Netflix Earnings Preview: A Make-or-Break Quarter for a Beaten-Down Stock

Netflix Earnings Preview: A Make-or-Break Quarter for a Beaten-Down Stock

By:Mike Butler

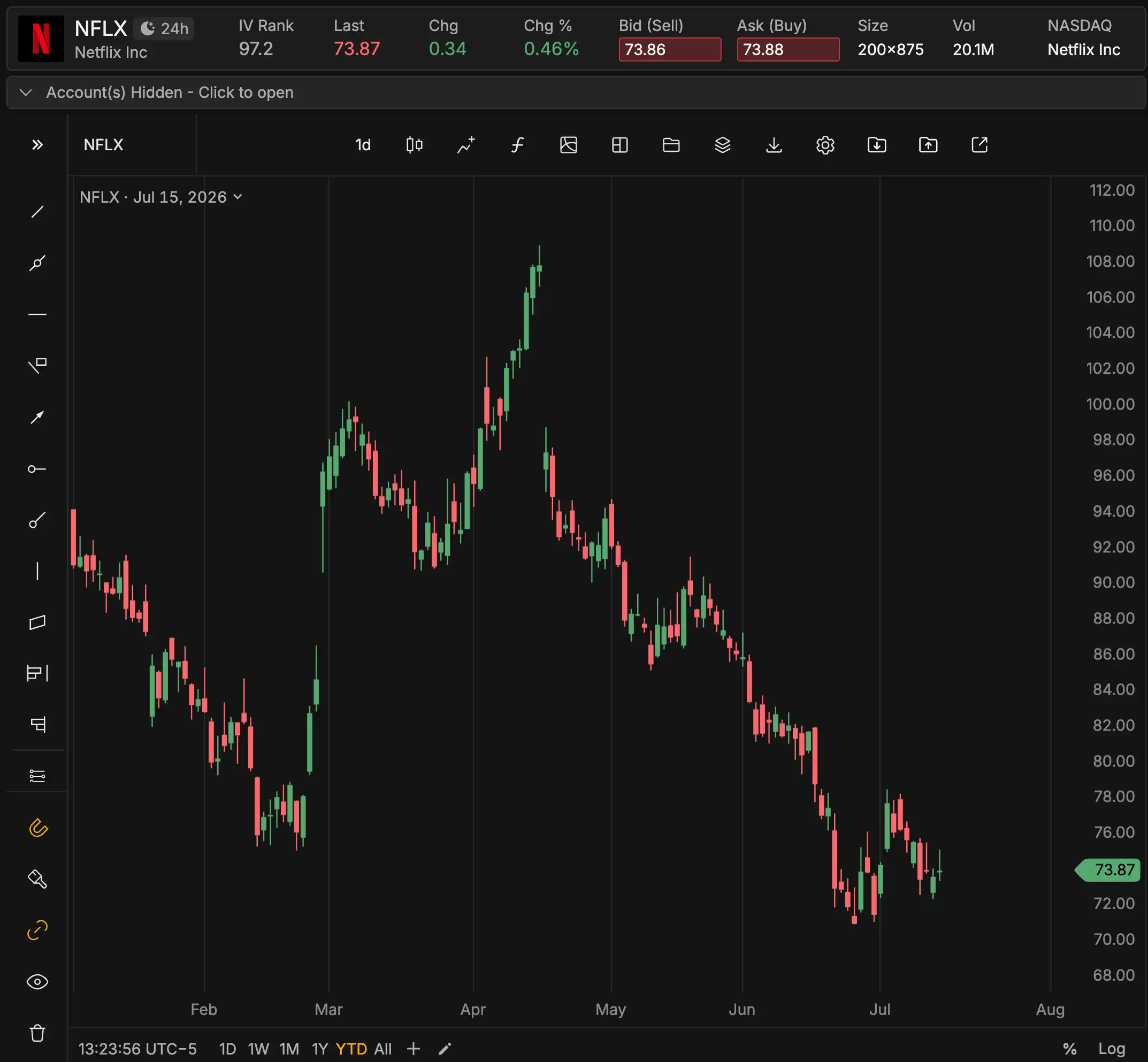

Netflix (NASDAQ: NFLX) reports second-quarter 2026 results on Thursday, July 16, after the closing bell, in what may be the most closely watched print of the streaming giant's year. The stock enters earnings down roughly 24% in the first half of 2026 and down more than 40% over the past 12 months, a sharp reversal for a name that traded above $1,100 a share before its 10-for-1 stock split took effect in November 2025.

Shares closed at $73.83 on July 13, well off their post-split high of $127.75 and hovering just above their 52-week low of $70.86. That decline has come even as Netflix's underlying business has kept growing, which is part of what makes Thursday's report so pivotal: investors want to know whether the stock's slide reflects a genuine business slowdown or simply a valuation reset after a run that took the price-to-earnings multiple as high as 63 last year.

Netflix Earnings Preview: What Analysts Expect

Consensus estimates call for:

EPS: $0.79, up modestly from a year ago on a comparable basis (the prior-year comp is complicated by unusual tax items)

Revenue: Approximately $12.57 billion, up 13.5% to 13.8% year-over-year

Operating margin: Management has guided to roughly 32.6% for the quarter, part of a 31.5% full-year target

For context, Netflix beat estimates comfortably last quarter, with Q1 2026 EPS of $1.23 topping the $0.79 consensus and revenue of about $12.25 billion edging past estimates, yet the stock still struggled to hold gains. That pattern, a fundamental beat that fails to translate into a sustained rally, is exactly what bulls are hoping doesn't repeat itself this time.

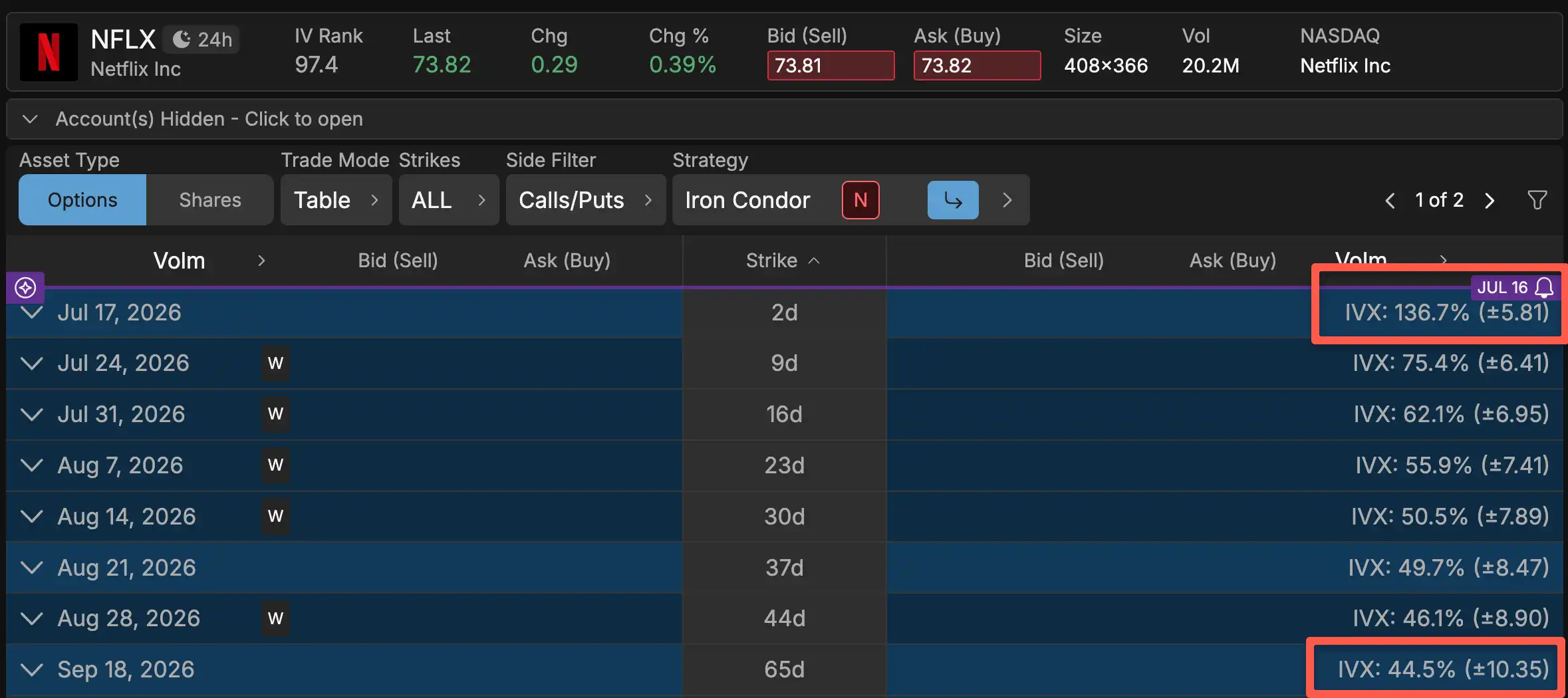

The implied volatility for NFLX is quite high, with an implied weekly move of +-$5.81 against the current stock price of $73. This is about 8% of the notional value of the stock price, which puts NFLX earnings on the higher end of the implied ranges we typically see between 5-10% of notional value. Looking further to September 2026, we only see a +-$10.35 implied move, meaning a lot of the implied volatility for this earnings announcement encompasses the expected move through September - an ominous sign for potential volatility ahead.

Ahead of Earnings, Wall Street Is Trimming Price Targets

The run-up to this report has been unusually cautious for a stock that spent most of 2025 as a market darling. In the past week, Morgan Stanley cut its price target to $90 from $115, Bernstein lowered its target to $100 from $110, and Citi and HSBC made similar reductions, even as most of these firms kept positive ratings on the stock. KeyBanc has framed the quarter as likely to be "largely in line," neither a blowout nor a disaster.

That combination, price target cuts alongside maintained buy ratings, suggests analysts see the recent selloff as more about sentiment and valuation than a broken growth story. Options traders appear to agree: bullish positioning has picked up heading into the print, and retail investor interest in the stock has reportedly increased in recent days.

The Warner Bros. Discovery Hangover

No discussion of Netflix's 2026 is complete without the Warner Bros. Discovery saga. Netflix entered a bidding war for the media conglomerate's studio and streaming assets, ultimately losing out to Paramount Skydance in a deal reportedly worth around $111 billion. The failed pursuit weighed on sentiment for months, and while Netflix has since pivoted back to messaging around disciplined capital allocation and organic growth, some investors still view the episode as a distraction that cost the company both time and credibility with the market.

Management has indicated the termination fee from the collapsed deal is actually padding free cash flow this year, with full-year 2026 free cash flow guidance raised to approximately $12.5 billion from a prior estimate of $11 billion. Whether investors view that as a genuine silver lining or a one-time accounting footnote will likely come up on the earnings call.

Advertising Growth and the Subscriber Question

Netflix's advertising business remains one of the more concrete bright spots in the bull case. Ad revenue is expected to roughly double year-over-year to approximately $3 billion for full-year 2026, with the ad-supported tier now reportedly reaching around 190 million monthly active viewers globally. That expansion has been aided by price increases across subscription tiers in major markets earlier this year.

One wrinkle for this report: Netflix discontinued regular quarterly membership disclosures after Q1 2026, so there is no official consensus subscriber estimate for analysts to measure against. That makes engagement metrics, average revenue per member, and management commentary on retention more important than usual. Recent reporting suggests Netflix has flagged early signs of softening engagement even as churn remains low, which is part of why the company is testing new content formats, including curated short and mid-form video from publishers like BuzzFeed, Condé Nast, and Hearst rolling out across its platform starting in early August.

Bullish Case for Netflix Earnings

The bull case rests on the idea that Netflix's core business has not actually broken, even if the stock has. Revenue growth in the mid-teens percentage range remains healthy for a company of Netflix's scale, and the advertising business is scaling quickly toward a $3 billion annual run rate with room to keep growing as more markets and more ad inventory come online. Free cash flow guidance has been raised, not cut, and the balance sheet benefits from the terminated Warner Bros. Discovery deal rather than being burdened by a costly acquisition. Netflix also continues to produce some of the most-watched original content in the industry, giving it pricing power that has already shown up in this year's tier price increases. With the stock trading at a historically low valuation relative to its own recent history and several analysts maintaining buy ratings even after cutting price targets, bulls argue that a clean quarter Thursday, paired with reassuring commentary on engagement and the ad business, could be the catalyst that stops the bleeding and starts a re-rating higher.

Bearish Case for Netflix Earnings

The bear case centers on the fact that Netflix's stock has fallen for months despite generally solid headline numbers, which suggests the market is worried about something beyond the immediate quarter. Chief among those worries is engagement. If subscribers are spending less time on the platform even while churn stays low, that is often an early warning sign that shows up in slower growth or weaker pricing power down the road, and Netflix's decision to stop reporting subscriber counts makes it harder for investors to verify the underlying trend in real time. The Warner Bros. Discovery bidding war, while ultimately unconsummated, cost Netflix months of strategic focus and invited questions about capital discipline that still linger. Competition from Disney+, Amazon, and other streaming and short-form platforms continues to intensify, and Netflix's move into curated third-party short-form content is itself an acknowledgment that traditional long-form bingeing may not be enough to hold attention going forward. With the stock still carrying a premium valuation relative to legacy media peers and multiple analysts cutting price targets just days before the print, a guidance disappointment, particularly on engagement or back-half margin trends, could extend the stock's slide rather than mark its bottom.

Mike Butler, tastylive director of market intelligence, has been trading the markets for a decade. He appears on the tastylive morning show Monday - Friday. @tradermikeyb

For live daily programming, market news and commentary, visit tastylive or the YouTube channel tastylive (for options traders).

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices