Should the Stock Market Be Higher if the US-Iran Oil Shock is Over?

Should the Stock Market Be Higher if the US-Iran Oil Shock is Over?

By:Ilya Spivak

The war premium has drained from crude oil, interest rates are lower, and chipmakers are pledging hundreds of billions — yet stocks stay stuck. With a data-packed holiday week ahead, what is the market really watching?

- The S&P 500 is grinding in the middle of its range, unable to break out despite a barrage of good news

- Wages have now slipped below the rate of inflation, a fresh squeeze on the consumer that powers most of the economy

- A shortened week packed with jobs and manufacturing data will test whether that squeeze is starting to bite

The bellwether S&P 500 managed a rebound but could not get far, settling back into the middle of the range that has boxed it in since early May. What makes the stall remarkable is everything it is shrugging off. By any conventional reading, this should be the best of all possible worlds for equities — and they cannot break out.

The best of all possible worlds, ignored

Consider what the rest of the market is signaling. Crude oil has all but erased the entire wartime run-up as the US-Iran ceasefire holds and tankers trickle back through the Strait of Hormuz, draining the geopolitical premium that drove this year’s inflation fears. Treasury bonds have broken higher out of a month-long range, pulling yields lower, as if to say the inflation threat is easing. Gold’s long slide is showing signs of fatigue and the US dollar is edging off its highs.

On top of all that, South Korea’s chipmaking giants Samsung and SK Hynix pledged alongside the government to deliver a massive 800 billion won (some US$520 billion) for development. That came just days after blowout earnings results from US memory giant Micron Technology underscored that the AI building boom continues to burn bright.

War premium gone, borrowing costs easing, the AI engine roaring — stocks could be expected to be soaring. Instead, they sit pinned in their range. When the best possible news cannot lift a market, the obvious conclusion is that the market is no longer worried about what that news addresses. The wartime narrative is giving way to something else.

The new worry: wages can’t keep up with prices

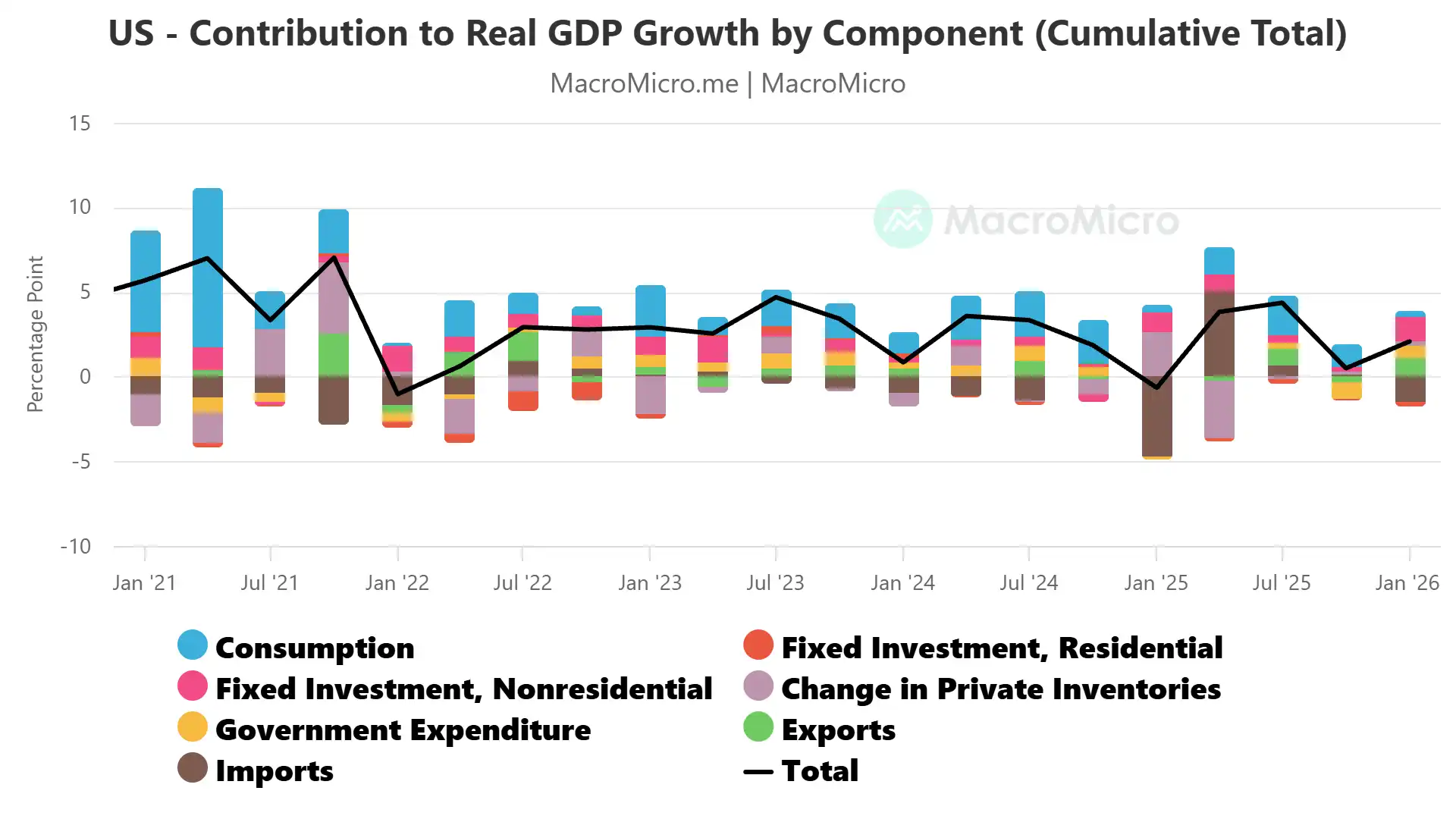

That something else is the consumer, and the freshest evidence is unsettling: average hourly earnings growth has now fallen below the rate of inflation. With price growth scratching above 4% — the highest in years — paychecks are losing ground in real terms for the first time in a long while. That is where the danger lies, because the consumer accounts for 68% of the economy, dwarfing the roughly 14% from business investment.

Last week’s data showed why that imbalance is so corrosive. First-quarter gross domestic product (GDP) growth was revised up to 2.1%, yet consumption contributed a pittance — the smallest input of any category save imports — while business investment, growing above a 10% annualized clip on the data center boom, did nearly all the work.

The catch is that investment-led growth has a hard ceiling: over more than two decades it has contributed more than 2% to annualized GDP only twice, whereas consumption-led growth routinely runs higher. So 2.1% is about the best that the current growth configuration can produce, against the nearly 4% the economy logged last year when households were stronger.

To squeeze even that from one of the lesser engines of demand, it has to spin so fast that it throws off inflation. That lands in core services, which is exactly where consumer spending is concentrated. The current growth model thus seems to be cannibalizing the consumer it depends on, as if the economy is eating itself. Europe and Australia are further down that road already, their factories humming on the AI wave even as shrinking service sectors tip them into contraction.

A holiday week built to test the consumer

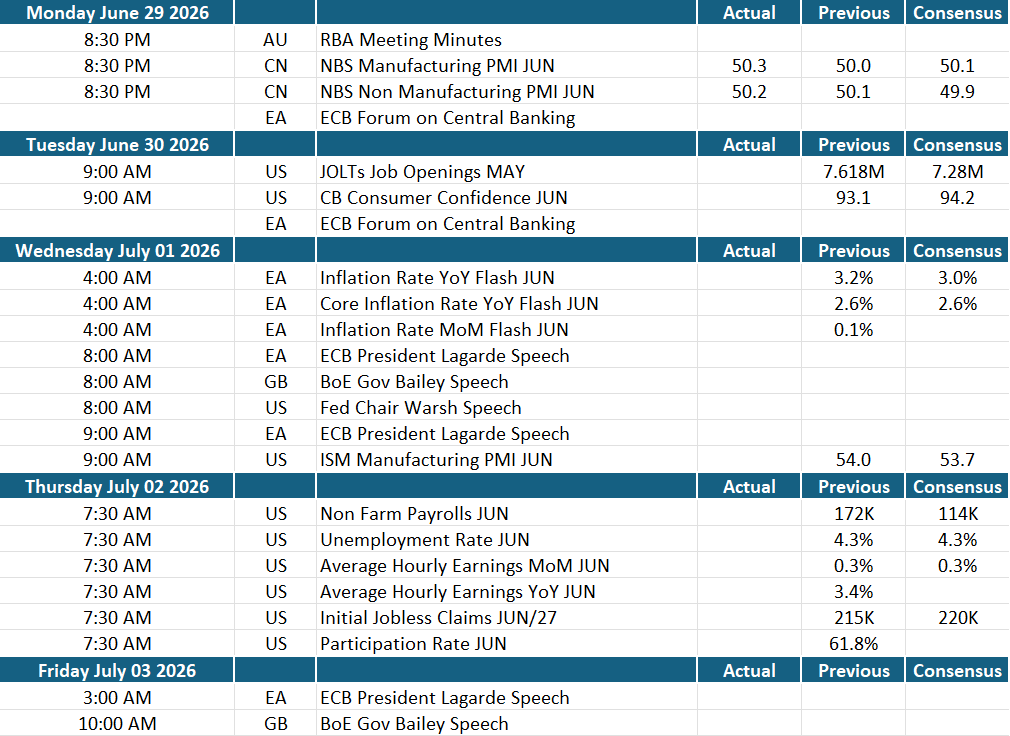

That is what makes the coming days pivotal. Trading is condensed into Monday through Thursday ahead of the US Independence Day holiday, and the calendar is stacked with readings on exactly this question.

US job openings on Tuesday are seen slipping to about 7.3 million from 7.6 million. The Institute for Supply Management (ISM) manufacturing gauge should confirm the now-familiar split — a factory sector running near its strongest in four years while services barely register a pulse. Central bank chiefs, including new Fed chair Kevin Warsh, convene at the European Central Bank’s annual forum in Sintra, Portugal. The same inflation-versus-growth bind will surely be front of mind.

The marquee event is Thursday’s release of June payrolls report, pulled forward by the holiday. Hiring is expected to slow to 114,000 from 172,000, with the jobless rate holding at 4.3%. That would mark a clear downshift from the prior three months, all of which topped 170,000 — and a soft print would speak directly to the headwinds battering a consumer that is already losing the race against prices.

Even the Fed may start to flinch

The shift is creeping into rate expectations. Abroad, where the consumer squeeze is more advanced, the hawkish tally is receding — the odds of further tightening are fading for the central banks of Australia, the Eurozone, Canada, and the UK. The outlook for the Fed has held firmer but even its path has softened: markets that recently flirted with two 25-basis-point (bps) hikes this year now lean toward a single increase arriving by October, followed a long pause through 2027.

The conversation may be changing from how high rates must go to fight inflation to how much price growth is already hurting demand, and what the central bank may have to do as that pressure builds. That is perhaps why this market cannot rejoice in falling oil, easing yields, and record chip investment. Those are answers to last quarter’s question. The one now in front of investors is whether a consumer whose wages no longer keep up with prices can hold the line against an economy generating inflation faster than it generates growth. If this week’s data says no, the range that has contained stocks for two months is far likelier to break downward than up — and the rally that ran on war relief will have nothing left to lean on.

Ilya Spivak, tastylive Head of Global Macro, has over 15 years of experience in trading strategy. He specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices