Stocks and Gold Prices Melt Down: Is This More Than Just Inflation?

Stocks and Gold Prices Melt Down: Is This More Than Just Inflation?

By:Ilya Spivak

Stocks and gold crashed together in a dash for cash, and the move may not need oil or the Fed to keep going. Has the inflation shock become a growth scare?

- The S&P 500 followed through on its breakdown toward 7100 while gold plunged toward the $4000/oz figure

- Crude oil, Treasury bonds, and Fed rate expectations all sat still — yet the liquidation raged on

- Bond market inflation expectations are now diverging lower from oil, hinting the fear has shifted to growth

It is meltdown mode for financial markets — but not in the way one might have expected. Stocks extended their breakdown and gold cratered right alongside them. What ties these moves together seems to be the destination: cash. Price action is starting to look less like a reaction to any single piece of news and more like liquidation with a life of its own.

A dash for cash, not a reaction to the news

The bellwether S&P 500 followed through on last week’s breakdown, which had been gearing up for weeks amid fading volume and momentum. The index broke the bottom of the range in place since mid-May, exposing the way down toward former resistance turned support near 7100. Gold, meanwhile, did not merely leak lower as it had been — it broke a major inflection level, and a move below $4000/oz now looks to be in play. It seems like last year’s two great speculative narratives are being cashed out at once: gold’s relentless climb as a non-sovereign hedge against a deepening US-China trade war, and the artificial intelligence (AI) buildout trade in equities.

The revealing part is what stayed still. Crude oil — the supposed engine of this year’s inflation fears — went nowhere, even as its uptrend remained intact. Treasury bond prices barely moved. Fed rate expectations barely budged. The liquidation pressed on regardless. The market, it seems, no longer needs crude oil or a fresh tightening scare to fuel its anxiety. That raises a pointed question: even if a US-Iran deal were to materialize, would it matter? The selling has detached from its original trigger.

Why cash — and why bonds are holding up

The key word in liquidation is liquidity. When investors rush to raise cash, they go to the most liquid version — the US dollar, which settles nearly 90% of global transactions. That is why the greenback has held firm even as everything around it falls. The same logic explains a puzzle in the bond market: prices have not crashed despite a still-rising rate backdrop. Part of the reason may be that – at least for now – the markets are not ready to price in more rate hikes. Another part of the story may be haven demand. The US Treasury market remains the deepest pool of so-called “risk-free” assets, and a dash for cash naturally washes into it. Crucially, capital-preservation buyers care little about whether yields drift higher. It is liquidity and safety they are after.

The clue hiding in inflation expectations

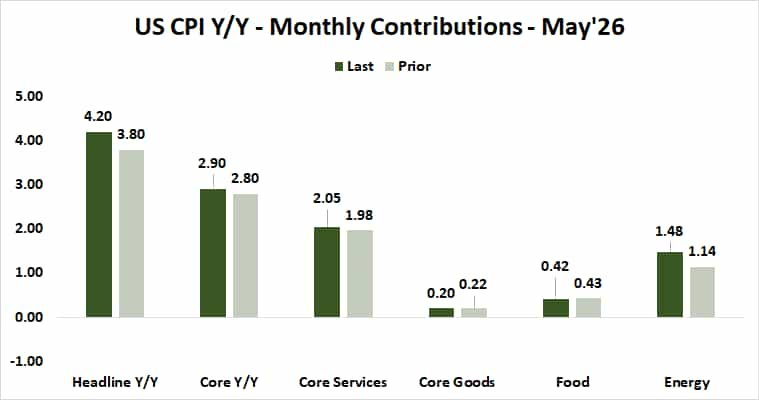

Today’s May US consumer price index (CPI) report landed almost exactly as forecast — a 4.2% headline rate year-on-year and 2.9% on the core measure that excludes food and energy. Energy was the obvious driver, but core services inflation accelerated again, with transportation services standing out as evidence the energy shock keeps seeping into stickier corners of the economy. None of that was a surprise.

The genuinely new signal sits elsewhere. Bond market breakeven inflation rates — the 5-year and 10-year expectations embedded in Treasury pricing — have tracked crude oil higher all year. Now they have begun to diverge lower even as oil holds in its range. Why would inflation expectations fall in this environment? Because the market may be looking downwind of the immediate price spike and concluding that this squeeze on the consumer cannot leave growth unscathed. In other words, the fear is rotating from inflation toward recession.

From inflation shock to growth scare

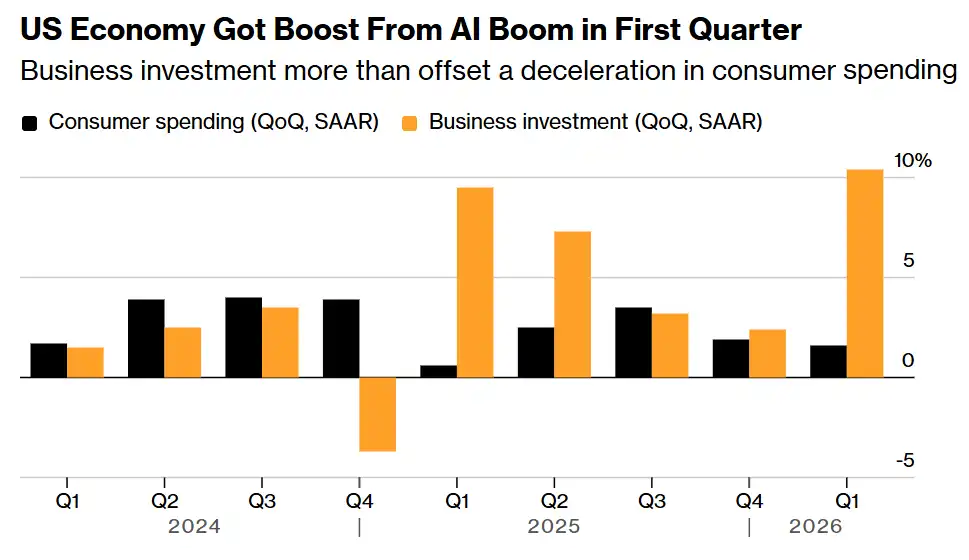

That reframing turns on the fragile shape of US growth. First-quarter gross domestic product (GDP) expanded largely because business investment — a mere 14% of the economy — grew at a blistering annualized clip of over 10% and out-contributed consumption, which is 68% of output and has now slowed for a second quarter straight. Generating growth by overclocking a small share of the economy is inherently inflationary. It is also precarious: it would not take much of a downshift in the already shaky consumer sector to overwhelm even a fast-spinning investment engine. If that happens, growth cracks.

The next 24 hours bring May producer price index (PPI) data, where the question is again whether the energy shock is bleeding into core wholesale costs, as it did last month. A European Central Bank (ECB) rate decision is also on deck. The central bank priced for three hikes this year despite an economy far weaker than America’s — in a preview of the bind the US may yet face. But the deeper message of today’s tape is that the selloff is outgrowing its origins. It no longer waits on an oil headline, a hawkish Fed, or a hot inflation print. Stocks and gold are being liquidated into cash because the market is starting to price the one thing it spent months ignoring: that an economy straining this hard to grow may not keep growing at all. If that is the realization taking hold, the markets may be in the early innings of a far larger repricing.

Ilya Spivak, tastylive Head of Global Macro, has over 15 years of experience in trading strategy. He specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices