Will the Stock Market Care as Brutal Inflation Hits Consumers?

Will the Stock Market Care as Brutal Inflation Hits Consumers?

By:Ilya Spivak

Stock markets have ignored inflation fears amid the AI buildout frenzy. Will retail sales data finally rouse them?

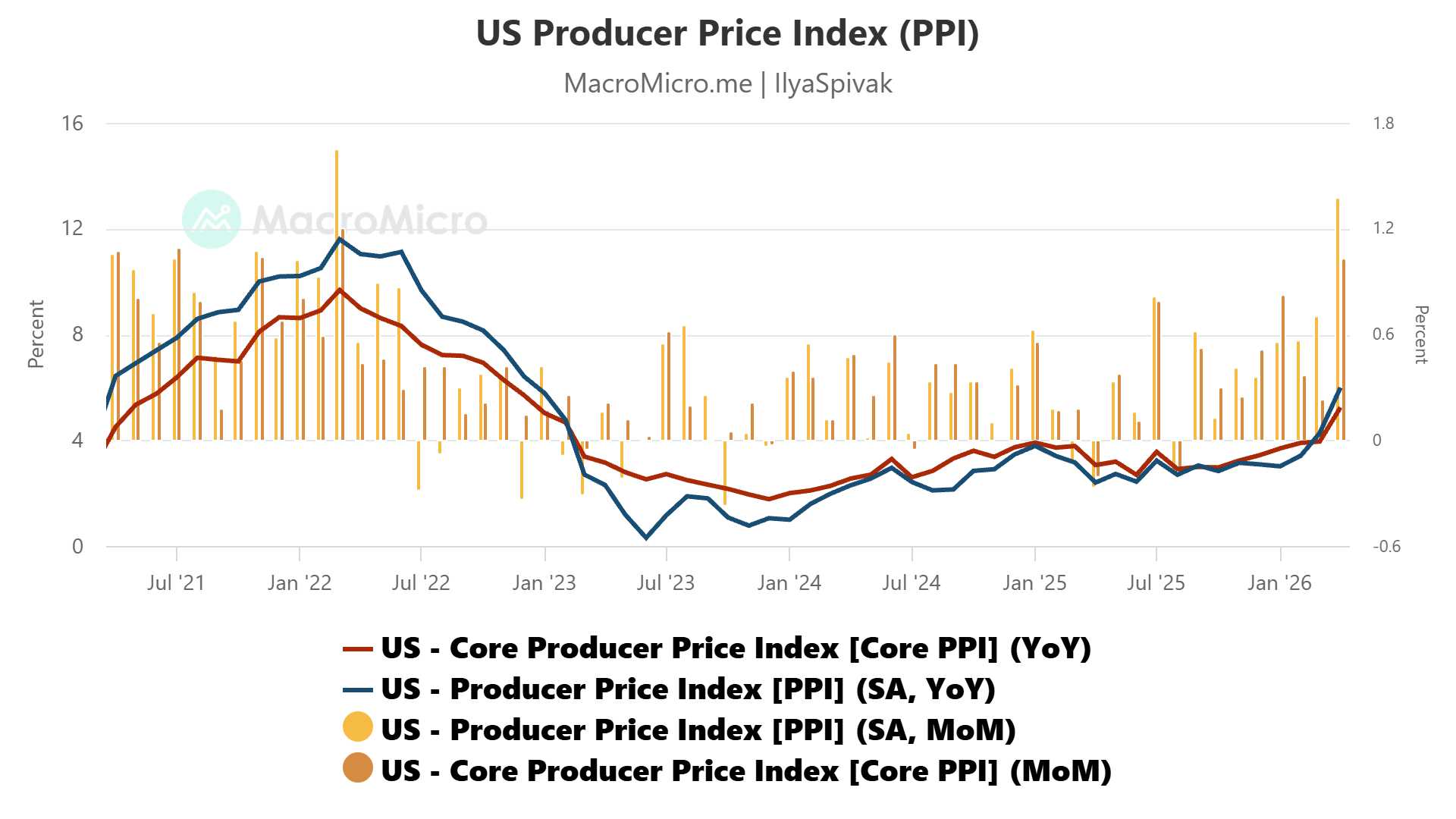

- US PPI data put wholesale inflation at 6% y/y in April, the highest since December 2022

- The energy price shock is now spilling into transportation, warehousing, and margins

- Can stock markets look the other way if April’s retail sales data shows consumers buckling?

US wholesale inflation surged in April to its highest level in over three years, dramatically overshooting expectations. The shock comes one day after a hotter-than-forecast consumer inflation print, and on the eve of an April retail sales report set to show whether US shoppers are still holding up. A narrow chip-stock melt-up continued on Wall Street, setting fresh record highs even as every other major markets priced in a worsening squeeze on the economy.

Wholesale inflation is no longer just an energy story

Headline producer price index (PPI) data showed wholesale inflation rose to 6% year-on-year in April, well above the 4.9% expected by economists and the highest reading since December 2022. The core measure stripping out food and energy rose also hit the highest in over three years, rising to 5.2% year-on-year and topping the 4.3% consensus.

On its surface, the headline number tells a familiar US-Iran war story. Crude oil moves filter into inflation gauges with a roughly one-month lag, and West Texas Intermediate (WTI) crude is still pinned near $101 a barrel, near the middle of its wartime range. Goods PPI was unsurprisingly driven by surging fuel costs from jet fuel to gasoline.

The worrying part is on the services side. The biggest jump was in transportation and warehousing services, up north of 12% year-on-year. That captures the cost of moving goods from where they arrive or are made to where they are sold — cost pressure much closer to the consumer than the wellhead.

Trade services, essentially wholesaler margins, also expanded sharply, with the bulk of the move tied to selling petroleum, fuels, and lubricants. In other words, the Iran war oil price shock is no longer just an energy line item. It is spilling into the costs of nearly everything energy touches.

The CPI picture confirms inflation spillover

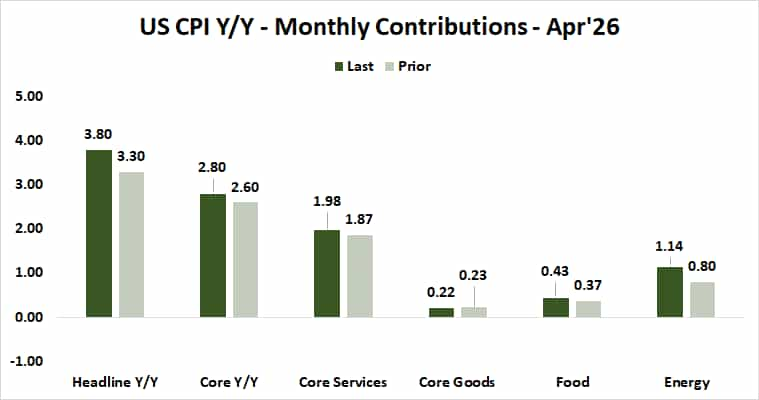

This follows April’s headline US consumer price index (CPI) reading at 3.8% year-on-year, which also overshot expectations at 3.7% and marked the highest reading since late 2023. Core CPI came in at 2.8%, beating consensus at 2.7%.

Energy was again the standout, but the worrying pattern is that service-sector costs outside food and energy grew faster too. Core services inflation is showing the same signs of spillover as PPI. Tellingly, the biggest uplift came from transportation.

Bond markets have been pricing in these risks for weeks. The spread between 5- and 10-year breakeven inflation rates was virtually nonexistent at the start of the year and has widened sharply, signaling traders are looking beyond the immediate spike in oil prices to inflation that stubbornly builds over a longer time horizon. With WTI still locked in its wartime range despite a supposed ceasefire, that impulse looks unlikely to fade soon.

Retail sales data will test the US consumer

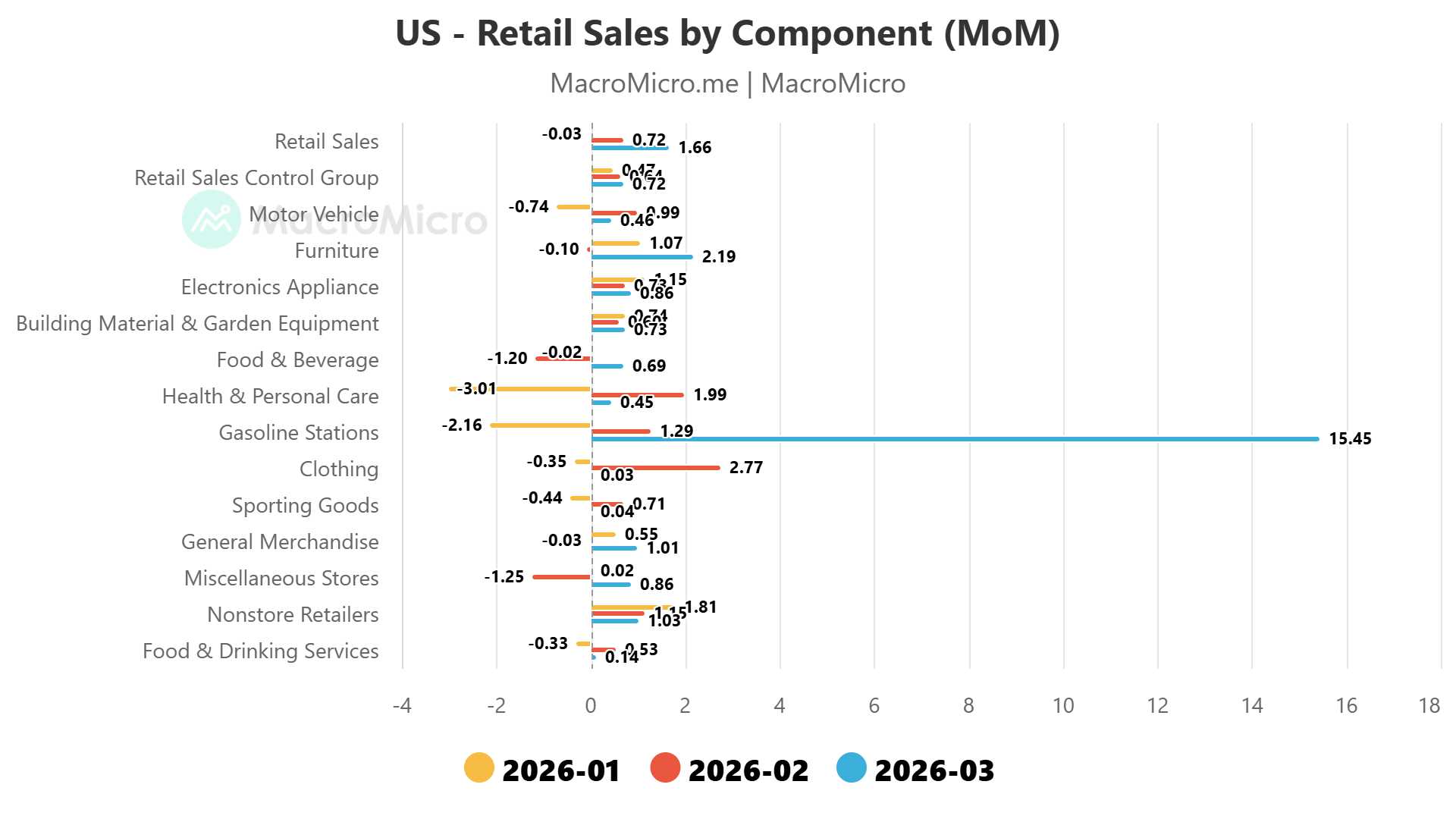

The April retail sales report is the next clean read on whether the consumer is bending under all of this pressure. The consensus calls for a modest 0.5% monthly rise after March’s much stronger 1.7% jump. That bounce was unhelpfully inflated by an almost 15.5% surge in gas station sales. This was a display of the oil price shock expressed in dollar terms rather than a genuine burst of demand strength.

The backdrop is unforgiving. First-quarter US gross domestic product (GDP) data showed consumption — a meaty 68% slice of total output — grew at meager annual rate of 1.6%, weaker than GDP itself at 2% and slowing for a second consecutive quarter.

Meanwhile, the Federal Reserve and other major central banks have abandoned any near-term hope of rate cuts. The US central bank looks the most dovish of the bunch and is priced for policy standstill this year. Before the war, traders were primed for 50 basis points (bps) of easing. The Bank of England (BOE) and the European Central Bank (ECB) are now slated for hikes, and the Reserve Bank of Australia (RBA) is penciled for four rate hikes instead of just two previously.

That means consumers are facing a sustained squeeze with no monetary policy relief in sight. Whatever growth shock arrives will be allowed to develop until it does enough damage to beat back prices and justify cuts. That looks like a high bar given how stuck the inflation picture looks.

The chip-stock melt-up is asking a lot

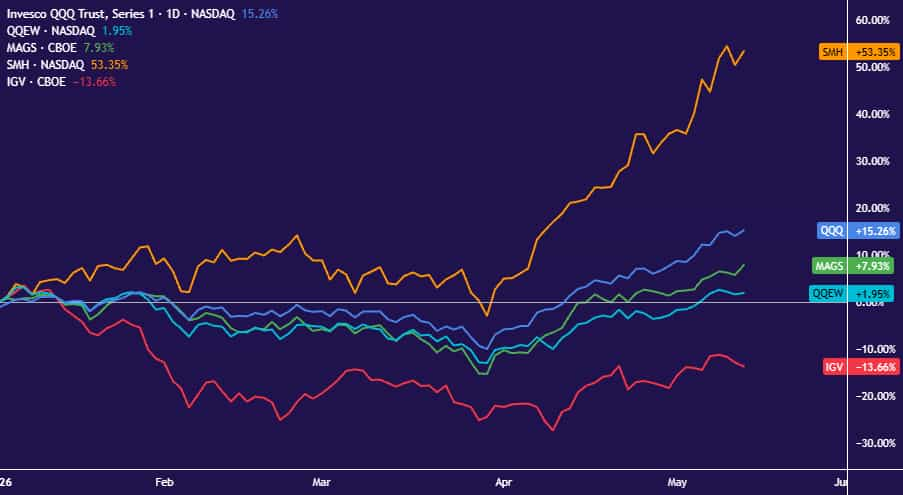

Stocks are still pushing higher into all of this. The bellwether S&P 500 set another record today, but the technical issues flagged two weeks ago persist. Trading volumes have shrunk throughout the rebound from the wartime selloff. The headline Nasdaq is up over 15% year-to-date, but the equal-weighted version is up just 2%. The magnificent seven mega-caps are up only 8%. Software companies exposed to artificial intelligence (AI) disruption are down close to 14%. The singular force lifting the indexes is semiconductors, up more than 53% year-to-date.

The fundamental case for that move rests on that same first-quarter GDP data showing fixed nonresidential investment contributing 1.39 percentage points (ppt) to the 2% growth headline, edging out consumption at 1.08ppt despite the latter being five times larger as a share of the economy. Business investment grew at a blistering annual rate of 10.4% however, outpacing consumption more than sixfold. Stock markets seem to be betting that this composition can persist — that the AI building frenzy can burn hot enough to offset retreating consumers.

And yet, the same headwinds bedevil data center builders and consumers alike: higher oil prices, dramatically elevated transport costs, mounting bottlenecks for key inputs, and a murky outlook for economic policy. A gauge measuring that uncertainty based on analysis of the news articles is at the highest in about four decades.

Close to 40% of data center projects originally slated for 2026 have already been reported as delayed into 2027 and beyond. It will be devilishly hard for business investment’s 14% slice of GDP to keep outpacing consumption’s 68% - by far the lion’s share – if both are being hobbled simultaneously.

If April’s retail sales report suggests that consumers are buckling — especially if demand looks weak even after gas station sales are stripped out — stock markets may find the economic backdrop harder to ignore. The melt-up has been running on fading trading volumes for weeks. Thin liquidity makes prices easier to push around in either direction. If the data demands Wall Street to rethink its ways, the about-face that follows may be a violent affair.

Ilya Spivak, tastylive Head of Global Macro, has over 15 years of experience in trading strategy. He specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices