AI Frenzy Saved Stocks from the Iran War. Now It Is the Problem

AI Frenzy Saved Stocks from the Iran War. Now It Is the Problem

By:Ilya Spivak

Stocks struggled despite cooling inflation as the AI fever broke in overseas markets and US data warned that battered consumers may derail the economy.

- A week of soft inflation and spending data has bonds and gold quietly worrying about an economic slowdown rather than a rate hike

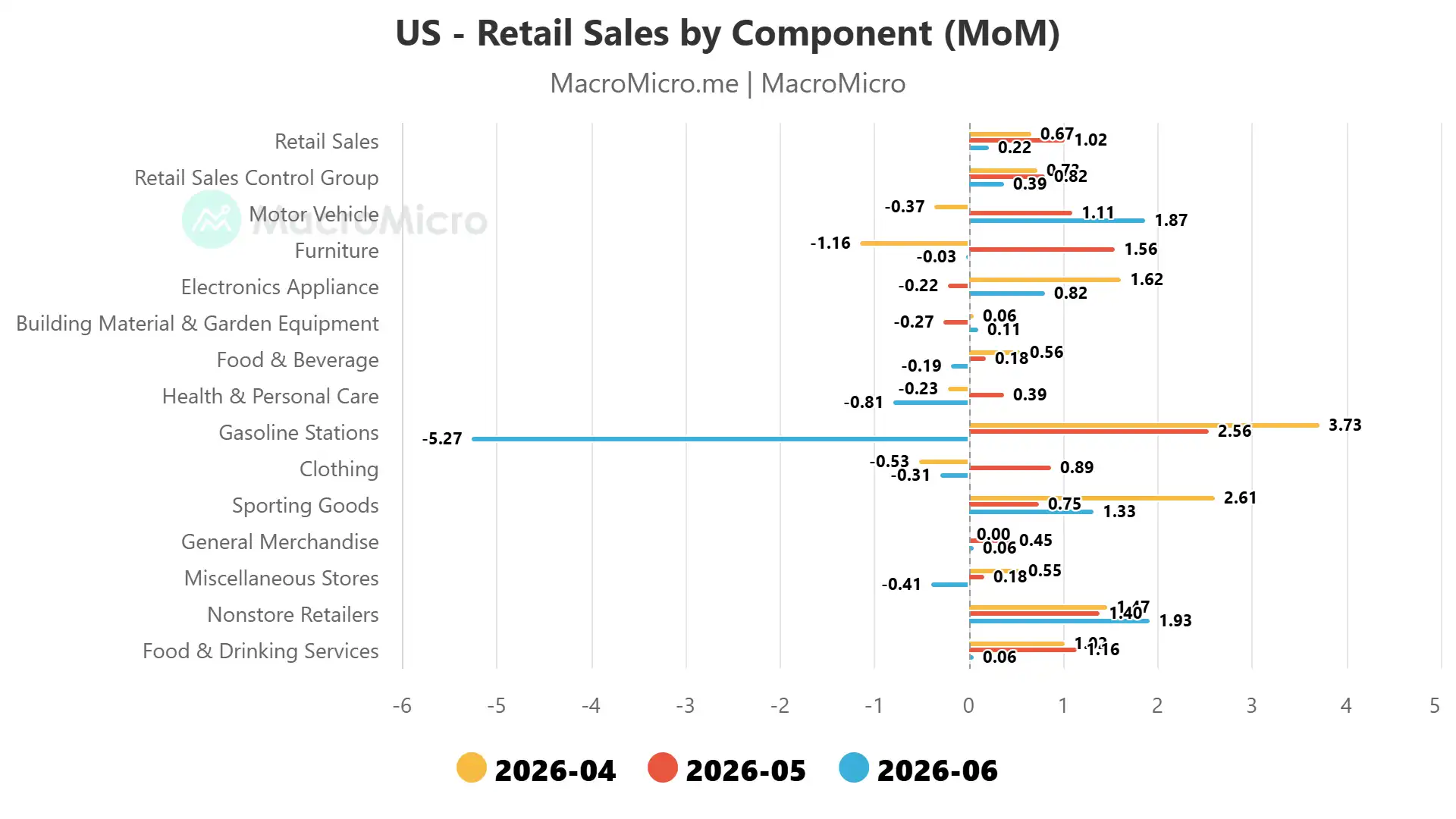

- Retail sales held up on the surface, but discretionary categories fell in ways cheaper fuel cannot explain

- A fresh read on consumer confidence may reveal whether households are worried about more than just the Iran war

The bellwether S&P 500 drifted lower, weighed down by its artificial intelligence (AI) names after an overnight meltdown in South Korea, a market that has become a barometer for the semiconductor boom. Even so, the move was soft rather than decisive, leaving the index inside the range that has boxed it in since mid-May. The more revealing action was in bonds, gold, and the dollar, which spent the week digesting a heavy run of data and came away leaning the same way.

Bonds and gold read the week differently than stocks

It was a crowded week: consumer and wholesale inflation reports, two days of congressional testimony from Federal Reserve Chair Kevin Warsh, and June’s retail sales figures. Treasury bonds whipsawed through all of it — knocked lower first by the oil spike from renewed Middle East fighting, then again by Warsh’s hawkish first-day remarks — before turning higher as softer data won out. Gold never even flinched, holding its range near $4000/oz and refusing to read the news as hawkish. The US dollar, firm at the start of the week, went soggy and slipped below the uptrend it had built since spring. The collective verdict points to a growth problem taking over from the inflation one.

A calm headline hiding a nervous consumer

Today’s retail sales report is a clear example. Receipts rose 0.2% on the month, exactly as expected, and easy to shrug off. The numbers are not adjusted for inflation, so with crude oil down more than 25% across May and June, cheaper gasoline alone dragged the total lower — sales at gas stations fell over 5%, echoing the drop in pump prices.

The internals are what raise eyebrows. In a month when the World Cup was drawing crowds across the country, spending on eating and drinking out stalled, alongside declines in clothing and personal care. Those are discretionary categories that cheaper fuel cannot explain, and their weakness carries the fingerprints of a consumer starting to get defensive. The same signature ran through the week’s inflation reports: consumer prices posted their first monthly drop since 2020, but strip out the plunge in energy and the softness bled into core services — the everyday spending that makes up the bulk of household budgets — rather than staying contained to fuel.

An economy leaning on the wrong engine

This is the risk that has been building in the growth data. First-quarter gross domestic product (GDP) rose 2.1%, only about half the pace of the quarters before last year’s government shutdown, and the heavy lifting came almost entirely from business investment, which expanded north of a 10% annualized rate on the data center boom. Consumption, at 68% of the economy against investment’s 14%, made its weakest contribution since early 2022 and has now retrenched for two straight quarters.

Forcing so small an engine to carry the economy means spinning it fast enough to throw off inflation that then settles into core services prices, squeezing the very consumer the economy ultimately depends on. Because consumption dwarfs investment by five to one, it would take only a modest further pullback by households to overwhelm the AI boom and drag growth into reverse. The pattern is already visible abroad: June’s S&P Global purchasing managers index (PMI) surveys show manufacturing expanding across Australia, the Eurozone, and the UK even as those economies shrink, their larger service sectors contracting under the same squeeze. The US has not arrived there, but this week’s data hints at early steps down that road.

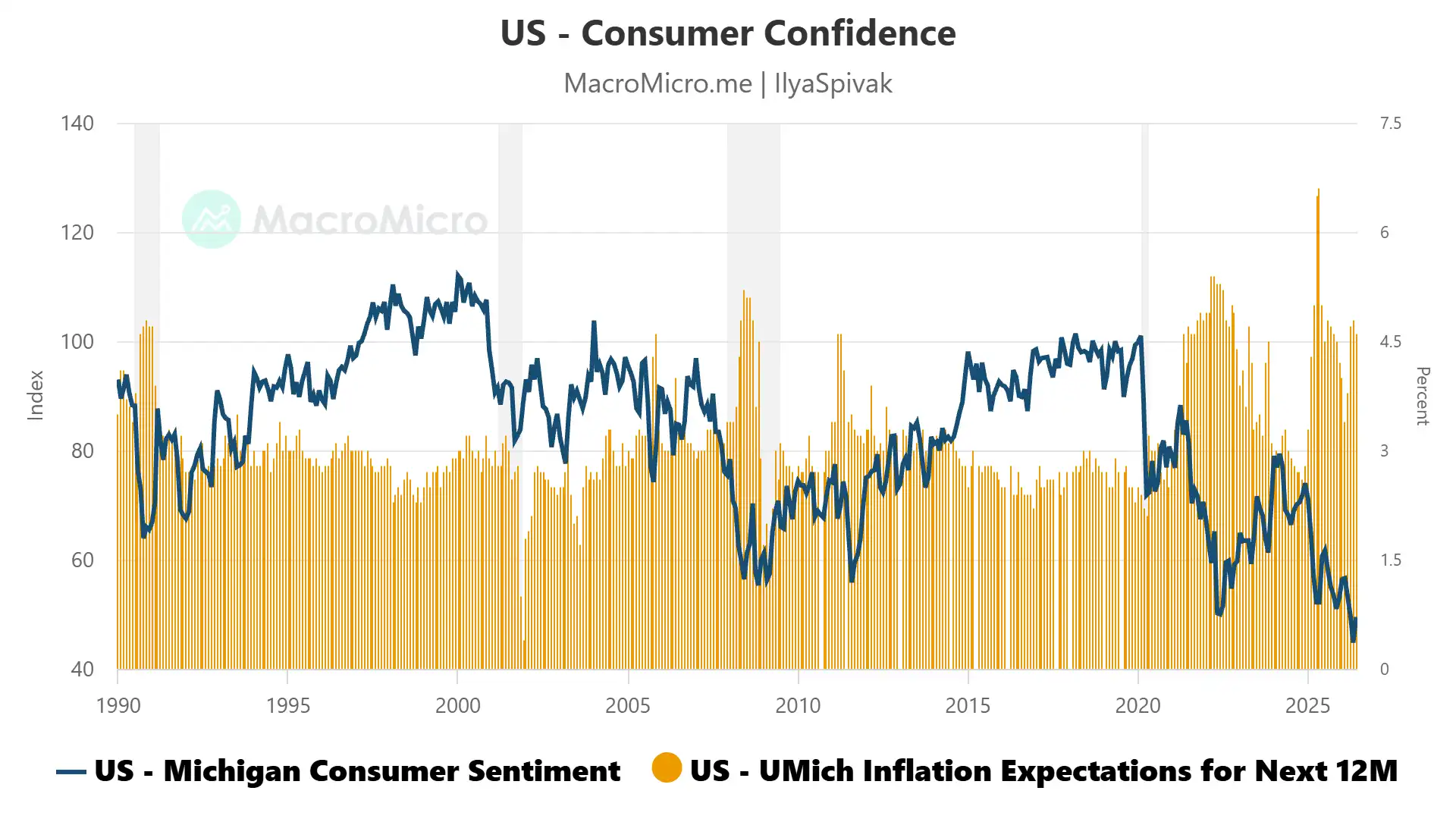

What consumer confidence data may confirm

July’s University of Michigan (UofM) consumer confidence survey is the next test, and the interplay between two of its readings is what matters. Oil has fallen and the market has clearly noticed, so the survey’s year-ahead inflation expectations should ease. The tell is whether sentiment rises in tandem. Confidence is seen barely off record lows near 51, and if cooling inflation still fails to lift the mood, that would suggest households are worried about something beyond gas prices, which is exactly what the rest of the week’s data began to whisper.

That is the fault line beneath a quiet market. Rate-hike pricing has already gone lukewarm, with a single move this year no longer treated as a lock and next year a wash. Should the confidence data confirm a consumer turning cautious for reasons deeper than the Iran war oil shock, the story stops being about how many hikes lie ahead. It becomes about a Fed still fixated on inflation while the economy slips beneath it — slow to cut, and late to the downturn. That is the scenario bonds and gold appear to be edging toward, and why the next real move in rates may end up being down. For a stock market clinging to its highs on an AI story already wobbling overseas, a consumer that quietly buckles would be the catalyst it has spent two months waiting to find.

Ilya Spivak, tastylive Head of Global Macro, has over 15 years of experience in trading strategy. He specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices