Stock Market Surges on US, Iran Deal. Problem Solved? Not So Fast

Stock Market Surges on US, Iran Deal. Problem Solved? Not So Fast

By:Ilya Spivak

Stocks cheered a breakthrough toward ending the US-Iran war, but the bond market refused to celebrate. Has the deal fixed the wrong problem?

- Equities, gold, and oil all showed relief, yet none broke the levels that have defined recent market turmoil

- Treasury bonds barely flinched — no rally, not even a token bounce — signaling the inflation threat is intact

- With the new Fed chair’s first meeting on deck, will policymakers confirm that a truce changes nothing on rates?

Financial markets are jubilant. After what feels like dozens of false starts, there is finally an apparent step toward ending the US-Iran war — an understanding between Washington and Tehran to reopen the Strait of Hormuz — and risk assets cheered. But the celebration is far from unanimous across markets, and the holdout is the one that matters most.

Everyone is celebrating except the bond market

The bellwether S&P 500 stormed higher, breaking above the bounds that had defined the recent selloff. Yet it closed below its record high, the critical level defining the downturn this month, and the rebound is coming on drastically fading volume — the same thinning participation that preceded the breakdown.

Crude oil pulled back as some geopolitical risk came off the table, but it held the wartime floor it established after the conflict began. Gold staged a potent bounce, only to stall at former support turned resistance without breaking back over; its sequence of lower highs and lower lows remains intact.

Then there are bonds — and here the story turns. Treasury prices did not merely rally weakly; they barely reacted at all, with not even a token wick above the range top that has capped them since mid-May. If a genuine de-escalation were resolving what truly ails markets, bonds might have been the first to unclench. They have not. The US dollar tells a similar tale, easing only modestly while holding the bounds of its six-week uptrend.

The deal fixed the missiles, not the inflation

The divergence makes sense once you ask which problem the deal actually solves. From the war’s outset, markets read it not as a “World War III” scenario but as an inflation shock: crude spiked, and that translated into weaker bonds, higher yields, a firmer dollar, and softer gold. The truce may genuinely lower the odds of missiles flying. It does little if anything for the inflationary impulse that was the real concern all along.

That impulse is already baked in. Reopening the Strait of Hormuz will take months in practice — the Red Sea offers a cautionary parallel, where shipping traffic still has not recovered nearly a year after a deal with the Houthis, because insurers and shippers remain skittish. More importantly, the energy shock has already seeped into core inflation.

The latest consumer price index (CPI) data showed core services — the largest slice of inflation excluding energy — rising at its fastest year-on-year pace since the middle of last year as the energy shock spilled over into the broader cost structure. Producer prices (PPI) data told a similar story. That scarring will not heal in weeks or months; it is more likely a matter of quarters. The bond market, refusing to rally, is simply pricing what stocks are ignoring.

A central-bank week built around Wednesday

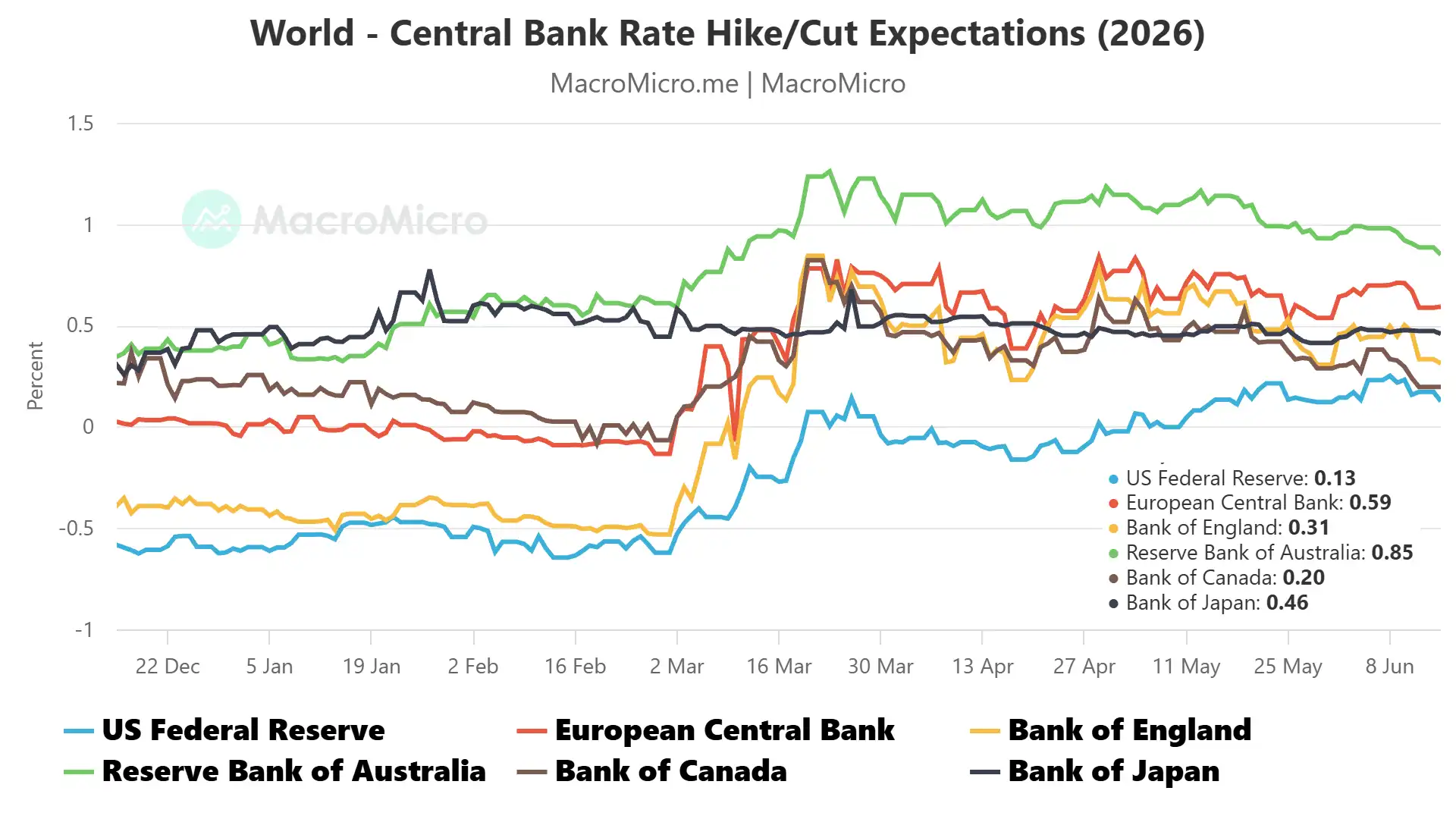

The week ahead splits into three: before Wednesday, Wednesday, and after. Ahead of the main event, the Bank of Japan (BOJ) is expected to hike for the first time since December, lifting rates to their highest since 1995, while the Reserve Bank of Australia (RBA) is seen pausing after three straight increases as its economy shows signs of wear — two very different responses to the same global pressure.

Wednesday brings the first Federal Reserve policy announcement under new chair Kevin Warsh. No rate change is expected, but the updated projections and the tone of the press conference are what matter, alongside a retail sales report that speaks directly to the embattled consumer.

After Wednesday, the Bank of England (BOE) decides; no move is expected there either, but the hawkish camp is seen growing from one official favoring a hike to two — echoing the European Central Bank (ECB), which hiked last week despite a standstill economy. Tellingly, markets still price a roughly 75% cumulative chance of at least one Fed hike by December, peace deal notwithstanding.

Why the Fed won’t ride to the rescue

The bullish hope is that a truce paves the way for a friendlier rates backdrop. The Fed’s own projections argue otherwise. Its March forecasts, issued just after the war began, raised expectations for both output and inflation — and lifted the longer-run growth and interest-rate paths too.

That combination is the tell. If the uplift in inflation expectations reflected an energy shock, the Fed would have marked growth down, not up. Raising both says policymakers see price pressure that does not owe to the war at all.

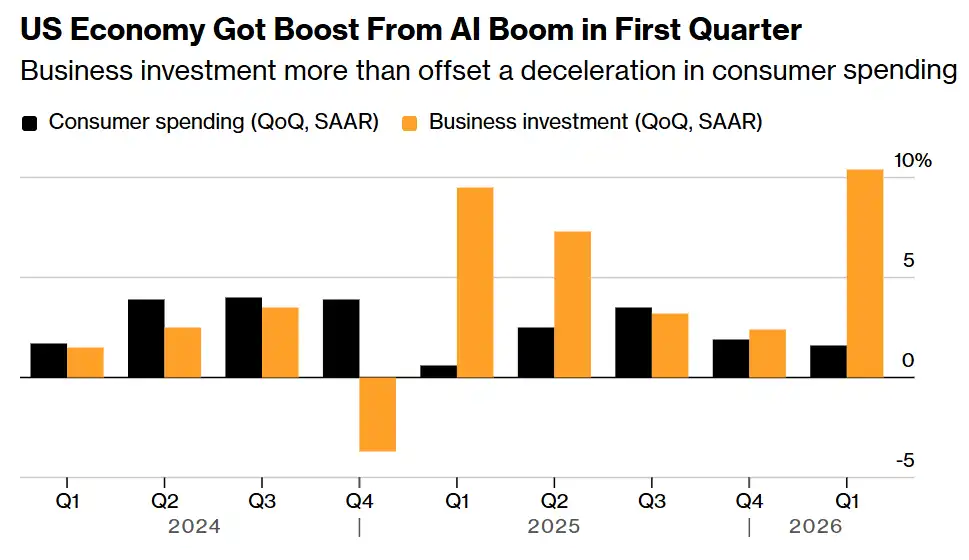

That pressure traces to the fragile shape of US growth. First-quarter gross domestic product (GDP) recovered only about halfway from the slump amid the US government shutdown in the fourth quarter, and it did so because business investment — about 14% of the economy — grew at a blistering 10.4% annualized clip and out-contributed consumption, which is 68% of output and decelerated for a second straight quarter. Forcing a small share of the economy to grow so fast sends money churning at high velocity – that is what inflation is made of. The war did not create the problem; it compounded one already building.

So, when the Fed speaks Wednesday, the dovish pivot that traders may be counting on is unlikely to arrive. The last Fed meeting’s sharpest dissents came from members who wanted the easing bias removed from the policy statement, and nothing about a truce changes the inflation math. If bonds are right and stocks are wrong, this jubilant rebound is running on a misread, and the reckoning has merely been postponed.

Ilya Spivak, tastylive Head of Global Macro, has over 15 years of experience in trading strategy. He specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices