Stock Market: Are Oil and Gold Prices Saying There's Trouble Ahead?

Stock Market: Are Oil and Gold Prices Saying There's Trouble Ahead?

By:Ilya Spivak

A weak jobs report may finally pull the market’s gaze off Middle East headlines and onto the economy, where a squeezed consumer is looking like the real threat.

- Crude oil refused to fall even as Saudi Arabia cut prices and OPEC+ agreed to pump more, a sign the war premium is fully drained

- Bonds and gold are turning higher while the dollar slips — moves that now look less like war relief and more like a growth scare

- June’s payrolls came in soft, and incoming Fed meeting minutes will show whether policymakers share the worry

The US economy is inching along, and the stock market is doing much the same. The bellwether S&P 500 popped to start the week, but on almost comically thin volume, and the broad consolidation that has gripped it since mid-May rolled on. The chart is still flirting with a possible “diamond top” — a still unconfirmed bearish reversal pattern — as momentum ebbs and the market hunts for direction. Other financial markets offer more instructive signals, however.

Crude shrugs off bad news as the war trade unwinds

Start with crude oil, which has drifted back to the gap it left when the US-Iran war erupted in late February, the geopolitical premium all but washed out. What is telling is how little it now reacts to news that should push it lower. Saudi Arabia circulated discounted prices for Asian buyers, the first such cut since the 2020 price war, and OPEC and its allies agreed over the weekend to raise output. Crude barely flinched. With momentum quietly turning up, the market seems to have decided the relief from the war is already in the price, and there is little more to give without a fresh catalyst.

The other war-trade assets are reversing in tandem. Treasury bonds, battered lower through the conflict as yields climbed, are carving out a base and holding a series of higher lows, as if rates are searching for a ceiling. Gold has perked back above $4000/oz and looks set to retest the $4300–$4400 zone. The US dollar, which fed on wartime yields, is pulling back on cue as that support fades. For weeks these moves could be read as the war scare receding. That reading may no longer fit, precisely because crude has already erased the war’s impact and now refuses to fall further.

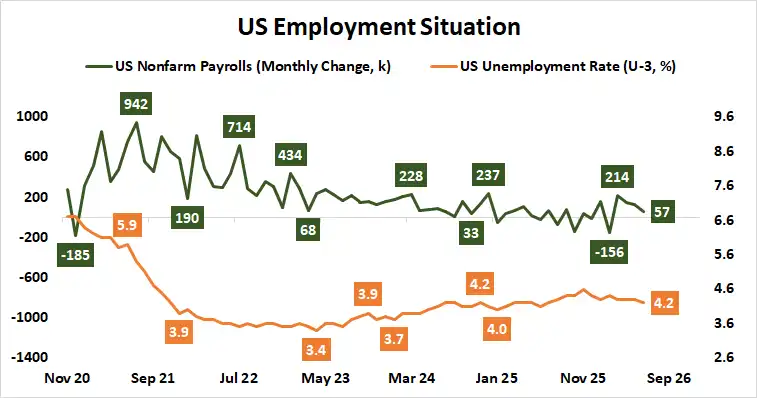

A soft jobs report shifts the story to the cycle

If not war relief, then what? The answer arrived in Friday’s June payrolls report, and it was unsettling. The economy added just 57,000 jobs, roughly half the 110,000 expected. The unemployment rate slipped to 4.2%, but for the wrong reason — the labor force shrank as discouraged workers stopped looking, flattering the figure rather than reflecting strength. Worse, the prior two months were revised down by a combined 74,000. Layered on top of an economy that this week’s ISM surveys show may have plateaued after last year’s thrust, the labor data gives the market permission to stop chasing the day’s Middle East headlines and start reckoning with the business cycle itself.

The consumer is being squeezed by what holds the economy up

The jobs data amplifies a problem the first-quarter growth figures already flagged. Gross domestic product (GDP) expanded 2.1%, but the contribution came overwhelmingly from business investment — barely 15% of the economy — while consumption, five times larger at 68% of output, added almost nothing by comparison. That inversion exists because the artificial intelligence (AI) buildout has investment growing at a blistering pace even as consumer spending fades.

The catch is that wringing steady growth from so small an engine forces it to run hot enough to throw off inflation, which lands in the core services, where households do most of their spending. Friday’s report sets up a third straight month of negative real wages, with pay growth at 3.5% trailing inflation above 4%. The very dynamic propping up the economy is bleeding the consumer who is supposed to sustain it — a self-defeating loop that can only run so long, given that consumption dwarfs investment. The endgame is already on display abroad: in Europe and Australia, humming AI-linked factories have not spared economies that are contracting as their far larger, consumer-driven service sectors shrink.

The Fed may back off — for the wrong reasons

This recasts the bottoming in bonds and gold and the topping in the dollar. Rather than celebrating a durable peace that lifts the threat of expensive oil, those reversals look like the market sniffing out a cyclical risk — demand destruction that would spare the Fed from aggressive rate hikes as a weakening economy does the tightening for it. Fittingly, policy expectations have cooled: a single hike this year is still the base case, but no longer a certainty.

Wednesday’s minutes from Kevin Warsh’s first meeting as Fed chair are the next test. If the committee sounds as worried about growth as it is about the lingering inflation shock, it would validate the cyclical anxiety now seeping into markets and could be the nudge that completes that diamond top hanging over stocks. The market has spent months trading war headlines one tweet at a time. A soft jobs report has quietly changed the subject to something harder to negotiate away: an economy generating inflation faster than it generates the wages to withstand it.

Ilya Spivak, tastylive Head of Global Macro, has over 15 years of experience in trading strategy. He specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices