Micron Earnings Preview: The New Trillion Dollar Chip Stock

Micron Earnings Preview: The New Trillion Dollar Chip Stock

By:Mike Butler

Micron stock has surged over 756% in the past year, making MU one of the best-performing large-cap stocks of 2026, fueled entirely by insatiable AI infrastructure demand for its memory chips.

Both Micron and SK Hynix have reported their entire 2026 HBM production is completely sold out, driven by the explosive memory requirements of next-generation AI accelerators like Nvidia's Blackwell B200 GPU.

Analysts are forecasting Q3 EPS of $19.72 on revenue of $34.52 billion — representing year-over-year earnings growth of approximately 932% — with upward estimate revisions accelerating in the weeks leading into the June 24 report.

- Micron crossed a $1 trillion market cap for the first time in May 2026, sparking a broader debate about whether AI has permanently broken the memory industry's historic boom-bust cycle and whether today's record margins are structural or a peak.

- The key bear risk heading into earnings is a potential oversupply event in 2027–2028, as Micron, SK Hynix, and Samsung are all running massive simultaneous capital expenditure programs that could flood the market with new HBM capacity just as AI demand growth begins to moderate.

Micron Earnings Preview - June 2026

Micron Technology (NASDAQ: MU) has been one of the most explosive large-cap stories on Wall Street this year. MU has delivered a 756% change over the past year, with a 52-week range between $103.38 and $1,204.50 as of today, June 22nd. Shares have more than tripled year to date, and the stock surged 19% in a single session in late May after UBS nearly tripled its price target from $535 to $1,625, citing long-term supply agreements with partially fixed pricing. The stock has been added to the S&P 100 and has become a bellwether for the entire AI infrastructure trade, with retail and institutional investors alike piling in ahead of Tuesday's print.

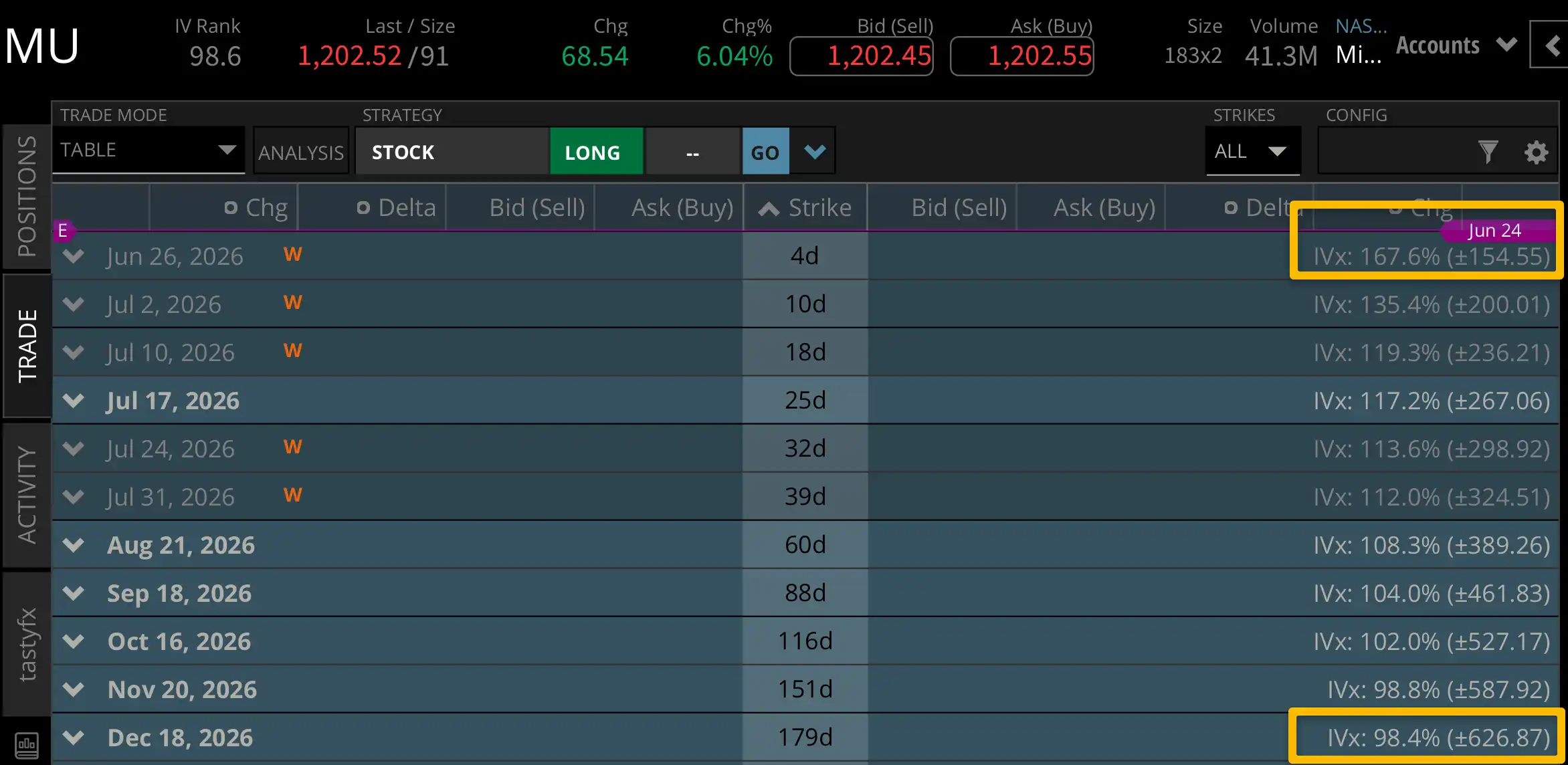

Micron's implied volatility landscape is extremely high for the earnings announcement itself, but also through the end of the year. This week's expected move is 13% of the notional value of the stock price, which is very high for any company reporting earnings. What's even more interesting is that the EOY expected move through December 2026 is over $600 - that's half the stock price right now - massive implied volatility indicates uncertainty in the future price of the stock. Expect nothing but fireworks for Wednesday's announcement.

Micron AI Memory Boom

The fundamental story behind MU's surge is straightforward: AI needs memory, and Micron makes it. Revenue grew from $6.8 billion in Q3 fiscal 2024 to $23.9 billion in Q2 fiscal 2026 — a pace few large-cap technology companies have matched — driven largely by high-bandwidth memory, the specialized DRAM designed to sit beside AI processors and deliver data far faster than standard chips. CEO Sanjay Mehrotra stated in March that NAND demand is "significantly in excess of available supply for the foreseeable future" and that both AI and conventional servers face a "lack of adequate DRAM and NAND supply." Importantly, Micron has also begun shifting from spot-price memory sales to multi-year supply agreements at pre-agreed pricing — a move away from commodity economics toward infrastructure-style pricing.

Micron's HBM Sold Out Through 2026 — What It Means for AI Chip Supply

The supply-demand imbalance in HBM is unlike anything the memory industry has seen in recent cycles. Both SK Hynix and Micron have reported their entire 2026 HBM production is sold out — a situation driven in part by the escalating memory requirements of AI models. Nvidia's Blackwell B200 GPU uses 192GB of HBM3E, a 140% increase from the H100's 80GB, and that rapid growth in memory per chip, multiplied across millions of units, has created a demand surge that manufacturing simply cannot keep up with. Goldman Sachs has pegged the 2026 DRAM supply-demand gap at 4.9%, describing it as the most severe shortage in 15 years. For consumers, this tightness isn't just an investor story — it is the reason RAM and DDR5 prices in laptops and PCs have continued to climb.

Micron Crosses $1 Trillion in Market Cap: Is the Memory Cycle Finally Broken?

For decades, Micron was considered one of the most cyclical stocks in technology — a company where margins could swing violently from negative territory to record highs and back. That narrative is now being challenged. Micron topped a $1 trillion market value for the first time in late May, with investors snapping up stocks tied to memory and processing needed to run agentic AI workloads — a battleground once dominated solely by Nvidia. Gross margins reached 75% in Q2 FY2026 — roughly triple what Micron reported in 2024 — with Q3 guidance pointing to 81%, driven by the pricing power that comes from being one of only three companies on earth that produce essentially all of the world's DRAM and NAND. Whether those margins represent a permanent structural shift or a cycle peak is the defining question heading into Tuesday's report.

Bullish Case for Micron Earnings

The bull case rests on durability, not just momentum. Analyst EPS estimates have surged 68.1% over the past 90 days — from $11.73 to a current consensus of $19.72 — a sustained upward revision pattern signaling that analysts have been scrambling to keep pace with improving fundamentals. For full fiscal 2026, analysts project EPS of $57.71, up 651% from $7.68 in fiscal 2025, with further growth to $97.77 expected in fiscal 2027. Bulls also point to Micron's transition into multi-year HBM supply contracts, its growing role in Nvidia's Vera Rubin platform, and a new strategic partnership with Anthropic as evidence that this is structural demand, not a speculative spike. Several major firms including RBC Capital, Cantor Fitzgerald, and Wedbush have sharply raised price targets in the week leading into earnings.

Bearish Case for Micron Earnings

Bears aren't dismissing Micron's growth — they're questioning its durability. Samsung, SK Hynix, and Micron are engaged in a massive simultaneous capital expenditure race, with Micron alone spending over $25 billion in FY2026. Synchronized capacity expansion at that scale could lead to an oversupply situation when new fabs come online in 2027 and 2028, causing a sharp drop in average selling prices and margins from current peaks. Goldman Sachs remains a notable outlier with a price target near $400, warning that memory remains cyclical and that today's margins represent a peak, not a floor. With the stock priced for perfection heading into the report, even a slight miss in forward guidance — particularly around HBM volume or Q4 margin expectations — could trigger a swift and painful selloff.

Mike Butler, tastylive director of market intelligence, has been trading the markets for a decade. He appears on Options Trading Concepts Live, Monday-Friday. @tradermikeyb

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices