Is the Stock Market Really Done Falling? Don't Get Your Hopes Up

Is the Stock Market Really Done Falling? Don't Get Your Hopes Up

By:Ilya Spivak

Markets roared back as Fed rate-hike bets cooled — but they may be falling for the wrong reason. Is the relief rally misreading demand destruction as good news?

- Stocks, gold, and bonds all rebounded sharply, though the move looks more like a retest than a confirmed reversal

- Odds of a December Fed rate hike slid from near-certain on Monday to roughly 60/40 today

- But softer core inflation looks like demand destruction — the consumer breaking, not prices cooling

Markets recovered aggressively across the board on Thursday after a brutal cash-for-everything liquidation earlier in the week. Stocks bounced, gold staged a violent reversal, and bonds rallied. The question is whether the story has actually changed or whether this is a reflexive bounce inside a larger breakdown. The early read leans toward the latter.

A retest, not yet a reversal

The bellwether S&P 500 came roaring back toward the range it shattered just a day before. The index is grinding right where it paused before the breakdown — a retest of whether the market truly wants to extend lower rather than proof that it does not.

Gold’s turn was more violent, erasing nearly all of the prior session’s plunge, yet the larger breakdown remains intact. The bounce may still turn out to be no more than a temporary retracement.

Tellingly, crude oil barely budged even as the White House canceled threatened strikes on Iran in exchange for a supposedly imminent signing of a memorandum of understanding (MOU) — a deal to begin talks, and not a peace accord. For now, the war-trade premium in oil is not unwinding in earnest.

The rally is really a bet on cheaper money

The common thread is bonds. With stocks and gold rebounding, Treasury bond prices rallied too, pushing yields lower in what amounts to an unclenching of interest-rate fears. The odds of a December rate hike from the Federal Reserve, priced as all but certain on Monday, fell to roughly 60/40 by today.

Besides hopes for a US-Iran breakthrough, May’s US PPI data might have helped. While energy prices buoyed the headline reading, core wholesale prices rose a softer 0.4% on the month versus 0.5% expected. The year-on-year trend PPI growth rate held at 4.9%, rather than climbing to 5.4% as economists feared.

The catch: softer prices look like demand destruction

However, a look inside the PPI report’s internals suggests these seemingly benign results appeared not because inflationary pressure faded, but because the consumer is buckling under it. Margins were squeezed hardest are on automobiles and auto parts, while the fattest ones still belong to sellers of fuels and lubricants. Wholesalers slashed their cut on big-ticket, energy-dependent goods to protect demand, in a sign that it may be evaporating.

-960x540.png?format=pjpg&auto=webp&quality=50&width=1920&disable=upscale)

Consumer price index (CPI) data published earlier in the week told the same story: core goods prices fell, but the driver was a decline in used cars and trucks. That looks like demand destruction in plain sight. Energy is squeezing spending on the expensive, fuel-hungry things consumers can no longer justify.

Meanwhile the spillover the Fed actually fears is still building. Core services inflation crept back above 2% for the first time since January, led by transportation and warehousing — the sector’s energy-sensitive corner — for a second straight month. Services prices drive the bulk of inflation, and price rises here looked sticky even as the goods prices rolled over for the wrong reasons.

That is the worst of both worlds for the US central bank. Sticky underlying inflation alongside a consumer that is already pulling back put its policy objectives on a collision course, making it devilishly hard to craft a response.

The wrong kind of rate relief

This is why falling rate-hike odds may be nothing to celebrate. If the Fed ends up holding or easing because demand is collapsing, that is a recession signal, not a green light for risk assets that depend on consumers spending.

Bond market breakeven inflation rates — the 5-year and 10-year expectations embedded in Treasury pricing — have begun diverging lower from crude oil, which itself refuses to break. The market seems to be looking downwind of the price spike and pricing damage to growth, not relief from it.

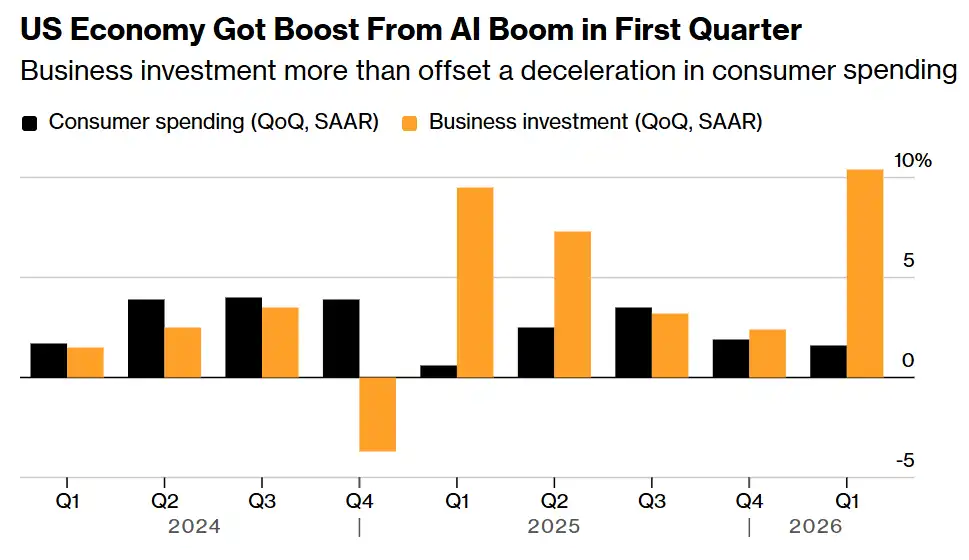

The fragile shape of US growth is what makes this dangerous. First-quarter gross domestic product (GDP) expanded largely because business investment — about 14% of the economy — grew at better than a 10% annualized clip and out-contributed consumption, which is 68% of output and has now retrenched for a second straight quarter. The data center builders driving that investment face the very same energy and freight costs crushing the consumer; they are not immune.

It would not take much further weakening in the dominant 68% slice of the economy to overwhelm even a fast-spinning investment engine. Tomorrow’s University of Michigan consumer sentiment reading — already at a record low of 44.8 — will offer the next read on how close that breaking point is. What looks like a turnaround may instead be a handoff: stocks left hampered while bonds stop falling, as the market trades one fear – inflation – for a graver one: recession.

Ilya Spivak, tastylive Head of Global Macro, has over 15 years of experience in trading strategy. He specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices