Core CPI Preview: Do Stocks Care if Inflation is Higher Than Expected?

Core CPI Preview: Do Stocks Care if Inflation is Higher Than Expected?

By:Ilya Spivak

U.S. inflation data may mark an inflection point for stocks, bonds and the U.S. dollar—no matter what the outcome

- U.S. CPI inflation is seen cooling in September as markets yearn for interest rate cuts.

- An upside surprise may be in store for “core services” prices, the focus for Fed policy.

- How markets react may prove pivotal, especially to higher-than-expected outcomes.

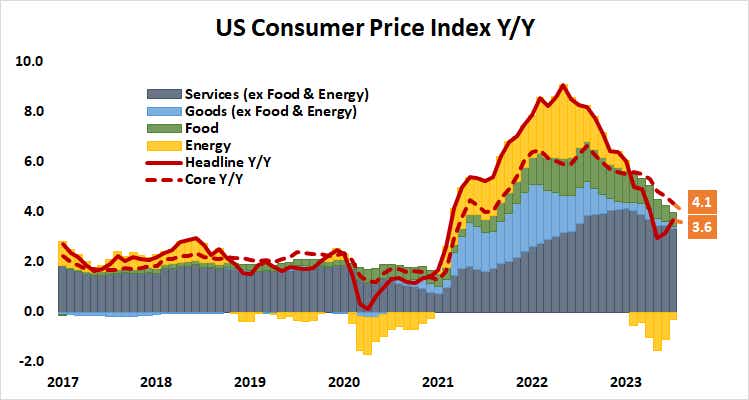

U.S. inflation is expected to have cooled in September. The headline consumer price index (CPI) is seen rising 3.6% year-on-year, a climbdown from 3.7% recorded in August and a break of a two-month streak of accelerating price growth.

The core CPI measure excluding volatile food and energy prices is expected to inch down for a 13th consecutive month. This measure captures pricing trends where Fed policy has some agency for direct impact, so the central bank is probably focused there. Seesawing crude oil prices explain much of the recent disparity between it and broader CPI.

Another downtick is likely to be broadly welcomed by investors. However, its market-moving potential will probably depend on what the numbers mean for the arrival of a much-hoped-for rate cut cycle as global economic growth grinds down to near-standstill, threatening recession.

For the Fed, not all inflation is created equal

This is where things get trickier.

At this stage, the service sector is the main contributor to inflation. This is primarily underpinned by the cost of housing, where the Fed has little agency to drive near-term outcomes. Its own rate hikes have created illiquidity because market mortgage rates exceed what owners have locked in by close to 400 basis points (bps) on average. That has discouraged selling, drawing down inventories and keeping prices up.

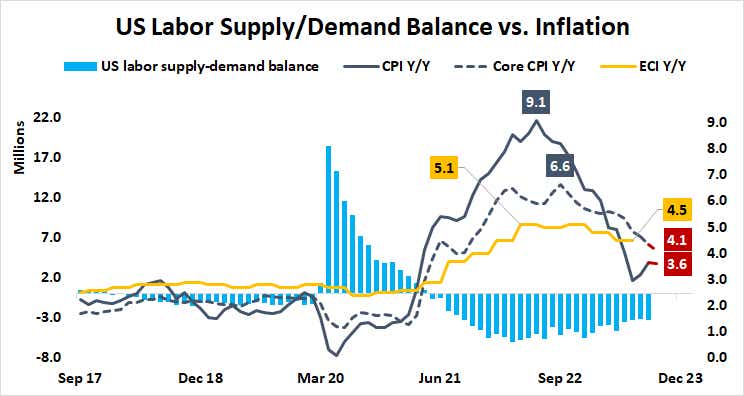

That leaves the labor market. Employment costs have been stickier than overall inflation as labor shortages underpin wages. The U.S. central bank is aiming for higher rates to cool economic activity, reduce labor demand, and trigger a wave of wage agreement resets (i.e., layoffs). It hopes to dial in just enough pain for this process to pass without too much damage, for a so-called “soft landing”.

How long the Fed will wait with rates at their cycle highs before it feels confident enough for a reversal has become the main object of speculation for financial markets. The first 25-basis-point (bps) cut is expected in June 2024. Another has been penciled in by November and a third by December, for a cumulative 75 bps in easing.

That might be a bit too optimistic.

Will markets care if core inflation is stronger than expected?

September’s U.S. jobs data printed much stronger than what was penciled into baseline forecasts, as expected. Surveys of purchasing managers by S&P Global and the Institute of Supply Management (ISM) showed brisk hiring and elevated service sector inflation in September. The former flagged the fastest price growth since July and the latter saw costs rising at a pace matching August’s four-month high.

Furthermore, wholesale inflation turned out to be higher than projected, and for ominous reasons. The producer price index (PPI) rose 2.2% year-on-year in September, sailing past analysts’ median forecast of 1.6% to record a five-month high. The rise was overwhelmingly driven by final “core” domestic demand in the service sector.

On balance, this suggests that—whatever happens with headline CPI thanks to the vagaries of oil markets—the part of inflation that is of greatest interest for the Fed may not endorse a dovish retreat. In fact, an upside surprise is a significant possibility.

Stocks may retreat while bond yields and the U.S. dollar rise in this scenario, but the degree of follow-through on any such move is likely to be critical. If markets shrug off an upside surprise as they did with nonfarm payrolls’ buoyant print last week, the case for bullish trend reversal in stock and bond markets will seem stronger.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices