Will the Stock Market Boil Over as AI Overheats the Economy?

Will the Stock Market Boil Over as AI Overheats the Economy?

By:Ilya Spivak

Stocks look stuck but gold, oil, and the bond market hint the US-Iran war trade is running out of road. A wave of economic data will decide what comes next.

- The S&P 500 remains stuck in the range it has held since May, unmoved by cheaper oil amid the reopening of the Strait of Hormuz

- Gold and Treasury bonds are showing early signs that the wartime inflation trade may now look overextended

- From here, hot ISM manufacturing PMI data may put the spotlight on the AI boom and the threat that it will crush consumers and overheat the economy

Wall Street advanced for a second day but the bellwether S&P 500 stock index is still pinned in the range that has held since early May amid fading volume and slackening momentum. The stock market looks wanting for a catalyst, and the action unfolding in other assets may be starting to signal that something new is brewing.

The war trade shows signs of running out of steam

Crude oil has washed out almost the entire geopolitical premium built up since the US-Iran war began in late February. The ceasefire is broadly holding – periodic violations notwithstanding - and tankers are moving through the Strait of Hormuz again.

Some of the price drop may be overdone — a brief supply glut is in view as previously trapped ships exit the Persian Gulf, but depleted global reserves will soon need refilling, and it is unclear how many empty vessels will brave returning empty through the Strait. Still, the war premium is, for now, all but gone.

Gold tells a subtler story. Its slide since the war began was the classic response to an inflationary supply shock and the higher rates that come with it, punishing a metal that yields nothing. Now the selloff may be tiring however: prices are still setting lower lows, but momentum is diverging in a way that hints the downdraft is losing force. Treasury bonds echo as much. Having broken out of the range that capped them since mid-May, prices have pushed higher and yields lower, as if the wartime melt-up in rates has finally run its course.

A market bracing for a rethink

Put together, the gold and bond markets are whispering the same thing: the impetus behind higher rates and a more hawkish Federal Reserve may be overdone and ripe for reconsideration. That is a meaningful shift. For months the market traded a single story — the war stokes inflation, which keeps the Fed from cutting. If that fear is now draining away alongside the oil premium, the question becomes what comes next. A flood of US economic news-flow over the next two days may have the answer.

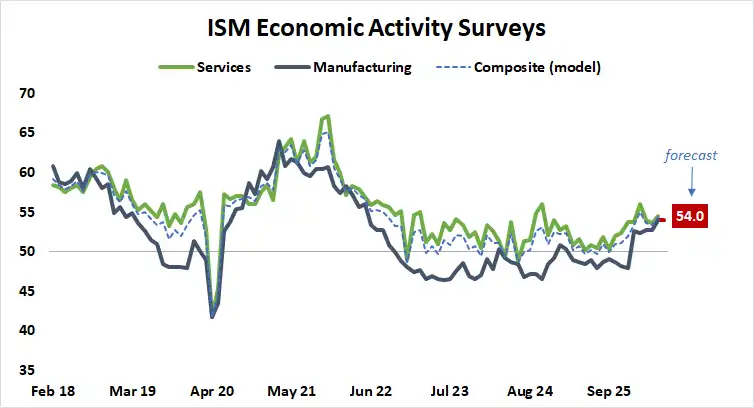

Why a strong factory report would be bad news

The first marquee release is June’s manufacturing survey from the Institute for Supply Management (ISM). The headline purchasing managers index (PMI) gauge is expected to print at 54.0, matching May’s result, which was the strongest in four years.

US manufacturing is booming, and it is tempting to credit a wave of data center construction. That is something of an oversimplification. For example, roughly $40 billion of data center projects slated to come online this year have been throttled by local opposition. The factory surge is instead more of a stockpiling of inputs — buyers loading up ahead of an even higher cost curve, given the long runway of buildout that the hyperscalers’ lavish capital-spending plans imply.

This is precisely how, in the first quarter, investment overtook the consumer as the main engine of growth. First-quarter gross domestic product (GDP) growth was revised up to an annual rate of 2.1%, yet consumption — 68% of the economy — made its smallest contribution in a year, while business investment, barely 15% of output, grew above a 10% annualized clip and did the heavy lifting.

When so small a sector is pushed to punch that far above its weight, its rapid spinning stokes inflation that lands in core services, the key area for household demand. Another hot manufacturing print may thus warn of ominous overheating that hollows out the consumer sector that the economy ultimately leans on.

From rate hikes to an overheating reckoning

That trap is already visible abroad. Europe and Australia carry booming factory sectors catching the same AI wave, yet the latest batch of S&P Global PMI data shows their economies have slid into contraction as inflation destroys demand in their far larger service sectors. In fact, June’s softer-than-expected German inflation data suggests weaker demand is already beginning to feed back into prices. This warns that the current configuration of US economic growth, capped near 2% because investment alone has almost never contributed more in the past two decades, will bring the same results.

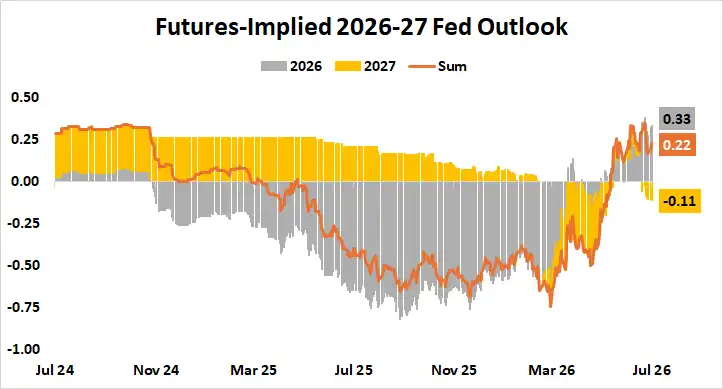

For now, markets still lean toward one 25-basis-point (bps) Fed hike this year. Fed Funds futures price in about 33bps of tightening this year, a near-lock on a September or October move, but only a 28% chance of a second one. A rate cut is narrowly favored for 2027.

What gold and bonds may be starting to anticipate is the next chapter in the story — an economy running hotter than it can sustain, on the verge of eating into the very 2% growth it clawed back, at which point the conversation stops being about how high rates must go and turns to the damage already done. If this week’s data stokes such fears, the reversals stirring in gold and bond markets may find follow-through, and the range that has trapped stocks for two months might give way to the downside.

Ilya Spivak, tastylive Head of Global Macro, has over 15 years of experience in trading strategy. He specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices