Oil Prices Spike Again, But Stock Markets Face a Bigger Risk Now

Oil Prices Spike Again, But Stock Markets Face a Bigger Risk Now

By:Ilya Spivak

Oil prices jumped and June Fed meeting minutes came out hawkish, yet bonds, gold, and the dollar refused to play along. That looks scary for stock markets.

- Crude oil surged and June’s Fed meeting minutes read as hawkish, both pointing toward higher interest rates

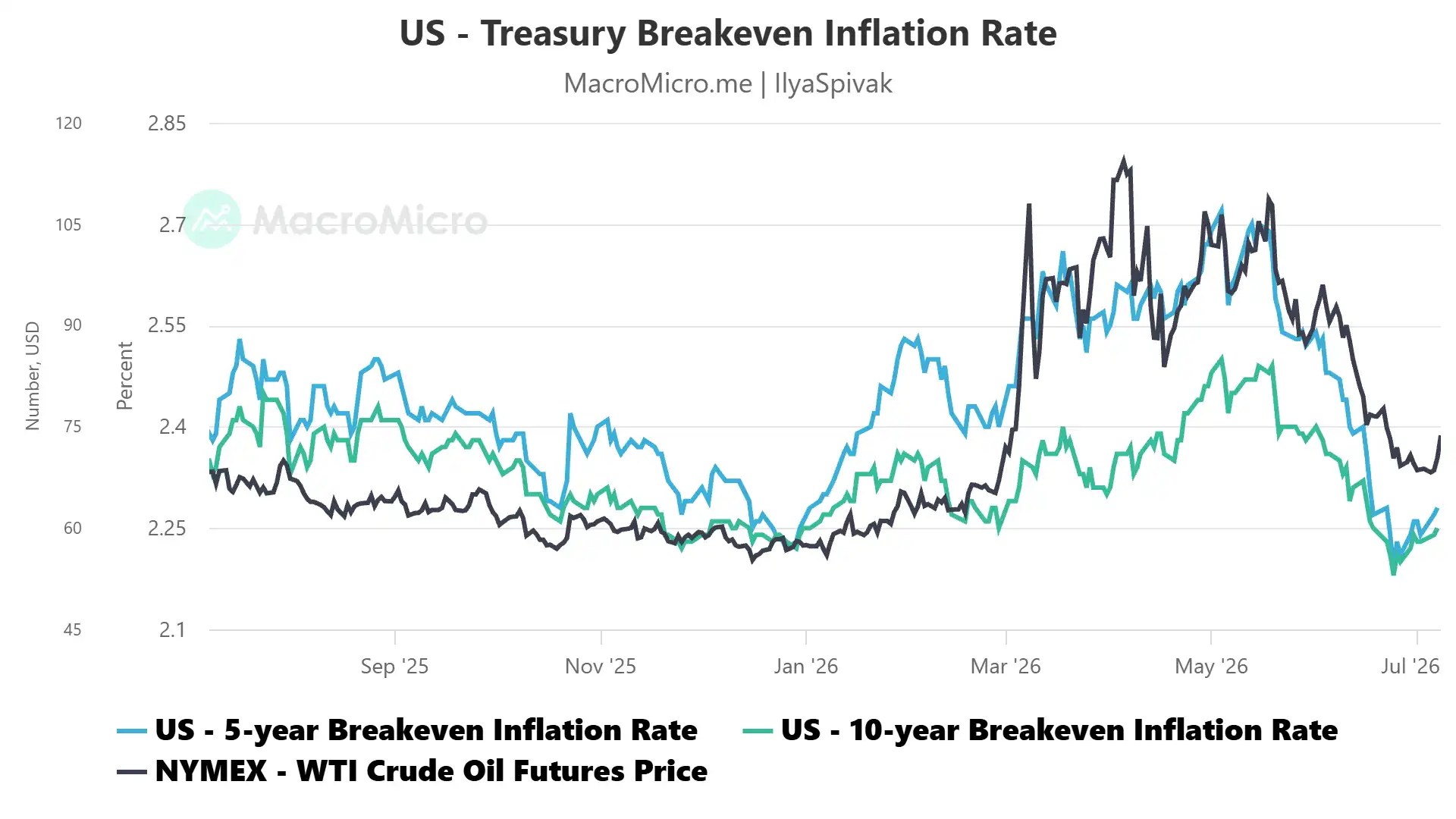

- Bonds and gold still refused to break lower, while priced-in inflation expectations have sunk below where they began the year

- Traders appear to be betting the central bank is chasing an inflation threat just as the real danger shifts to growth

The bellwether S&P 500 is still churning in the choppy range that has held it since mid-May, tracing the outline of a possible “diamond top” bearish reversal chart pattern that would project a drop toward 7000 if it were confirmed. That is yet to happen, and the stalemate persists. A more salient lead seems to be coming from the gold and Treasury bond markets, and from what they pointedly refuse to do.

The market got hawkish news and shrugged

Two developments might have driven interest rates higher. Crude oil surged after US President Donald Trump moved to tear up the ceasefire with Iran. Prices pared gains when Trump walked back some of the fire and fury, but the WTI benchmark still closed up 3.3% on the day and 8.7% over two sessions. On top of that came the minutes of June’s Federal Open Market Committee (FOMC) meeting, and they were unmistakably hawkish: most officials judged the upside risks to inflation elevated and preferred stripping the easing bias the latest policy statement. A few even argued that a rate hike was already warranted.

By the old script, that combination should have sent bonds lower and yields higher. It did not. Treasury bonds sagged but held the base they have been building since mid-May, as if to say the market has already priced in all the tightening it cares to. Gold, which fell hard through the war as rising rates and a strong dollar punished a metal that yields nothing, dipped but never tested its lows, extending the bottoming process it began weeks ago. The US dollar tried to break higher and faded. Handed news it could have used to push rates up, the market declined the invitation.

Fighting the last war

The minutes revealed a Fed convinced the inflation problem runs deeper than oil. Officials pointed to strong demand tied to the artificial intelligence (AI) buildout, layered on top of freight and warehousing costs left by the wartime energy shock and the lingering bite of tariffs. Their reaction function tilted hawkish in both directions: if the labor market holds up, inflation stays hot enough to justify further hikes; even if inflation cools toward the 2% goal, they would sooner hold than cut. New Chair Kevin Warsh drove the point home, hammering the commitment to price stability.

Yet the market is looking straight past that resolve, and the clearest sign sits in the bond market’s own inflation gauges. Breakeven rates — the 5-year and 10-year inflation expectations embedded in Treasury prices — have not merely given back the war premium; they have sunk below where they stood at the start of the year. Oil is still net higher on the year, yet expected inflation has dipped lower, which means something more powerful than the fading war premium is now in play. Traders, in short, suspect the Fed is fighting the last war — steeling itself against an inflation threat that is already giving way to a bigger disinflationary force building underneath it.

An economy set up to eat itself

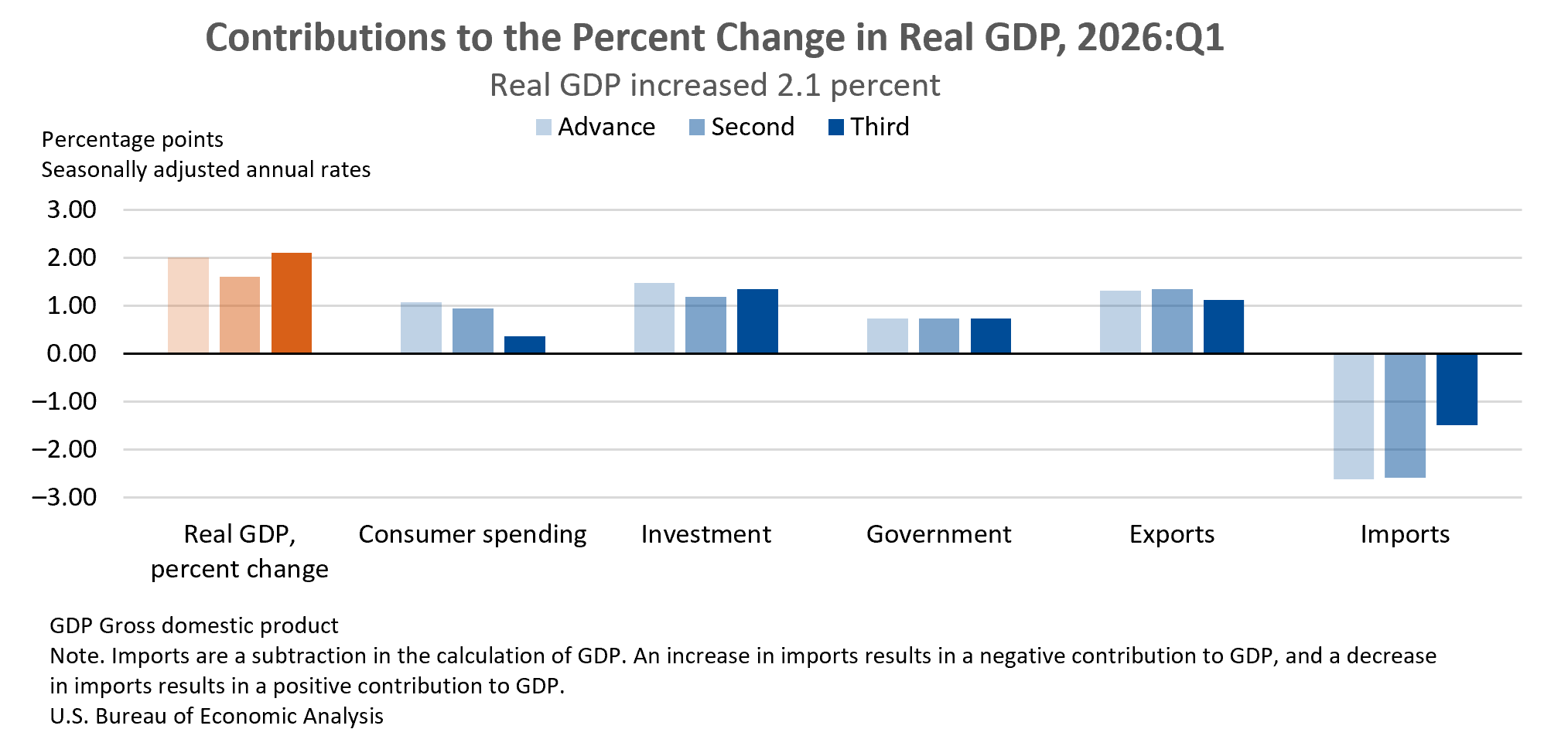

That force is the lopsided shape of US growth. First-quarter gross domestic product (GDP) rose 2.1%, only about halfway back to the roughly 4% pace of last year’s middle quarters, and it got there with almost no help from the consumer. The muscle came instead from business investment — barely 15% of the economy against consumption’s 68% — as companies stockpile inputs ahead of the AI construction wave, even as local opposition holds back the data centers themselves.

The problem is what that arrangement does to prices. Forcing so small an engine to carry the economy means running it hot enough to send money churning at high velocity, which throws off inflation. That is already showing up in core prices, where the impact of energy (and food) is stripped away. That inflation has lifted the costs of services, where most household spending lands, squeezing consumers that make up more than two-thirds of the economy. The AI boom keeping growth alive in the near term is thus hampering the demand that it ultimately rests on. Europe and Australia show where the road leads: their factory sectors are humming along thanks to the same AI tailwinds, yet the overall economies have slipped into contraction mode as inflation forces their dominant service sectors to retrench. The US has not arrived there, but the recipe seems to be the same.

A rate hike the market plans to take back

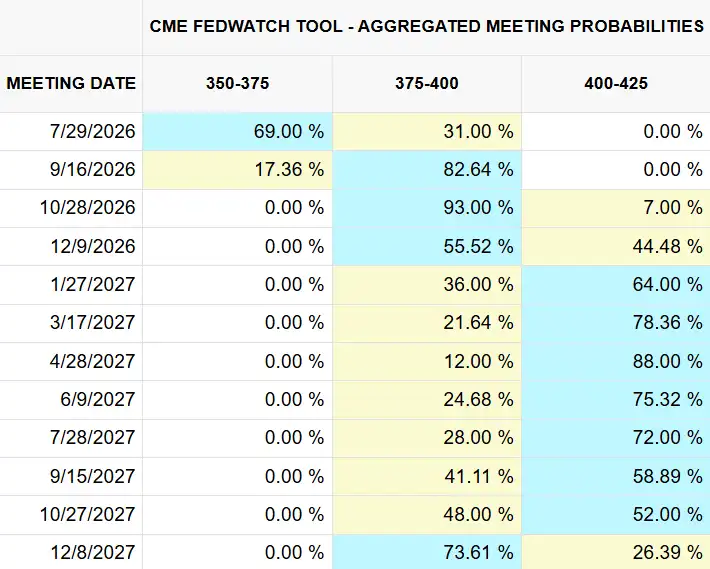

The Fed policy outlook captures the tension perfectly. Futures fully price one 25-basis-point (bps) hike this year — near-certain by October — and better-than-even odds of a second by early next year. But that is where conviction stops. By the end of 2027, markets put a 93% chance that the second hike is already reversed. Traders will grant the Fed its near-term hawkishness, but they refuse to extrapolate it. That seems to be because they expect a slowing economy to force a rethink.

That is the message beneath a quiet, indecisive day. The Fed is anchored to the inflation it can see now, while the bond and gold markets are positioning for the downturn they see coming — the point where the AI-driven boom finally tips the squeezed consumer into retreat and drags growth down with it. Should that happen, a central bank still fixated on price stability would be slow to ease, arriving with support only after a lot of damage has been done. For stocks caught in their two-month range, that is the unsettling subtext of the standoff: the longer the Fed leans against a fading threat, the greater the risk it is caught flat-footed by the one actually approaching.

Ilya Spivak, tastylive Head of Global Macro, has over 15 years of experience in trading strategy. He specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices