FOMC Minutes: Are Stocks at Risk if the Fed Gets Inflation Wrong?

FOMC Minutes: Are Stocks at Risk if the Fed Gets Inflation Wrong?

By:Ilya Spivak

Is the stock market in trouble if the Fed is wrong about inflation? The Iran war trade is fading across gold, bonds, and the dollar. A hawkish turn at the US central bank may turn out to be dangerously out of date.

- Stocks remain trapped in a two-month range, but bonds and gold are turning up as the dollar rolls over

- Bond market inflation expectations have slipped below where they began the year, hinting at cooler prices ahead

- The Fed sounded aggressively hawkish in June — the risk is that it is fighting yesterday’s shock and missing tomorrow’s slowdown

The bellwether S&P 500 keeps oscillating in the choppy range that has held it for the better part of two months. It is still tracing the outline of a “diamond top” bearish reversal chart pattern, but the setup remains unconfirmed until a decisive breakdown has been registered. Direction, for now, is still missing. Conviction appears in markets outside of equities however, where a coherent story is taking shape.

The war trade is unwinding across the board

Crude oil has drifted back to the gap it left when the US-Iran war erupted in late February, the entire geopolitical premium erased, and momentum is now quietly turning up as if the selloff has found a floor. The initial relief from the latest ceasefire looks spent, with the market treating an open Strait of Hormuz — tankers departing despite sporadic violations, including an overnight strike on a Qatari gas carrier — as the new baseline. Treasury bonds are carving out a base on a series of higher lows, as though yields are hunting for a ceiling. Gold has cleared its near-term range top and looks set to retest $4400/oz. The US dollar, which fed on wartime yields, is sliding back toward the floor of its uptrend.

The pattern is unmistakable, because it is effectively the war trade in reverse. When the conflict began, oil spiked, the dollar rallied, gold fell, and bonds sold off as yields surged — all on the reckoning that the shock was inflationary and would force the Federal Reserve to abandon rate cut plans, and perhaps even consider a hike. With oil now back to square one, those moves look like the first steps of an about-face turn. If the markets have priced out the oil shock, then letting go of its inflationary echo may be next, and with it the hawkish Fed that the war conjured.

Markets are betting inflation runs cooler, not hotter

The clearest evidence sits in the bond market’s own inflation gauges. Breakeven rates — the 5-year and 10-year inflation expectations embedded in Treasury pricing — have slipped to levels lower than where they began the year. Stripped of the oil shock, in other words, traders now suspect inflation may run cooler than they assumed even before the conflict. That may be because because growth itself is seen faltering as a broader downswing in the business cycle comes into view. The Cleveland Fed’s widely watched inflation “nowcast” points the same way, with the headline measure set to decline in the months ahead.

An economy quietly eating itself

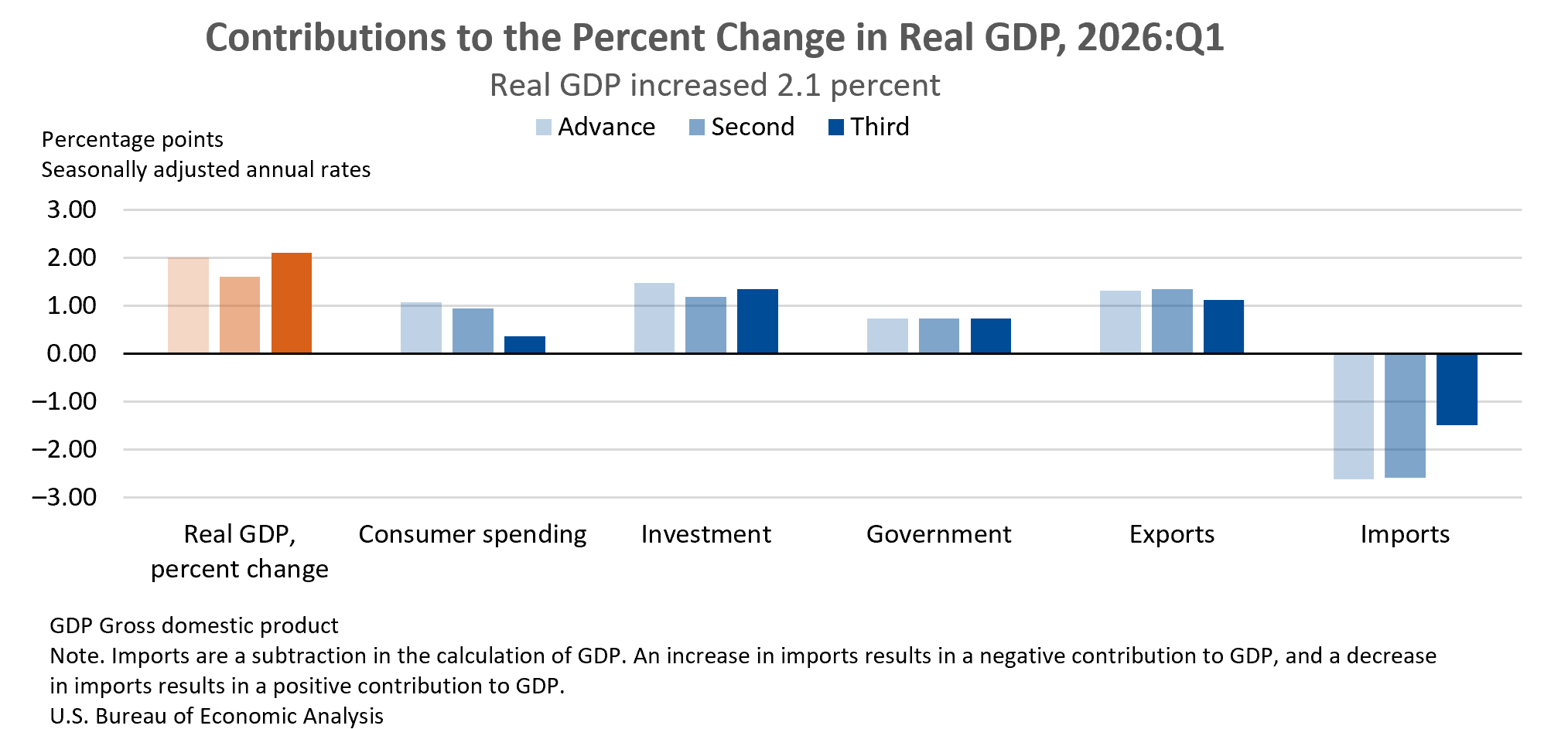

Suspicion of a faltering economy traces to an unsustainable growth mix. First-quarter gross domestic product (GDP) rose 2.1%, only about halfway back to the roughly 4% the economy managed before last year’s government-shutdown quarter, and it got there with barely any help from consumption — 68% of output — while business investment, a mere 15%, did the heavy lifting on the back of the artificial intelligence (AI) buildout.

The trouble is that forcing so small an engine to spin at a blistering annualized pace above 10% throws off inflation that seems to have crept into the core services sector, where households do most of their spending. That squeeze helps explain a third straight month of falling real wages, and it feeds a self-defeating loop: the investment boom holding the economy up is also steadily bleeding the consumer, who is five times larger and, historically, a more robust source of expansion beyond the ceiling of about 2% for investment-led growth. Should consumption tip negative, the whole economy would likely follow. That template is already on display abroad — humming AI-linked factories in Europe and Australia have not kept those economies out of contraction as their dominant service sectors shrink.

Is the Fed fighting the last war?

That backdrop makes the release of minutes from June’s Federal Open Market Committee (FOMC) meeting — Kevin Warsh’s first as Fed chair — a pivotal event. The message from that gathering was startlingly hawkish for a chairman appointed as a supposed advocate of rate cuts: a terse statement, a repeated vow to deliver price stability, and projections from Mr Warsh’s colleagues that revised core inflation higher all the way out to 2028. Markets still price one 25-basis-point (bps) hike as a near-certainty by October, though only a 24% chance of a second one. The question the minutes must answer is whether the committee still saw the oil spike as a passing shock to be looked through last month, or as reason to get back on offense against inflation.

If policymakers seem fixated on an inflation shock that is already receding, they risk being slow to ease when the cyclical crack widens and the squeezed consumer finally buckles. That may be precisely what the attempted reversals in gold, bonds, and the dollar are starting to price in. A hawkish hold that might have looked prudent until recently would instead raise the specter of a Fed that is too reactive and late to respond as downturn strikes. That may bode ill for market-wide risk appetite, and stock markets by extension.

Ilya Spivak, tastylive Head of Global Macro, has over 15 years of experience in trading strategy. He specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices