Stock Markets Under Fire: Is the AI Boom Rally Overheating?

Stock Markets Under Fire: Is the AI Boom Rally Overheating?

By:Ilya Spivak

Stocks fell, the dollar surged, and bonds crept higher — the classic fingerprints of a growth scare. Is this selloff an unwind of AI hype or something worse?

- Technology led stock market losses while defensive sectors gained, a rotation that points beyond mere profit-taking on the “AI boom” trade

- Treasury yields ticked lower and the dollar jumped — that looks like capital fleeing into cash and safety, not just worrying about inflation

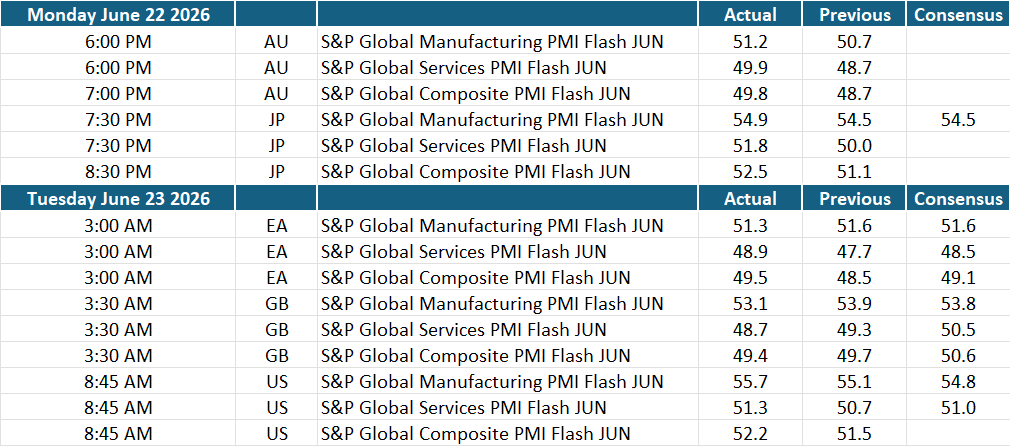

- June PMI data shows booming manufacturing and a stalled service sector across major economies. In Europe and Australia, that growth mix is already failing

Has sentiment finally broken? Stock markets swooned in Wall Street trade. The bellwether S&P 500 took out near-term support just under 7500 and could be carving out a major top, having lost steam on a climb from 7200 toward 7600 amid fading volume and waning momentum studies yet again.

This looks like a growth scare, not just an AI unwind

The selling was led by the technology names, down nearly 4%, with cycle-sensitive sectors like basic materials and industrials close behind. Meanwhile, defensive sectors rose — consumer staples added almost 2%, while healthcare and real estate rose nearly 1.5%.

This ominous mix seems to point to something more than just investors trimming exposure to frothy trades tied to the artificial intelligence (AI) boom. It may point capital repositioning for trouble in the economy itself.

The cross-asset picture sharpens the point. Gold fell and the US dollar surged, punching further past the range top that had contained it for nearly a year. Crucially, Treasury bonds did not keep sinking as they have when traders’ fears hinged on the US-Iran war and its inflation implications; instead, yields ticked slightly lower on the day.

A simultaneous decline in stocks and most commodities, paired with firmer bonds and a soaring dollar, is “risk-off” price action in its classic form — capital fleeing less liquid, riskier assets and rushing into cash and the deepest pool of safety, US Treasuries. This flight to liquidity hints that the wartime “inflation trade” is evolving into something much more sinister.

Notably, this is happening as oil keeps falling

All of this unfolded while the supposed source of the malaise was easing: crude oil broke below its wartime range and is approaching pre-war levels, its uptrend abandoned, as Washington and Tehran commit to a 60-day peacemaking window and geopolitical risk premium drains out of prices.

If the war were still the chief worry, sentiment should be improving. It is deteriorating instead, confirming what the rates trade has signaled for weeks. For markets, the conflict was always primarily an inflation story: from an energy shock to the resulting upward squeeze on rates, and the fragile growth underneath. Traders now seem to be eyeing the next chapter: not the inflation, but the downturn that it threatens to cause.

The PMIs reveal a dangerous imbalance

June’s US purchasing managers index (PMI) data looked strong on its face, pointing to the fastest economic activity growth since January. Under the surface, however, that progress has come thanks to a booming manufacturing sector, while services are managing little better than standstill. This looks like the same lopsided mix that defined first-quarter Gross Domestic Product (GDP) data: growth is powered by overclocking the smaller of the economy’s output engines. Not surprisingly, that is stoking inflation.

Economies outside the US show where this can lead. Analog PMI data showed that across Australia, the Eurozone, and the UK, manufacturing is booming yet the economies are contracting, because a shrinking service sector is far larger and drags the whole down. The US and Japan are still growing thanks to their deeper ties to the AI buildout, making the boost from manufacturing more potent, but the baseline imbalance remains. Growth is yet to falter under the weight of a sluggish service sector, but the direction of travel seems to be unmistakable.

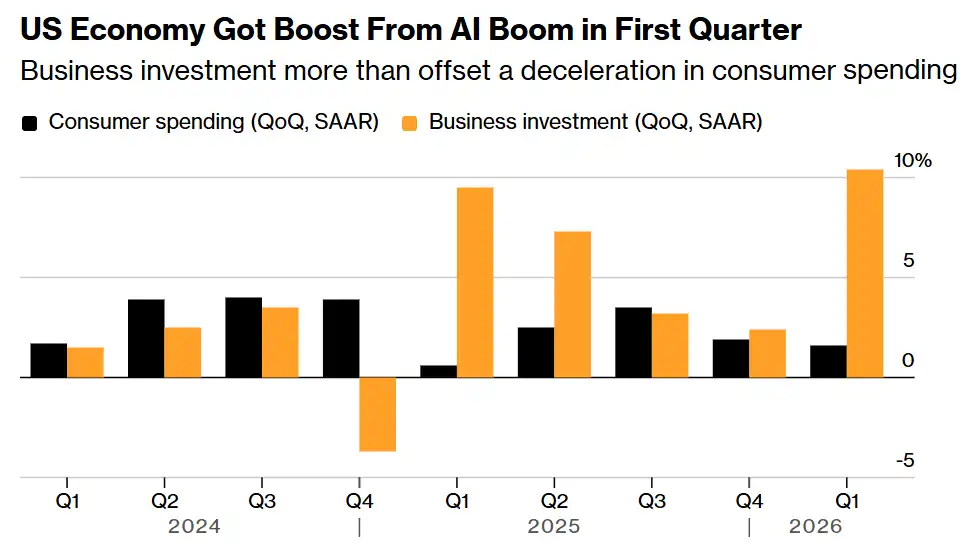

Why the imbalance was never sustainable

The math has always been precarious. GDP grew just 1.6% in the first quarter — less than half the roughly 4% pace of last year’s middle quarters — and it managed that only because business investment, about 14% of the economy, expanded at a scorching 10.4% annualized clip and out-contributed consumption, which is 68% of output and has retrenched for two straight quarters.

That such an arrangement can be sustained for any significant period of time has always appeared suspect. The idea that investment could spin fast enough to carry growth over a longer term even as the inflation it threw off bore down on the five-times-larger consumer sector was never plausible for long. Sooner or later the gravitational pull of retrenching consumers proves too strong to resist and growth slips, as the PMI numbers from Europe and Australia readily attest.

The latest defensive stock market rotation, firmer bonds, and surging dollar suggest that traders are beginning to suspect that a turn of some sort is near. The Federal Reserve, having shifted decisively hawkish and now priced to hike interest rates as soon as September, is in no position to cushion the blow. The relief that carried stocks back toward their highs this month may be running out of road.

Ilya Spivak, tastylive Head of Global Macro, has over 15 years of experience in trading strategy. He specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices