US Jobs Data: Is the AI Building Boom Stronger Than Recession Risk?

US Jobs Data: Is the AI Building Boom Stronger Than Recession Risk?

By:Ilya Spivak

US jobs data will test whether the AI buildout boom can overpower economic headwinds after the US-Iran war.

- Nonfarm payrolls are slated for a 62k rise in April while the jobless rate holds steady at 4.3%

- Leading ISM PMI data warns employment is shrinking, falling jobless claims are misleading

- The stock market may swoon on soft jobs data as Iran war inflation keeps the Fed on hold

Stock markets are still grinding higher even as crude oil hovers within its wartime range, now close to 45% higher since the US and Israel struck Iran in late February, and follow-on inflation fears make for hawkish central banks.

Incoming US jobs data is the next clean test of which narrative wins: the AI capital spending surge that did extraordinary work in first-quarter US gross domestic product (GDP), or the cyclical pressures building underneath.

The stock market surge is really just a single trade

The bellwether S&P 500 closed at another record today, but the technical issues flagged since last week persist. Trading volumes have shrunk throughout the rebound from the US-Iran wartime selloff, and the relative strength index (RSI) has flatlined even as prices set higher highs. This hints at ebbing bullish momentum.

The equal-weight S&P 500 (ETF: RSP) has lagged meaningfully and remains below February’s highs. The equal-weight Nasdaq (ETF: QQEW) is barely above water for the year. The “magnificent seven” mega-cap tech stocks (ETF: MAGS) are up just 3.6% since the start of 2026 versus the broader Nasdaq’s 12%.

Software companies (ETF: IGV) that markets see as particularly exposed to disruption from artificial intelligence (AI) are down over 15%. The singular driving force propelling the tech sector and broader market benchmarks higher is rosy optimism about semiconductors and the AI hardware stack — GPU, CPU, and memory makers. Those names (ETF: SMH) are up more than 48% year-to-date.

This is not a broad bull market but a single, narrow trade.

Other markets are still trading the war

Meanwhile, crude oil remains pinned sharply above pre-war levels. Headlines about a possible 30-day US-Iran pause to reopen the Strait of Hormuz arrived earlier today, only to be undercut by Iranian forces firing at an American vessel.

Treasury bond prices have slid back toward wartime lows, sending yields sharply higher. Gold is leaking lower as rising yields and a broadly stronger US dollar – net up 0.67% against the euro since the war began - make non-interest-bearing and anti-fiat assets less attractive.

The AI buildout engine versus the consumer

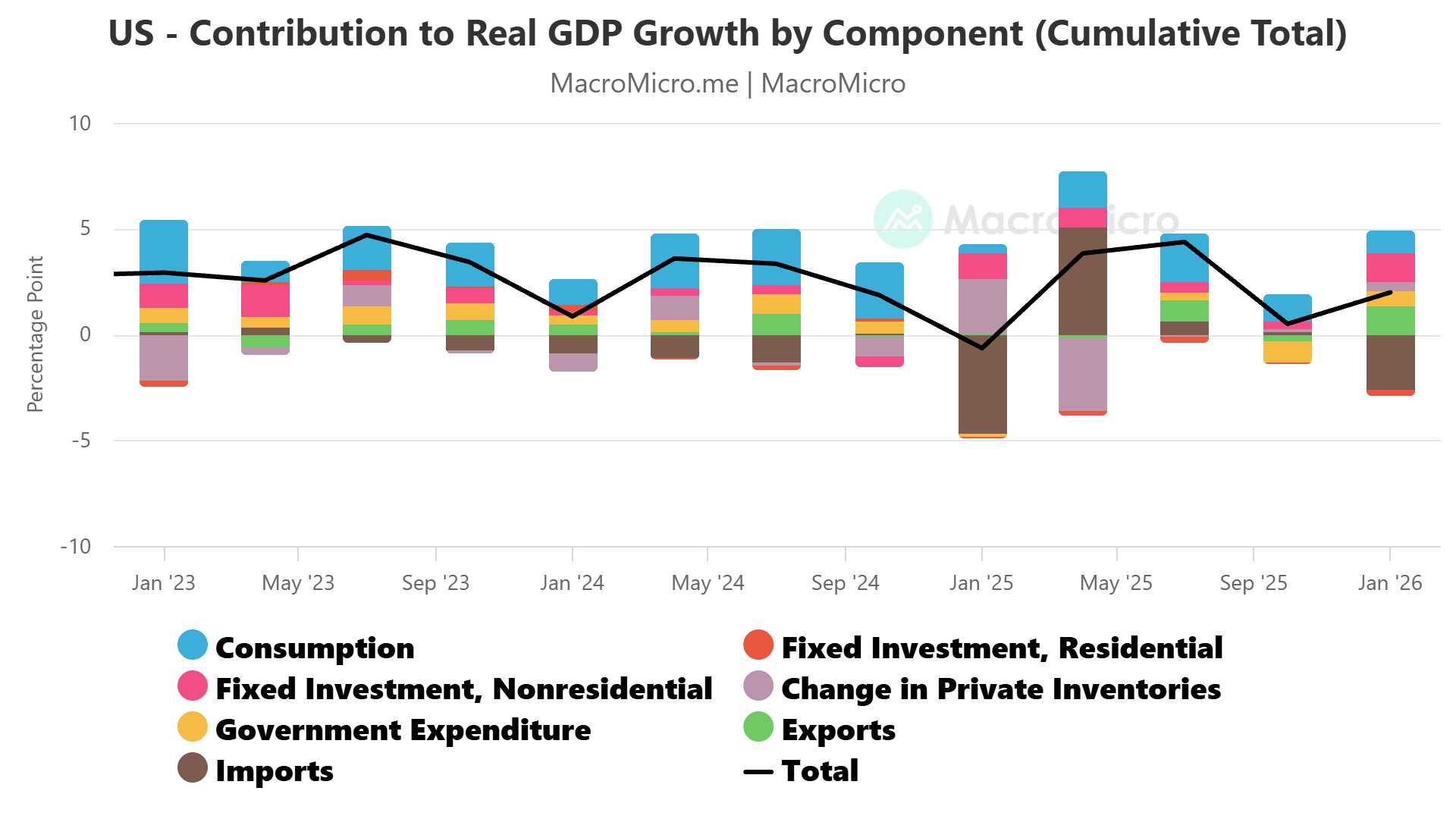

The narrow rally has fundamental underpinnings. First-quarter US gross domestic product (GDP) data showed fixed nonresidential investment contributing 1.39 percentage points (ppt) to the 2% headline growth figure, edging out consumption at 1.08ppt.

That’s staggering considering that consumption accounts for 68% of GDP while nonresidential investment makes up just 14%. The latter’s blistering growth rate made the difference. Business investment ballooned at an eye-watering annualized rate of 10.4% while consumer spending grew just 1.6%, lagging overall GDP growth and slowing for a second quarter straight.

The “hyperscaler” tech firms reporting earnings last week touted nearly $750 billion in 2026 capex to build out AI infrastructure, a figure nearly double that of last year. Demand justifies the urgency: surging demand is stretching compute capacity, forcing OpenAI to shut down its Sora video generation engine and driving Anthropic to throttle its Claude model during peak use hours.

From here, data center builders and consumers are facing the same headwinds: tariffs disrupting supply chains since early 2025 and now the ongoing closure of the Strait of Hormuz amid the US-Iran conflict amount to slower commercial activity and broadly higher prices.

Consumers are already groaning under the weight of these pressures and bottlenecks in the AI buildout area increasingly glaring. Roughly 40% of announced AI data center projects originally slated for 2026 are now expected to be delayed until 2027 or beyond. It’ll be devilishly hard for plucky investment growth to continue to offset sluggish consumption.

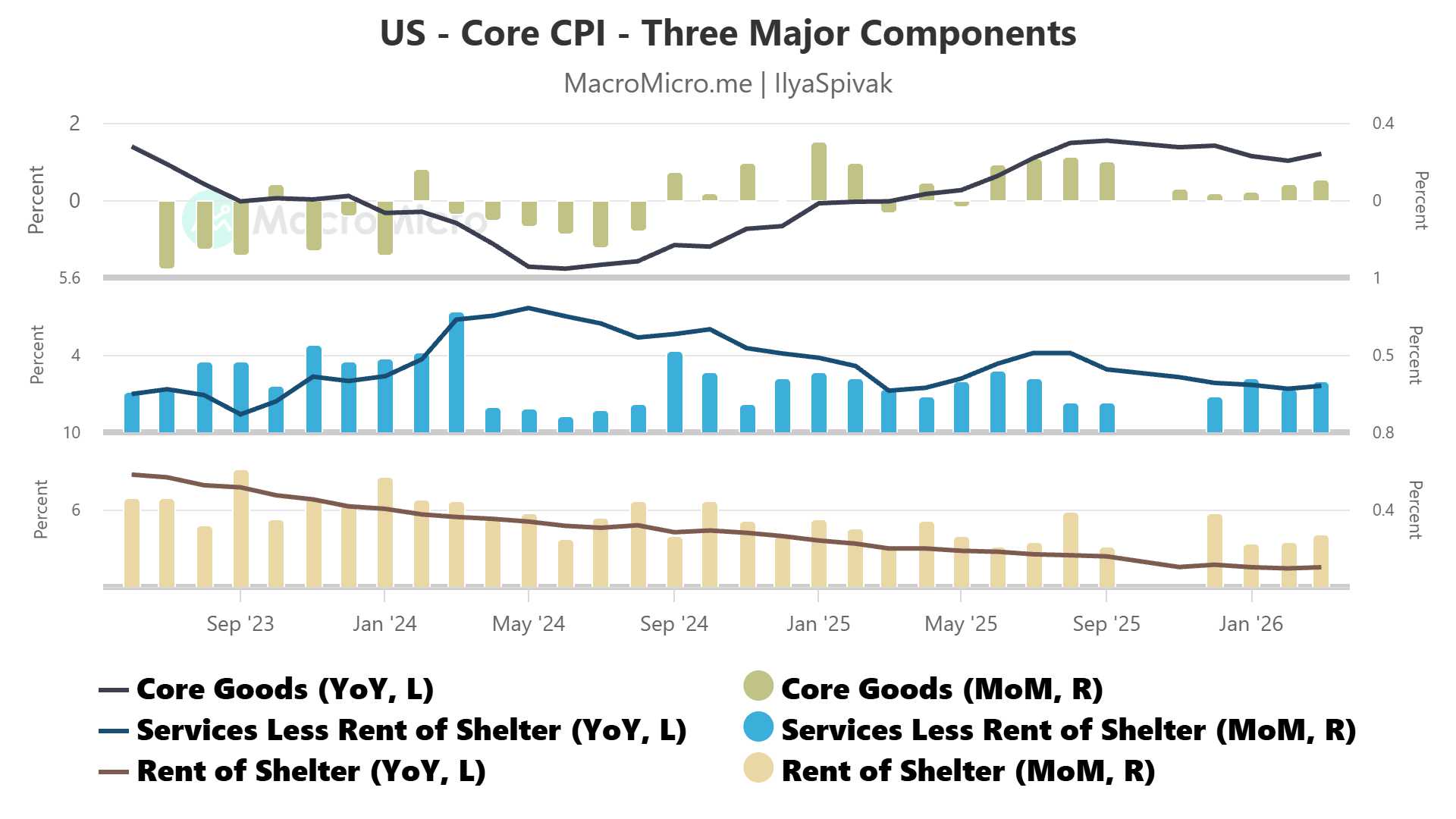

Inflation is broadening as central banks line up hawkish

Core inflation was perking up even before the war’s oil price shock. Goods inflation has been firming since the start of the year. Services inflation has been posting the highest monthly gains since mid-2025. House prices printed their largest monthly rise in three months in March. The jump in energy costs will layer atop these trends, with incoming April price growth data likely to begin showing the war’s consequences in earnest.

Central banks are seen pivoting accordingly. The European Central Bank (ECB) is now seen delivering at least 50 basis points (bps) of rate hikes in 2026 having been slated for standstill at the start of the year. The Bank of England (BOE) has shifted from 50bps of priced cuts to 50bps of hikes. The Reserve Bank of Australia (RBA) is on track for one more cut after delivering its third 25bps increase of the year in May, amounting to 100bps in total. The Federal Reserve is on course for zero cuts after being priced for two of them pre-war.

Why incoming US jobs data matters

US nonfarm payrolls are seen rising 62,000 in April, down after the 178,000 increase recorded in March. The unemployment rate is seen holding at 4.3%.

The leadup is ominous: the Institute for Supply Management (ISM) pointed to contracting employment across manufacturing and services last month in its latest PMI surveys. Falling jobless claims figures look reassuring on the surface but come alongside a falling labor force participation rate, suggesting they speak to structural outflows rather than improving hiring conditions.

A weak jobs report would land in an environment where growth is already holding on by a thread and central banks are in no position to offer policy support. Stocks have spent weeks blissfully ignoring this vulnerability. They may be faced with a rude awakening.

Ilya Spivak, tastylive Head of Global Macro, has over 15 years of experience in trading strategy. He specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices