FOMC Minutes: Why is the Fed More Worried Than the Markets?

FOMC Minutes: Why is the Fed More Worried Than the Markets?

By:Ilya Spivak

Why is the Fed skeptical as stock markets cheer? FOMC meeting minutes may have the answer.

- The Fed has become more despondent about tariffs amid policy standstill.

- Markets are decidedly cheerier, with US stocks erasing most 2025 losses.

- Minutes from May’s FOMC meeting may shed some light on this disparity.

The Federal Reserve has pointedly excused itself from passing judgement on what the trade war triggered by President Donald Trump will mean for the economy, and thereby for monetary policy. Traders will now be keen to gauge whether policymakers’ views started to tilt toward a clearer bias after April’s tariff-inspired fireworks.

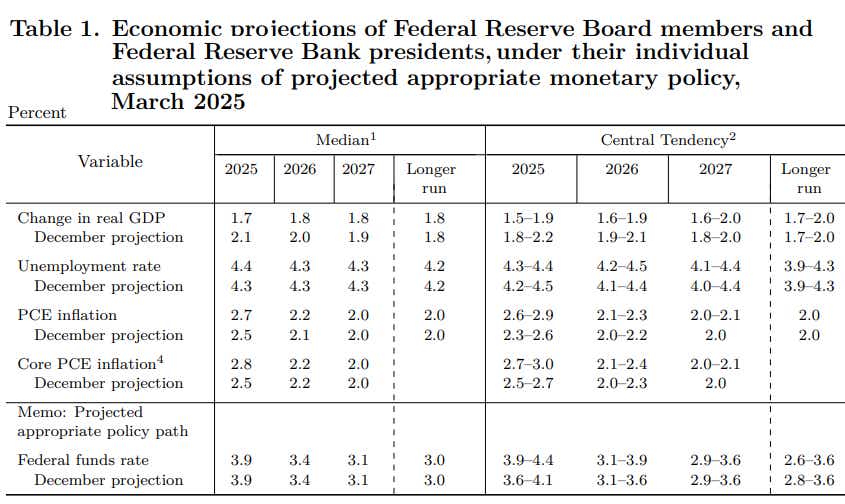

In March, the U.S. central bank threw up its hands as the White House began to announce a flurry of tariff hikes. Fed Chair Jerome Powell explained that tariffs typically boost inflation and depress growth, but there was no knowing how this particular episode will play out. With the jobless rate relatively low and inflation steady, it was time to wait.

US tariff policy has confounded the Federal Reserve

This message was broadly unchanged after the rate-setting Federal Open Market Committee (FOMC) met in early May. Powell’s tone had sharpened at the post-meeting press conference, however. He pointed squarely at the tariffs as threatening to put at odds the Fed’s employment and price stability objectives. He said “stagflation” aloud.

Updated language in the FOMC policy statement signaled that Powell’s feisty display was not a one-man act. Rather, it channeled the mood among officials. It was blunt, saying the committee “judges that the risks of higher unemployment and higher inflation have risen.”

By the time the FOMC gathered for May’s conclave, the bellwether S&P 500 stock index had already rallied as much as 18.5% from the panic lows set a month earlier. Wall Street had erased over 60% of the selloff from mid-February, triggered by worries about the tariffs’ economic consequences and culminating in early April’s “Liberation Day” panic.

May FOMC meeting minutes: what’s the Fed really afraid of?

Policymakers’ sour mood seems to have been clearly at odds with this exuberance in financial markets. With the release of minutes from May’s meeting, traders will want to see whether there’s more to this than the typical timeline mismatch between the markets’ more volatile reaction function and the central bank’s longer-view approach.

As it stands, the markets are pricing in 95 basis points (bps) in rate cuts between now and the end of next year. 44bps are priced into benchmark Fed Funds futures for 2025 and 52bps for 2026. This broadly lines up with the Fed’s guesstimate of 50bps apiece. The first cut this year has been pushed back to September.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts #Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit #tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices