Stocks Struggle Despite Micron Surge, Oil Price Drop. What's Wrong?

Stocks Struggle Despite Micron Surge, Oil Price Drop. What's Wrong?

By:Ilya Spivak

US growth was revised higher and the war premium has drained out of oil — yet stocks can’t rally. A closer look at the GDP data shows why: the economy may be eating itself.

- A Micron-fueled gap higher faded all day, leaving the S&P 500 back below the support it broke this week

- First-quarter GDP was revised up to 2.1%, but the internal imbalance behind it only grew starker

- Investment-led growth tops out near 2% and the inflation it generates is hollowing out the consumers who drive the rest

Micron Technology (MU) gave the market something to cheer, and it still could not stick the landing. The chipmaker’s blowout results gapped the bellwether S&P 500 up to chart resistance at the open, only for the index to bleed lower all session and surrender every cent of the gain, leaving the index below the support it broke earlier this week. A booming semiconductor space – clear evidence that the artificial intelligence (AI) buildout is thriving, bought stocks nothing. That refusal to rally on unambiguously good news is the heart of the story.

Good news everywhere, and stocks still won’t lift

The puzzle deepens across other markets. Gold steadied after sinking like a stone, finding footing as it negotiated the $4000/oz level. Crude oil steadied after a relentless selloff erased the entire wartime run-up in the global Brent benchmark, the geopolitical premium draining away as Washington and Tehran wind the conflict down. Treasury bonds, which fell relentlessly through the war as yields climbed, have reversed higher over recent days, pulling yields back down. So, the war premium is gone, borrowing costs are easing, and the AI engine is roaring. Stocks should be delighted. They are not — and the reason showed up in the day’s economic data.

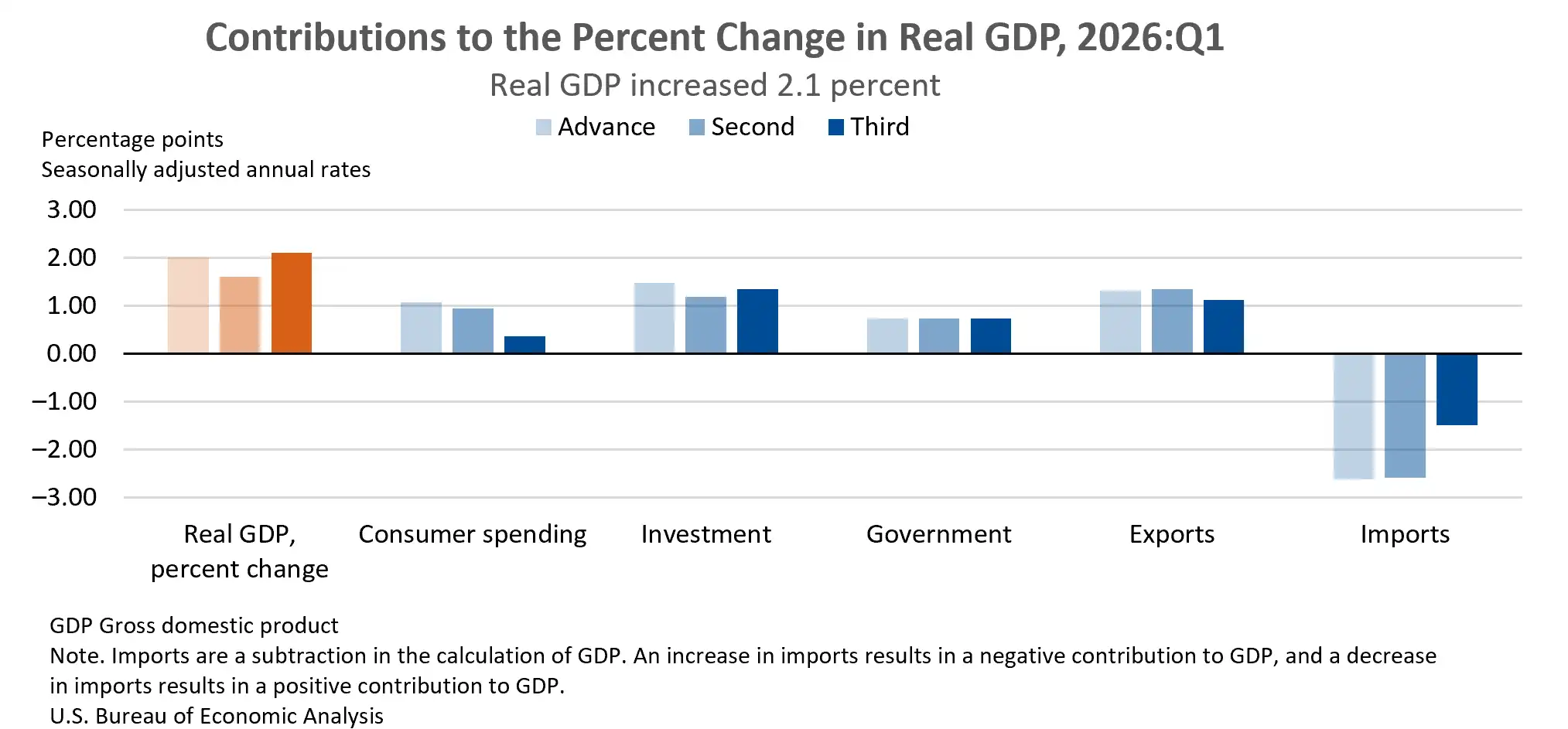

A better headline, a worse economy

The third and final revision of first-quarter US gross domestic product (GDP) rarely warrants much attention, but this one does. Growth was marked up to 2.1%, from 1.6% in the prior reading — a stronger headline that conceals a starker imbalance underneath. Consumption, which makes up 68% of the economy, contributed barely anything. Investment, just 14% of output, did the heavy lifting, and part of the upward revision was merely flattered by a smaller drag from imports rather than any genuine surge in demand.

The deeper problem is what history says about this configuration. Spinning a smaller GDP growth engine fast enough to outrun one five times its size takes a blistering pace — business investment grew above a 10% annualized clip, powered by the data center boom, even as consumption slowed. But investment-led growth has a ceiling. Over the past two decades, it has almost never contributed more than about 2 percentage points to GDP outside the post-pandemic rebound, whereas consumption-led growth routinely clears that bar. In other words, 2.1% is roughly as good as this arrangement gets — against the nearly 4% the economy managed last year when the consumer was strong. The last time consumption was similarly weak, in the first quarters of 2022 and 2025, the economy was contracting.

How the economy starts to eat itself

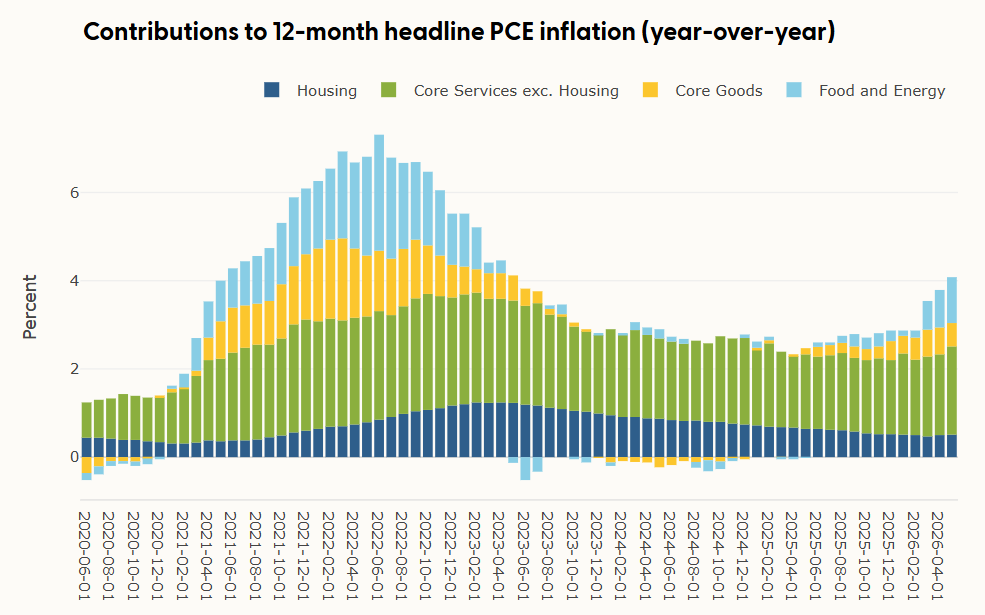

Here is the trap. To manage even mediocre growth, the investment component of GDP has to spin so fast that it throws off inflation — and the day’s price data shows exactly that. The personal consumption expenditures (PCE) index, the Federal Reserve’s favored gauge, rose to 4.1% year-on-year in May, the highest since April 2023, with the core measure at 3.4%, the most since October 2023. Crucially, core services inflation reached its highest share in three years.

That last detail is telling. Services are precisely what consumers spend most of their money on, so when the investment boom drives up core services prices, it directly erodes households’ ability to keep spending. The very growth model generating the inflation is undermining the consumer it ultimately depends on — an economy, in effect, begins to eat itself. The energy scarring from the war, lodged in costs like warehousing and freight, will fade only slowly and add to the squeeze, but the self-defeating growth mix is the durable problem. The endgame is already visible abroad: in Europe and Australia, manufacturing is catching the global AI wave, yet the economies are shrinking because their far larger service sectors have been squeezed into contraction. The US and AI-heavy Japan are not there yet, but the dynamic is the same.

The wrong kind of dovish turn

This reframes what markets should expect from the Fed. The war-trade logic said relentless inflation would force the central bank into a hawkish stance, and rate-hike bets duly soared. But the bond rally and shifting tightening odds tell a new story: the likely timing for a hike has slipped from September to October, a second is now roughly a coin toss, and traders are starting to pencil in the Fed reversing course as soon as the middle of next year. The central bank may end up less hawkish than the war trade implied — not because an inflation shock receded, but because it is already destroying demand.

That is the unwelcome punchline. A pivot back toward rate cuts would normally cheer stocks, but cuts delivered because growth is buckling are a recession signal, not a green light. It explains why a blowout from Micron and a vanishing war premium cannot lift the market: investors are looking past the inflation scare to the downturn it threatens to set off. An economy that can only manage 2% growth by stoking the very inflation that hollows out its consumer is caught in a bind it cannot easily escape. Until that contradiction resolves, rallies on good news look likely to fade, and a market that can no longer rise on goldilocks headlines is telling its own story.

Ilya Spivak, tastylive Head of Global Macro, has over 15 years of experience in trading strategy. He specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices