US CPI: Are Stock Markets Immune as the Iran War Fuels Inflation?

US CPI: Are Stock Markets Immune as the Iran War Fuels Inflation?

By:Ilya Spivak

Will US inflation data challenge the low-volume AI melt-up carrying the stock market to record highs?

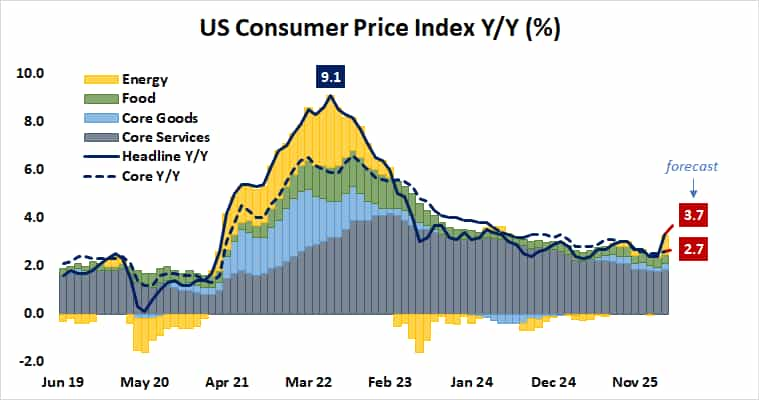

- Headline US CPI is slated to rise to 3.7% y/y in April, the highest since May 2024

- The full impact of the US-Iran war energy price shock has yet to land in the data

- Stock markets may finally face gravity if inflation fears pop the AI capex melt-up

Last week’s US jobs report came in modestly better than expected, but the major asset benchmarks barely moved out of their recent ranges. From here, the earnings calendar is thin until Nvidia (NVDA) reports next week, allowing traders’ attention to remain on macro forces. Incoming US consumer price index (CPI) data is the next clean test of whether the narrow rally carrying stocks higher can withstand the inflation fears that other markets have wrestled with for weeks.

The stock market surge is really just a single trade

The bellwether S&P 500 set yet another record high, but the technical issues flagged since last week persist. Trading volumes have shrunk throughout the rebound from the wartime selloff. The relative strength index (RSI) momentum indicator has tellingly flatlined even as prices set higher highs, warning that markets’ upward thrust may be waning.

Tellingly, the equal-weighted S&P 500 (ETF: RSP) has lagged meaningfully behind and remains pinned below February’s highs. The tech sector is outperforming by leaps and bounds, so much so that it seems singularly responsible for Wall Street’s rosy disposition.

A look under the surface revels a picture that is still more skewed. The equal-weighted Nasdaq 100 (ETF: QQEW) is up just 2.2% for the year. The “magnificent seven” mega-cap tech stocks (ETF: MAGS) are up 6.3%. Software companies (ETF: IGV) – seen as especially exposed to disruption from artificial intelligence (AI) – are down nearly 12%.

Nevertheless, the headline Nasdaq 100 index is up 15%. The force lifting the benchmarks is rosy optimism about semiconductors and the AI hardware stack — GPU, CPU, and memory makers (ETF: SMH) are up more than 54% year-to-date. This is not a broad bull market but a single, narrow trade.

Other markets are still trading the war

Meanwhile, crude oil remains pinned near the middle of its wartime range. It has been up as much as 68% above pre-war levels at the peak of the panic and as little as 23% more expensive at the most recent conflict low. It seems that energy costs are now stuck materially higher than they were before the US and Israel struck Iran in late February.

Treasury bond prices have slid back to test wartime lows, and yields are sharply higher. Gold is tiptoeing lower and the US dollar is consolidating after retracing about half its wartime gains. Bitcoin continues to appear disconnected from the broader macro narrative. It is meandering higher.

The AI buildout engine versus the consumer

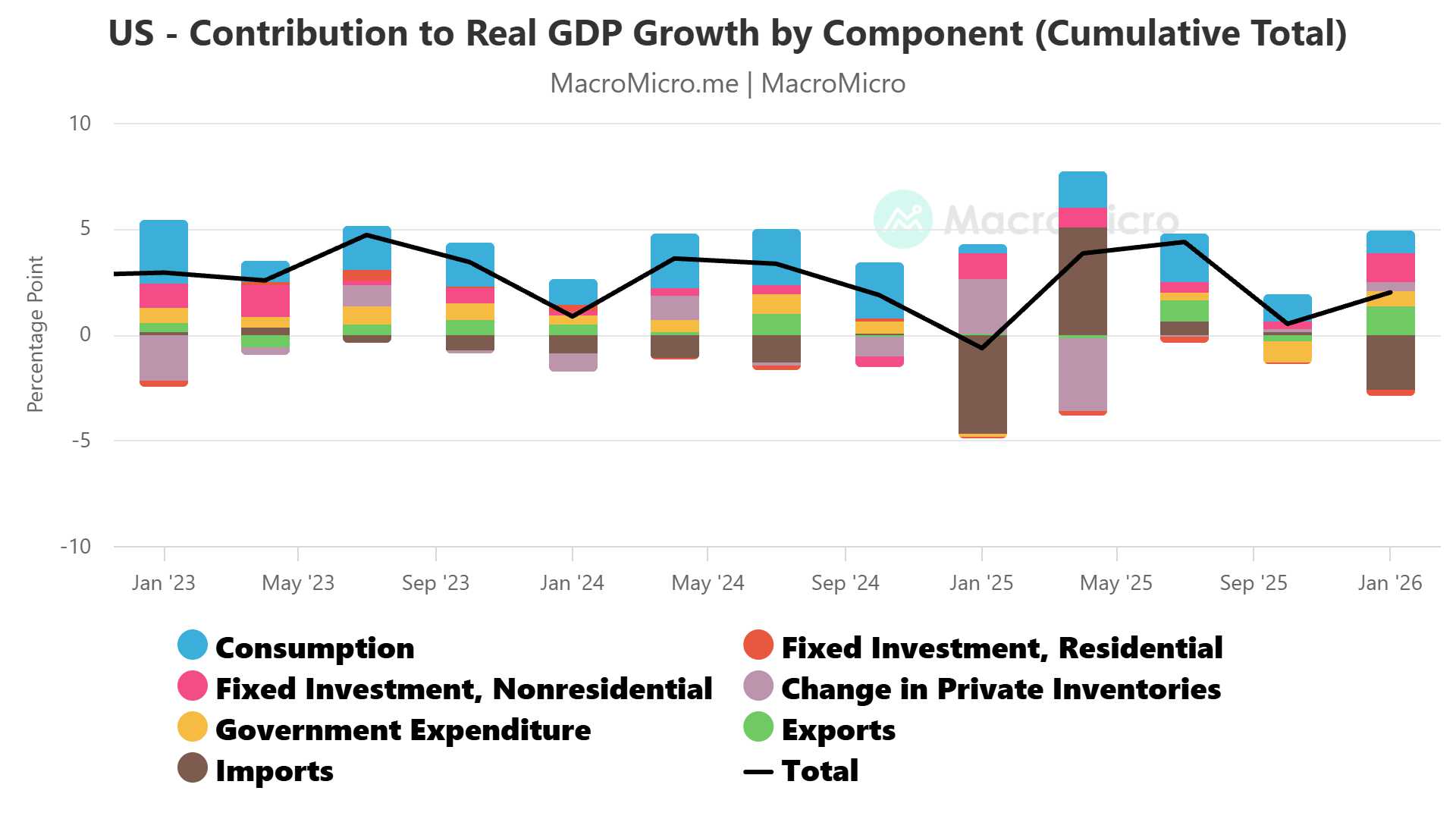

Despite being narrow, the stock market rally has fundamental underpinnings. First-quarter US gross domestic product (GDP) showed fixed nonresidential investment contributing 1.39 percentage points (ppt) to the 2% headline growth figure, edging out consumption at 1.08ppt.

That’s nothing short of staggering. Consumption is 68% of GDP while nonresidential investment is just 14%. However, business investment grew at a blistering annualized rate of 10.4% while consumer spending expanded at just 1.6%, slowing for a second straight quarter and lagging the growth rate pf GDP itself.

Wall Street optimism seems to rest on more of the same ahead. AI infrastructure capex this year is set to nearly double that of last year as traffic to the top models grows aggressively. However, fading stock market trading volumes warn that the story may soon run out of incremental buyers even as thin liquidity makes prices easier to push around.

From here, data center builders and consumers face the same headwinds. The US-Iran conflict has driven economic policy uncertainty to its highest in at least a decade. Shipping costs are dramatically elevated, energy is materially more expensive, and bottlenecks in critical inputs are mounting.

Consumers are already groaning, and the vulnerability of the AI buildout to the same headwinds is increasingly glaring. About 40% of data center projects originally slated for 2026 are now expected to slip into 2027 or beyond. It will be devilishly hard for a 14% slice of GDP to keep outpacing the 68% one if both are hobbled at once.

Why April’s US CPI inflation data matters

Core inflation was already perking up before the war’s energy shock. Goods prices have been firming for months, services inflation has been posting its strongest monthly gains since mid-2025, and housing prices printed the biggest rise in four months in March.

Bond markets have been pricing this in for weeks, with the spread between 5-year and 10-year breakeven inflation rates widening sharply. Central bank policy bets have followed suit.

The European Central Bank (ECB) is now seen delivering three 25-basis-point (bps) rate hikes in 2026, after starting the year with expectations of standstill. The Bank of England (BOE) is on track for at least two hikes, after being priced for 50bps of cuts pre-war. A similar call for easing at the Federal Reserve has been jettisoned in favor of standstill. The Reserve Bank of Australia (RBA) is set for a fourth hike before year-end after already delivering three of them.

The full Middle East energy shock is still ahead: crude oil moves filter into headline CPI with a roughly one-month lag, meaning March’s war-driven surge should begin to appear in earnest in April data. It is possible that even the consensus 3.7% year-on-year headline CPI growth reading may prove to be understated.

A hotter print would crystallize the inflation worries on display in markets outside equities, setting the stage for an unwelcome squeeze of consumers and data center builders alike. Against this backdrop, the narrow chip stock melt-up rally may finally meet the gravity it has spent weeks defying.

Ilya Spivak, tastylive Head of Global Macro, has over 15 years of experience in trading strategy. He specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices