already lost will take months and years of rebuilding to restore, and transit is unlikely to return to its pre-war freedom of navigation now that the strait has been activated as a tool of military leverage — a move with no easy reversal, much like the weaponization of the US banking system in recent geopolitical conflicts.

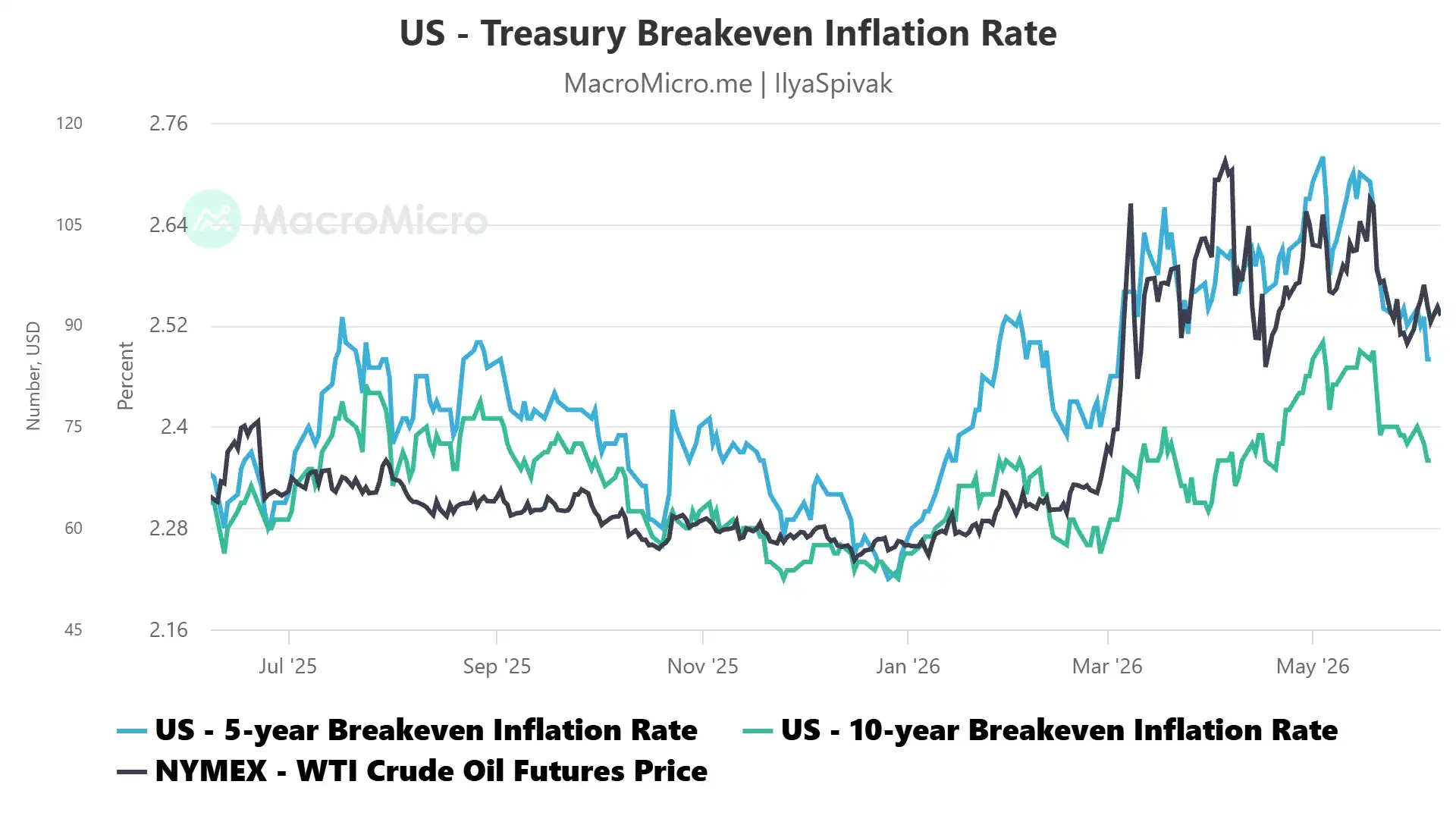

The upshot is that the inflation narrative now exists independent of what any deal between Washington and Tehran might look like. The damage is done. Crude moves take roughly a month to filter into the consumer price index (CPI), and the data is only beginning to absorb the wartime spike — at best, several months of pass-through still lie ahead. Markets know it: 5-year and 10-year breakeven inflation rates have repriced higher and are normalizing at those elevated levels, having fallen alongside crude into late 2025 only to reverse decisively in January. The energy shock’s imprint on inflation looks locked in.

A week of data built to test the thesis

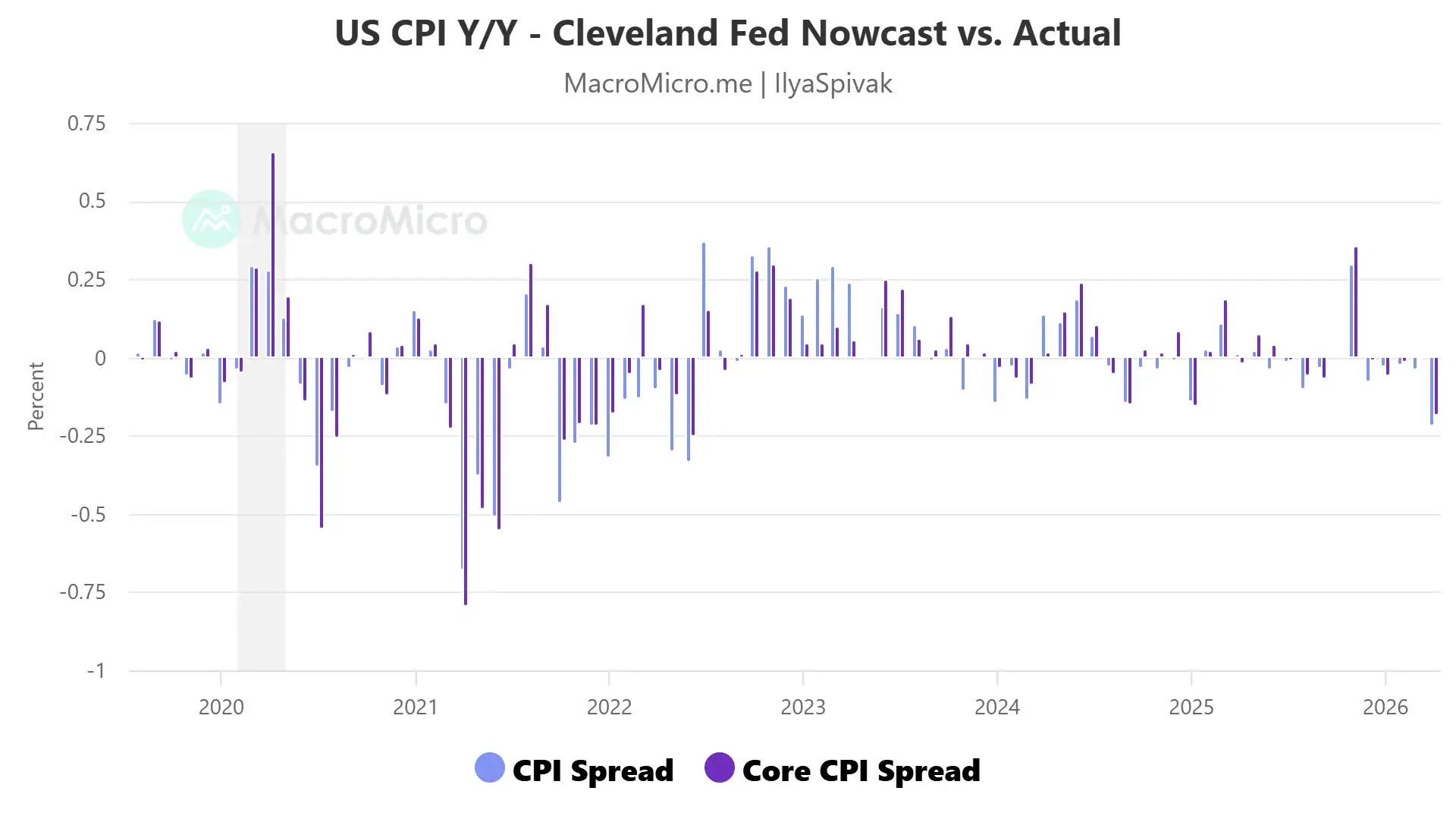

The calendar could hardly be better aimed. The May US CPI report is expected to show the headline rate jumping from 3.8% to 4.2% year-on-year, with the core measure that strips out food and energy edging from 2.8% to 2.9%. The risk skews hot: the Cleveland Fed’s closely watched inflation nowcast undershot the actual print last month by the widest margin since 2022, when the Fed was hiking in 75-basis-point clips to chase runaway prices. If consensus is again lowballing stickier-than-expected inflation, the surprise could be larger than markets are braced for.

A European Central Bank (ECB) rate decision follows later in the week. The same forces buffeting the US are hitting the world’s second-largest economy, and the ECB — biased toward cuts just three months ago — is now seen hiking, with pricing aiming toward 75 basis points (bps). It does so into an economy already in contraction: a few months of genuine stagflation are effectively on the books. That makes Europe a live preview of the bind the US may face next. The week closes Friday with University of Michigan (UofM) gauge of US consumer sentiment, already at a record low, its decline tracking tightly with consumers’ own surging inflation expectations.

Why last week’s selloff may be the start, not the end

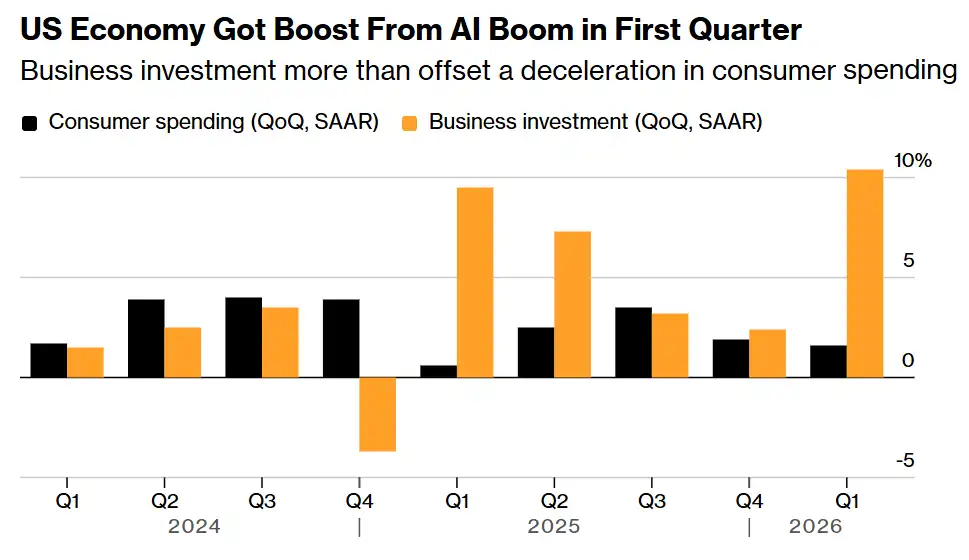

Beneath all of this sits an economy growing in an unusually fragile way. First-quarter US gross domestic product (GDP) expanded just 1.6%, barely half the roughly 4% pace logged before last year’s government-shutdown quarter — and it got there only because business investment, a mere 14% of the economy, grew at a blistering 10.4% annualized clip and out-contributed consumption, which is 68% of output and has now slowed for two straight quarters. Running a relatively small part of the economy that hot is itself inflationary, layered atop the war’s energy shock.

That fragility is the danger. With consumer sentiment at record lows and inflation squeezing households, it would not take much of a downshift in consumption to overwhelm even a fast-spinning investment engine and crack headline growth outright — not a drift into low growth but an actual contraction. Central banks offer no cushion: Fed funds futures price a hike for this year, the ECB is aiming higher still, and among the major central banks, only the Bank of Japan (BOJ) seems to stand apart. Stocks spent weeks treating the artificial intelligence (AI) buildout as a reason to look past inflation worries on display in other markets. Friday suggests traders are finally reading the same page as bonds, gold, and the dollar. If this week’s CPI confirms inflation is stickier than hoped, the bounce that fizzled today will look less like a bottom and more like the eye of the storm.

Ilya Spivak, tastylive Head of Global Macro, has over 15 years of experience in trading strategy. He specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices