Iran War vs. AI Boom: Will Inflation Break the Stock Market?

Iran War vs. AI Boom: Will Inflation Break the Stock Market?

By:Ilya Spivak

Oil prices surged and stocks fell as a clash between the US and Iran revived the war trade, but incoming CPI inflation data may point to a deeper problem.

- Renewed conflict near the Strait of Hormuz sent oil higher, and this time stocks fell alongside bonds and gold

- June inflation is expected to ease, but almost entirely on cheaper energy that has since reversed

- The number to watch is core services inflation, which was climbing well before the war began

The bellwether S&P 500 tried to break out last week and failed, retreating from the top of the range that has hemmed it in since mid-May. That leaves last week’s attempted run to the upside looking like a false start and keeps alive the possibility that the chart is sketching out a bearish “diamond top” reversal pattern. The trigger for the downward turn was a fresh surge in crude oil — and this time, the whole market moved with it.

The war trade comes roaring back

Crude jumped after fighting resumed near the Strait of Hormuz and US President Donald Trump moved to reimpose a blockade on Iranian oil and levy a toll for passage through the vital waterway. Prices punched back above near-term resistance and now look set to retest levels north of $80 a barrel. What makes this episode different from the past several weeks is the read-through. When oil spiked earlier, stocks largely ignored it; this time equities fell in sympathy, alongside a fresh leg lower in Treasury bonds — pushing yields up — as the market traded the move much as it did in the war’s opening days.

The other war-sensitive markets fell into line. Gold, which had managed to tiptoe above its near-term range top last week even as oil stirred, saw its push toward the $4300–$4400 area aborted, and its bounce now in doubt. The US dollar found fresh support atop the year-long range it broke during the conflict, buoyed by rising yields and a flight to cash. For the first time in months, the inflation trade that defined the spring is trading as a coherent whole again. That makes the timing of incoming US inflation data especially charged.

A cooler headline that hides more than it reveals

June’s consumer price index (CPI) report is expected to show headline inflation eased to 3.8% year-on-year from 4.2% in May, which was the highest in three years. The core measure, stripping out food and energy, is seen holding at 2.9%. Nearly all of the projected relief comes from energy: crude oil fell 8.8% in May and a further 18.3% in June, shedding more than a quarter of its value across the two months before this week’s rebound. That decline will flatter the headline, and the market is likely to look straight through it because oil is climbing again as the number lands.

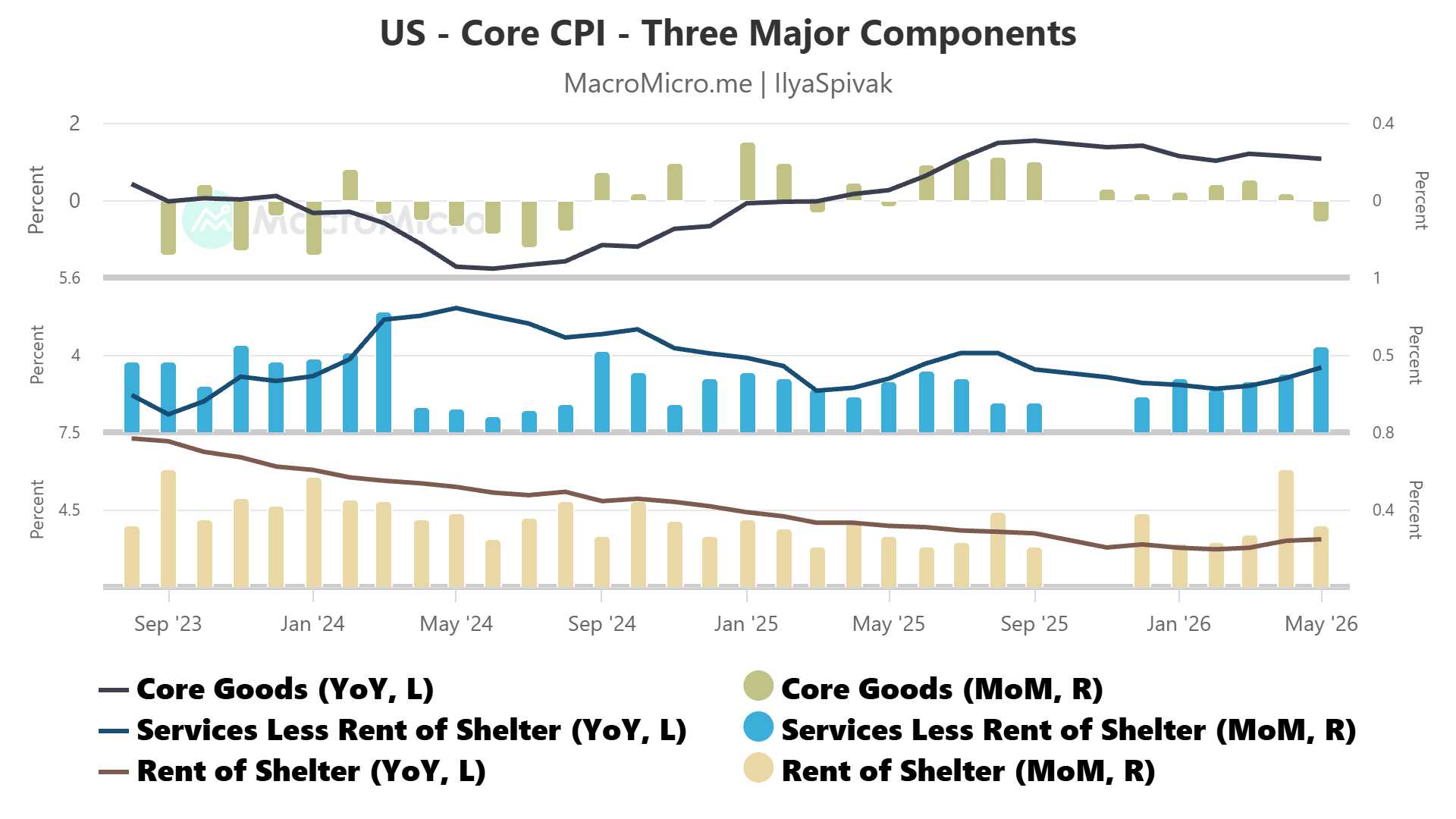

A more insidious kind of inflation

The revealing figure sits deeper in the report. Inflation in the core service sector — where the bulk of consumer spending lives — added more than two percentage points (ppt) to the May’s headline CPI reading, recording its biggest monthly jump since March 2024. Critically, that acceleration began well before the war sent oil soaring, and it excludes energy entirely. This is inflation of a different stripe, and the Federal Reserve has named the source: in the minutes from June’s Federal Open Market Committee (FOMC) policy meeting, officials cited strong demand tied to the artificial intelligence (AI) buildout ahead of the Middle East or tariffs as a driver of sticky inflation.

Economic growth figures show why that matters. First-quarter gross domestic product (GDP) rose 2.1%, and the biggest contributor by a wide margin was business investment — even though it is barely 14% of the economy against the consumer sector’s 68%. That outcome requires a strange world in which consumption barely grows while investment surges, and it is an inflationary way to grow, overclocking a small engine of demand at blistering speed while the larger one sputters. Money churns through the economy fast enough to throw off inflation, which lands in the core services that dominate household budgets.

The very boom keeping growth alive is squeezing the consumer who makes up two-thirds of it. June’s purchasing managers index (PMI) survey data from S&P Global shows where that leads: manufacturing is expanding across Australia, the eurozone, and the UK, yet all three economies are shrinking as their dominant service sectors contract under the strain. The US and Japan, more exposed to the AI buildout, have so far caught enough that tailwind to hold up.

The Fed may be fighting the last war

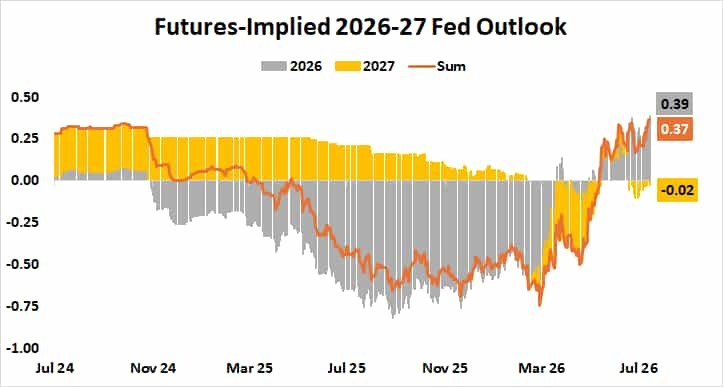

The near-term rate picture has turned hawkish again: futures price in 39 basis points (bps) of tightening this year, implying better than even odds of a second 25bps rate hike after an all-but-certain first one by September. Yet bond market positioning cuts the other way as well. Breakeven inflation rates — expectations embedded in Treasury prices — have probed below where they started the year, all the way back to levels last seen in April 2025, even though oil remained net up on 2026 even before the latest rebound. The gap between 5- and 10-year expectations has narrowed too, implying lower and steadier inflation in the longer term. Something other than just oil pulled those expectations lower. The market may be pricing in demand destruction ahead.

That is the deeper meaning of tomorrow’s report. Appropriately enough, Kevin Warsh will sit for his first semi-annual Congressional testimony as Fed Chair on the same day. He has been pounding the table about restoring price stability and will surely have to face a slew of questions from lawmakers about the “affordability crisis” splashed across the headlines for nearly nine months.

The real danger runs opposite to the hawkish headlines: a Fed locked into fighting inflation risks holding off cutting for too long, just as AI-driven price pressure grinds the exhausted consumer toward retreat. Consumption is so much larger than investment that no data center boom could offset the drag from anemic consumption for long if households continue to pull back, and the cautionary tale playing out in Europe and Australia would arrive on American shores. For a stock market already struggling at the highs, that would be a dismal prospect.

Ilya Spivak, tastylive Head of Global Macro, has over 15 years of experience in trading strategy. He specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices