Stocks and US Dollar at Risk as Markets Push Back Fed Rate Cuts

Stocks and US Dollar at Risk as Markets Push Back Fed Rate Cuts

By:Ilya Spivak

Markets are pushing back Fed rate cut expectations. That may spell trouble for stocks and the dollar.

- The Fed is firmly locked in wait-and-see mode, May FOMC minutes show.

- Markets seem no more certain of the economic outlook as key data looms.

- Repricing for a longer stimulus delay may punish stocks and the US dollar.

The Federal Reserve “well positioned to wait for more clarity” on inflation and the economy before acting on interest rates, according to minutes from May’s meeting of the central bank’s policy-steering Federal Open Market Committee (FOMC). Officials warned that uncertainty about the economic outlook is unusually elevated.

Participants in the conclave agreed that risks of higher inflation and higher unemployment have risen, noting that they may face “difficult tradeoffs” if inflation proved more persistent while growth and employment weakened. Almost all of them worried that inflation could prove to be more persistent than expected.

Where is the US economy really going now?

That broadly echoes the uncertainty prevailing in the financial markets. Analysis from the Fed’s Atlanta branch shows an unusually dispersed array of expectations for US economic growth in the second quarter, ranging from a decline of 1% to growth of 3%. The bank’s own GDPNow model is currently forecasting 2.2% based on the latest data flow.

.png?format=pjpg&auto=webp&quality=50&width=753&disable=upscale)

From here, the personal consumption expenditure (PCE) measure of US inflation – the price growth gauge favored by Fed officials – headlines a slew of releases due to update the markets on the state for the world’s largest economy. The headline reading is expected to inch down to 2.2% year-on-year in April, the lowest in seven months.

The core measure excluding volatile food and energy prices – a focal point for the Fed – is expected to come down to 2.5%, the lowest since March 2021. Both measures are seen rising just 0.1% from the prior month, hinting at a third month of improvement in annualized 3- and 6-month averages monitored by central bank officials.

Fed rate cut delay may hurt stocks and the US dollar

Meanwhile, a second look at first-quarter US gross domestic product (GDP) data is expected to confirm preliminary estimates showing that output fell at an annualized rate of 0.3%. Revised consumer confidence data from the University of Michigan (UofM) is expected to reiterate that sentiment soured to the weakest since June 2022 this month.

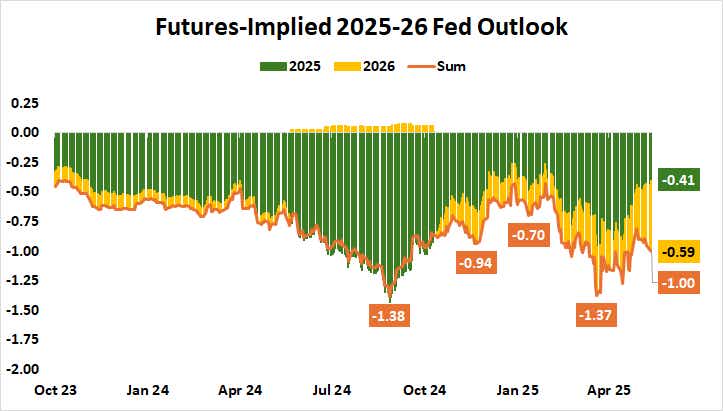

This makes for a curious way forward. If not for the Fed’s reluctant posture, cooling growth and inflation might have made for an ideal recipe to resume cutting interest rates. Benchmark Fed Funds futures suggest nothing of the sort is on the menu until September however, and even then the probability of delay is a hefty 40.1%.

Traders have trimmed rate cut bets to just 40 basis points (bps) in cuts this year, amounting to the most modest setting for 2025 stimulus expectations in three months. The view for 2026 has grown more dovish however, with 60bps now on the menu. Put simply, the markets are angling for a delay that demands more forceful action later.

Absent a striking departure from consensus in the upcoming data, a further shift in the same direction may breathe some life into longer-dated US Treasury bonds as well as gold prices. Meanwhile, stock markets and the US dollar may retreat. Needless to say, all this presumes no shocking headlines from the White House, which may be a tall order.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts #Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit #tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices