US Stock Markets Face a Tough March After Trouble in February

US Stock Markets Face a Tough March After Trouble in February

By:Ilya Spivak

US stock markets struggled in February. They might be in for harder times ahead in March.

- S&P 500 posted its first monthly drop in three months in February

- Tech stocks lagged while markets outside the US hit record highs

- Gold rose over 10% and bonds surged, but the dollar is holding up

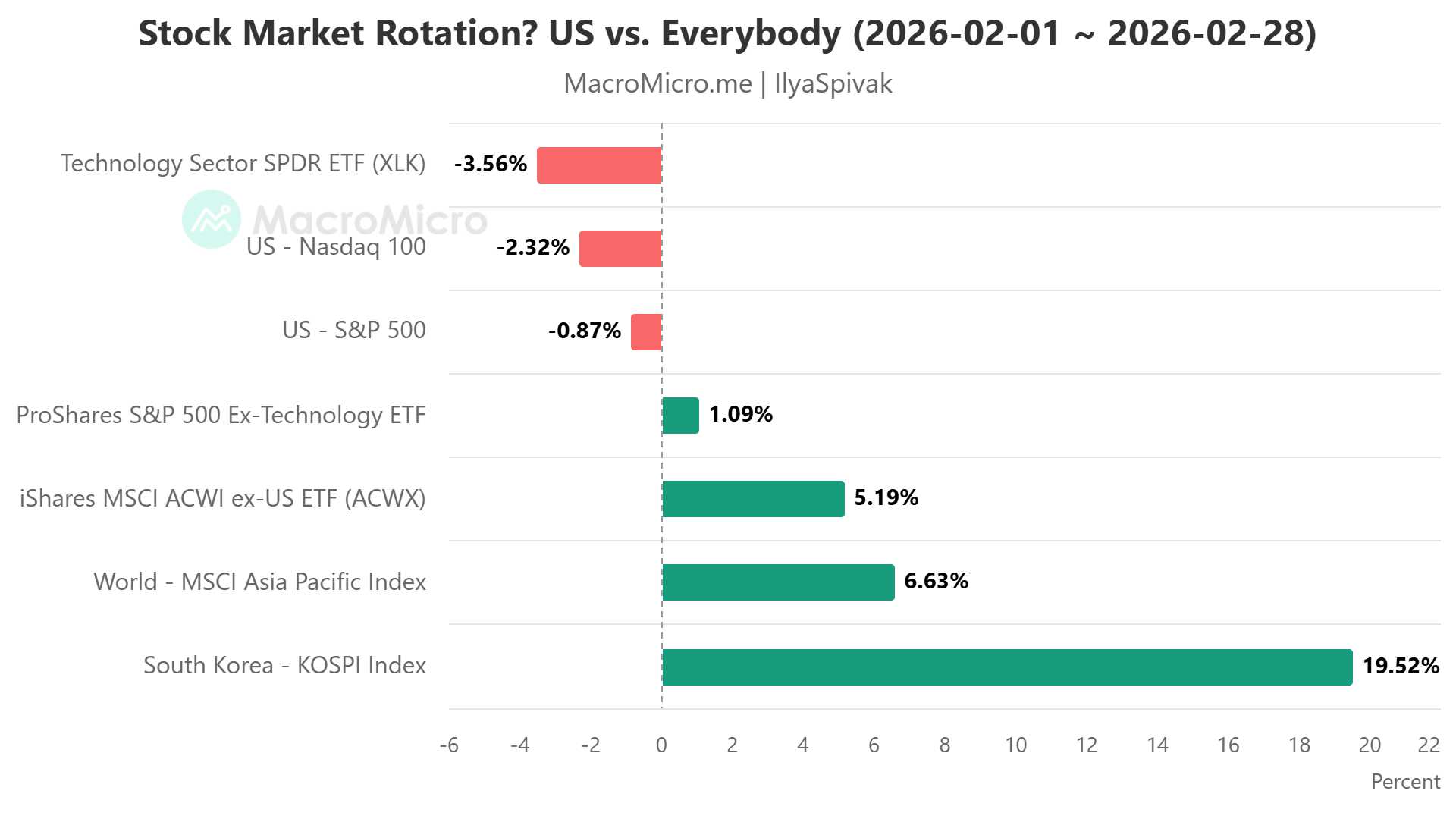

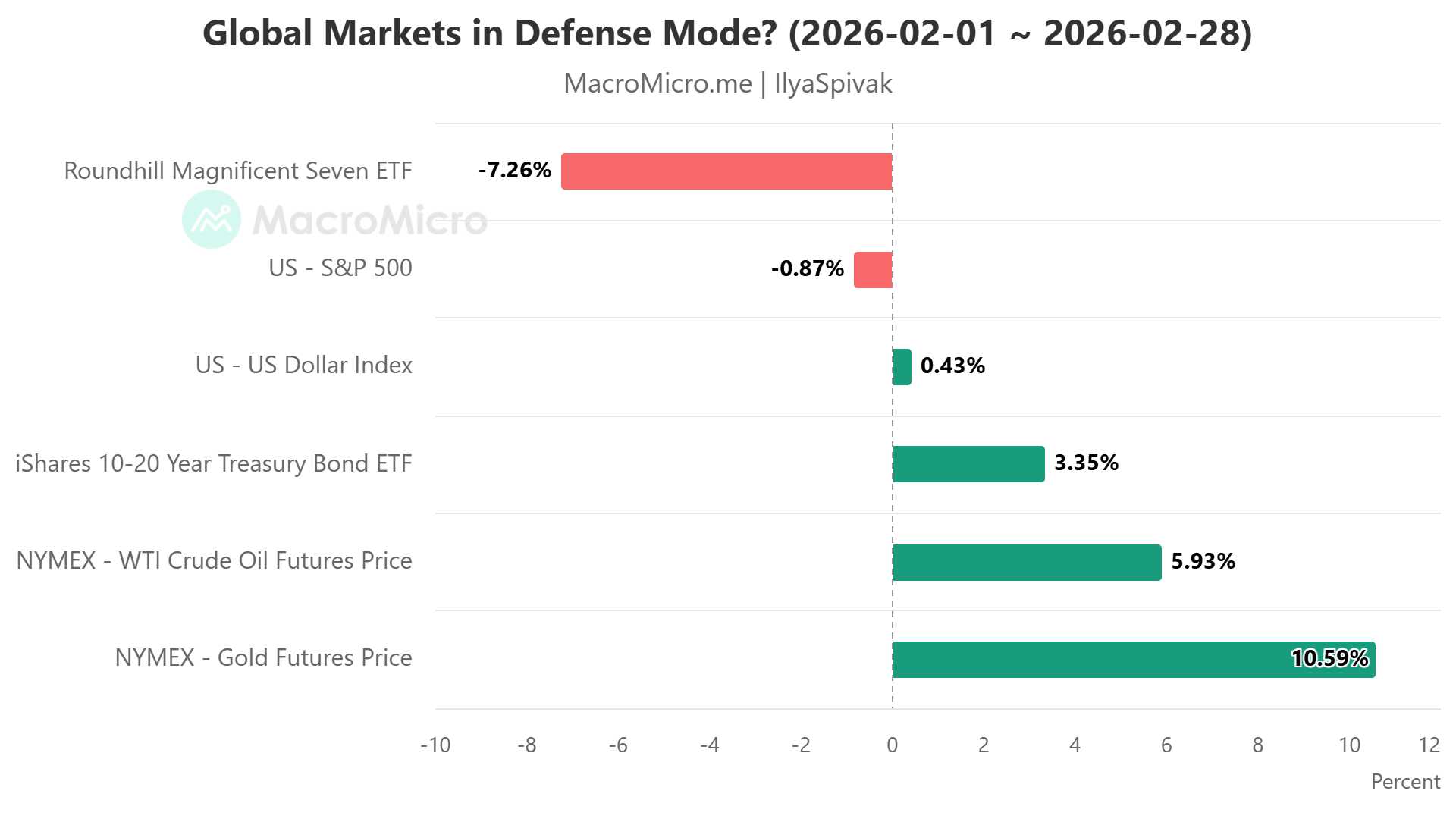

The S&P 500 posted its first monthly decline in three months, slipping 0.87% in February. The drop is modest, but it is the largest since April 2025, when markets were rattled by the unveiling of US President Trump’s tariffs regime. The tech-heavy Nasdaq fared worse, down 2.32% for its biggest slide since March 2025.

Technology stocks are at the center of the weakness. The State Street Technology Select Sector SPDR ETF (XLK) fell 3.56% to its lowest close in five months. Concerns seem to be mounting that the artificial intelligence (AI) boom has stretched valuations beyond a reasonably extrapolated growth path. Software companies’ stocks have come under particular pressure amid fears that AI could disrupt their enterprise business models, not enhance them.

US stock markets are lagging global peers, especially in Asia. Why?

Yet the story is not one of broad-based equity distress. The S&P 500 excluding technology (ETF: SPXT) is up 1.09% this month, marking a record high. Markets outside the United States are faring even better. The MSCI All-Country World Index of stocks excluding the US (ETF: ACWX) has surged 5.19% to its own record. AI-linked markets in Asia have been especially strong, with South Korea’s KOSPI up nearly 50% year-to-date and Taiwan’s TAIEX also rallying sharply, up over 22%.

At first glance, this appears to signal capital rotation away from US assets. However, the US dollar has remained relatively stable throughout February. It managed a modest rise of 0.23% against an average of the greenback’s top currency rivals like the euro and the Japanese yen. If capital were truly fleeing dollar-denominated markets wholesale, the currency would likely be under greater pressure.

That suggests something else is unfolding.

Crude oil prices climbed for a second consecutive month amid speculation about regime change in Iran and stepped-up enforcement against Russia’s so-called “shadow fleet” tankers, with France and India joining US efforts. Expectations of a supply glut seem to be fading. At the same time, gold prices surged 10.6%, posting their biggest monthly rise since March last year.

Taken together, this looks less like geographic rotation against a broadly positive global backdrop and more like de-risking.

Investors appear to be trimming exposure to crowded speculative narratives – notably, the one powering US mega-cap tech names – while increasing allocations to defensive assets. The dollar’s resilience may reflect its unrivaled liquidity as a venue to cash out in periods of uncertainty rather than enthusiasm for US growth prospects.

Are global markets going into defense mode?

Some capital is clearly flowing to AI catch-up trades outside the US, and it is not surprising that less-liquid markets are outperforming accordingly. The MSCI Asia-Pacific stock index has a market capitalization of about $15 trillion, while just the “magnificent seven” tech stocks themselves exceed $20 trillion. However, large pools of money are also clearly bound for defensive assets.

Bond markets seem to reinforce this. Traders have now fully priced two Federal Reserve interest rate cuts this year – double the projection offered up by central bank officials in December – and are increasingly flirting with the possibility of a third one in 2027. Treasuries have rallied accordingly.

The rhetoric from Fed officials seems to be pulling policy the opposite way, however. Minutes from January’s FOMC meeting carried a hawkish tone, with some policymakers even discussing the possibility of putting rate hikes back on the table. Core PCE inflation – the Fed’s preferred price growth gauge – returned to 3% for the first time since April 2024 in December, even as economic growth slowed in the fourth quarter.

Markets seem eager for the insurance of cheaper money in an environment of geopolitical tension and stretched valuations. The Fed, bound by its dual mandate focused on maximum employment and price stability, seems resigned to wait until something truly breaks in the economy or the markets. That divergence sets the stage for an uneasy March ahead.

Ilya Spivak, tastylive head of global macro, has over 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices