Stocks After the Fed: Did New Chair Warsh Just Break the Market?

Stocks After the Fed: Did New Chair Warsh Just Break the Market?

By:Ilya Spivak

A Fed chair installed to be dovish just oversaw a startlingly hawkish debut — setting the stage for rate hikes and punishing the stock market. Now what?

- Stocks reversed hard after the FOMC policy meeting, carving what might turn out to be a major top

- The Fed’s new projections swapped an expected rate cut this year for a hike — and chair Kevin Warsh refused to soften the message

- Markets now price near-certain tightening by autumn, with a second hike on the menu by December

Did the Fed just break the rally? The first policy announcement helmed by new Federal Reserve chair Kevin Warsh left markets visibly shaken, and the price action turned on a dime. The bellwether S&P 500 had climbed back to the swing high where June’s meltdown began; in the wake of the meeting, it reversed back through former support and now looks like it may be carving a double top.

A hawkish surprise stops the rebound cold

The reversal carries the same fingerprints as the prior breakdown — fading volume and negative divergence on the relative strength index (RSI), more acute this time because the index notched a marginally higher high while momentum lagged far behind.

Gold was rejected at former support turned resistance, reasserting its downtrend. Treasury bonds were turned away at the top of their recent range, leaving the wartime rise in yields intact, while the US dollar bounced off the uptrend it has built since April. In short, markets hoping for a softer touch from the US central bank did not like what they heard. Meanwhile, crude oil stopped falling at the bottom of its US-Iran-war range, an auspicious spot that suggests it may be done handing markets a disinflationary tailwind.

From a cut to a hike, with no guidance to soften it

The Fed held rates steady, as expected, but everything around that decision leaned hawkish. The statement itself was strikingly brief — a deliberate move away from forward guidance that hands markets more two-way risk about where policy goes next. What it did say flagged solid economic activity, strong capital investment and productivity, and inflation still elevated relative to the 2% goal, in part reflecting supply shocks. And one line, which Warsh would repeat almost mechanically throughout his press conference: the Fed will deliver price stability.

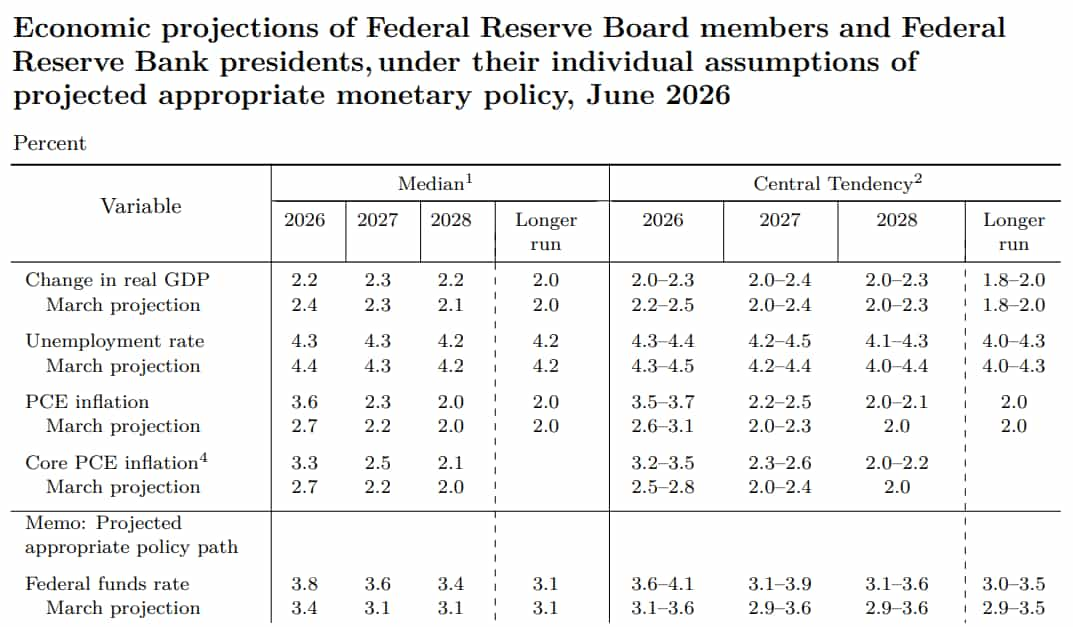

An updated Summary of Economic Projections (SEP) gave that pledge teeth. In March, the Fed’s rate path implied a cut this year, to midpoint of 3.4% from the current setting at 3.6%. The new dot plot lifts that to 3.8%, swapping the expected cut for a hike. Officials pencil in taking it back in 2027 and finally bringing rates to the 3.4% centerline a year later, a hawkish hump that means materially higher rates than previously expected across the whole forecast horizon. The estimate for the long-run rate was held at 3.1%.

The dovish chair who won’t fight the hawks

Here is the twist. Warsh arrived with a White House mandate to be more dovish than predecessor Jerome Powell. He did not participate in the dot plot at all, citing a philosophical objection to the exercise. The hawkish path therefore reflects the rest of the committee, and rather than push back on it, Warsh declined to offer any alternative, retreating to the refrain that the Fed is not in the business of “forward guidance” anymore.

A chair expected to advocate for easing instead let a hawkish committee speak for itself and added only that price stability must be had without fail. He also unveiled five task forces — on the Fed’s balance sheet, its use of economic data, its approach to benchmarking inflation, its policy communications, and the evolution of productivity and the labor market — to reexamine how the Fed operates by year-end. That made for a clear signal that this is a new regime, even as the 2% goal stays firmly off the table for revision.

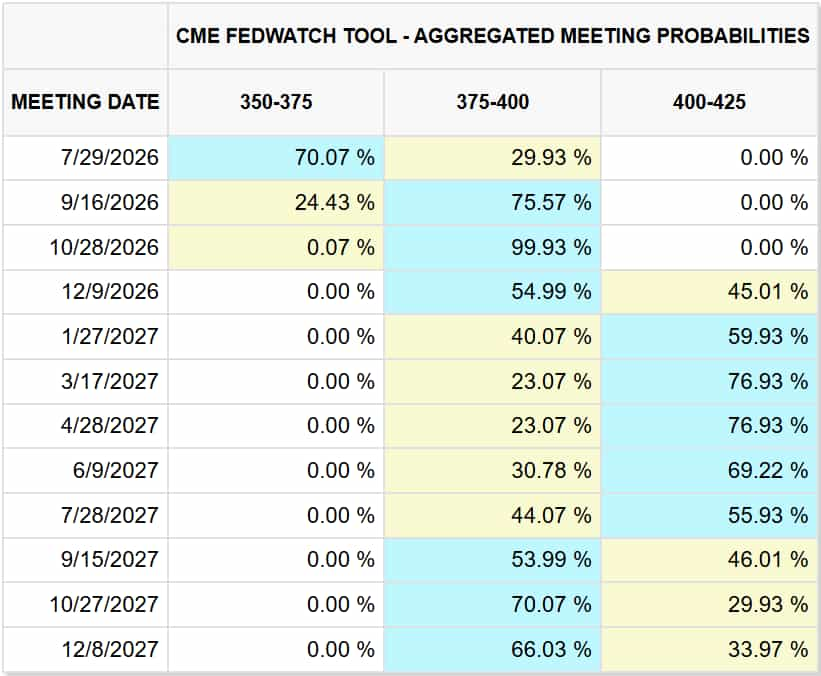

Markets repriced violently. Fed funds futures now reflect at least one 25-basis-point (bps) rate hike this year, and better-than-even odds of a second one. On a cumulative basis, the odds of at least one hike reach 99% by October. The chance of a second one by December is formidable at 45%. The about-face from the 50 basis points of cuts the market expected back in January seems complete.

Why the hawkish turn is well-founded

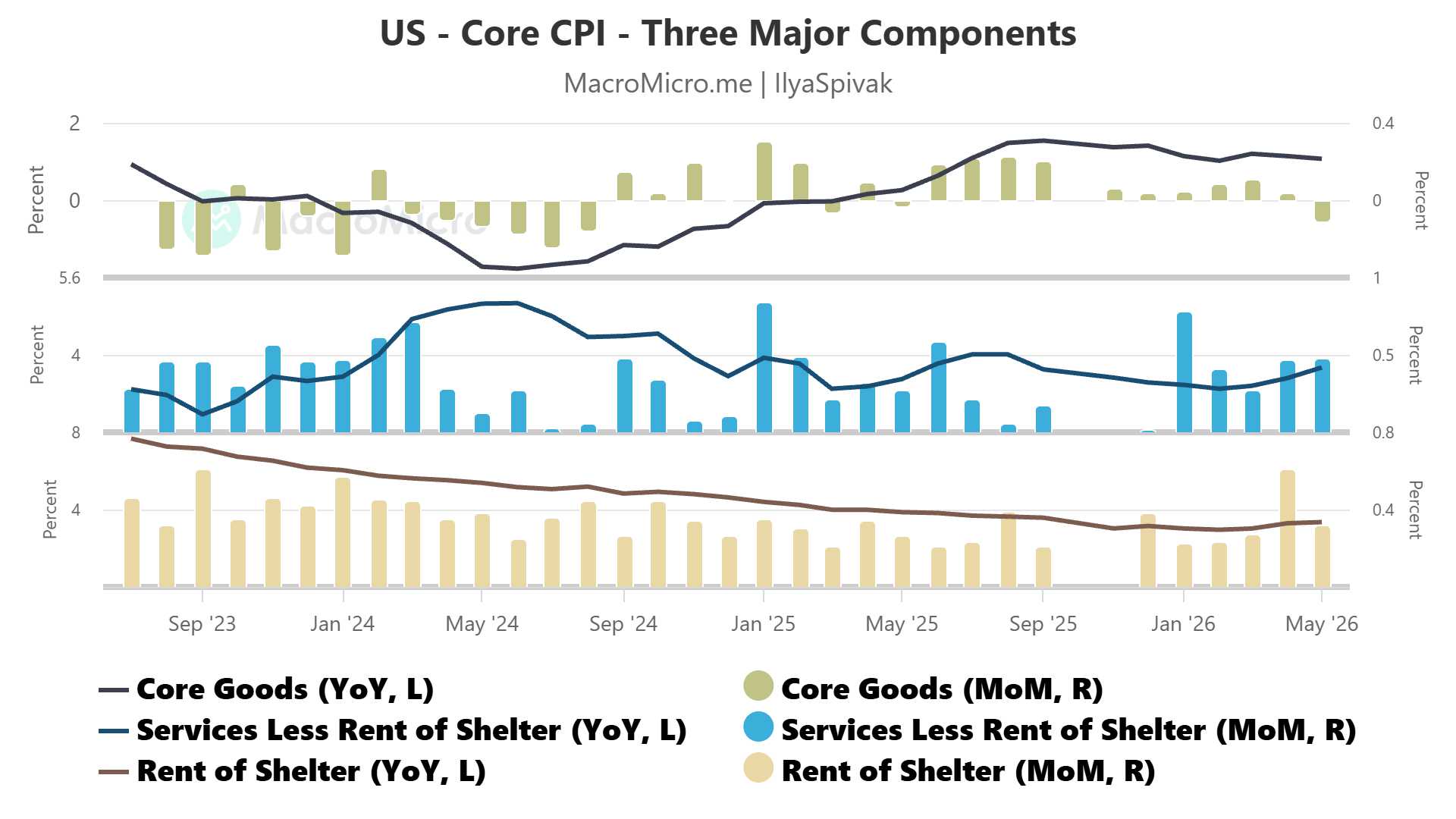

As jarring as the pivot looked, the inflation backdrop justifies it. The latest consumer price index (CPI) data showed core services inflation — the largest and stickiest component of overall price growth — rebounding to levels last seen in the middle of last year, before the disinflation that prompted 75bps of cuts in late 2025. Core goods prices slipped, but that mostly signaled early signs of demand destruction for energy-sensitive purchases like cars and auto parts. The energy shock from the war has been seeping into core costs through warehousing and freight, visible in both consumer and producer price data.

Moreover, the Fed was flagging inflation risks even before the war gave it more to worry about. That pressure traces to the peculiar shape of US economic growth this year. First-quarter gross domestic product (GDP) clawed back only about half the ground lost to the fourth-quarter government shutdown and managed that only because business investment — about 14% of the economy — grew at a scorching 10.4% annualized clip and out-contributed consumption, which is 68% of output and has decelerated for a second straight quarter.

Running one of the economy’s lesser engines that hot just to crawl forward may amount to overheating beneath a moderate-looking surface, an inflation risk all its own. Against that backdrop, Warsh’s unwillingness to lean dovish makes sense. The relief that lifted markets this week as the US and Iran embraced diplomacy has met a formidable obstacle. That rebound may prove to be not a turning point favoring the upside, but just another outturn on the path to a major market top.

Ilya Spivak, tastylive Head of Global Macro, has over 15 years of experience in trading strategy. He specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices