Will the Stock Market Fall if the Fed Gets Inflation Wrong?

Will the Stock Market Fall if the Fed Gets Inflation Wrong?

By:Ilya Spivak

Stock markets might have cheered as inflation expectedly fell, but fighting words from Fed Chair Kevin Warsh warned of trouble ahead.

- June’s US inflation data came in well below forecasts, with consumer prices falling month-on-month for the first time since 2020

- Bonds rallied on the news, then reversed hard after Fed Chair Kevin Warsh struck a firmly hawkish tone before Congress

- The soft reading looks like aged data, and the durable inflation threat from the AI boom is still building

Markets had plenty to digest — a softer inflation print, the first congressional testimony from new Federal Reserve Chair Kevin Warsh, a round of solid bank earnings — and the bellwether S&P 500 made almost nothing of it. The index kept grinding inside the narrowing range that has held it since mid-May on barebones trading volumes. The conviction was all in the bond market, where a telling round trip unfolded over the course of the day.

Bonds cheered the data, then Warsh changed their minds

Treasury bonds rallied hard when the soft inflation figures hit, briefly threatening to erase the previous day’s breakdown. Then Warsh took his seat on Capitol Hill, and his comments overturned the move almost entirely, pushing the 10-year note back and erasing most of the intraday rally.

That reversal reframed the whole session: the earlier rise now looked like a correction and the prior day’s breakdown like the real move, with the path of least resistance seemingly still favoring lower bond prices and higher yields. Gold prices broadly echoed the move, albeit with less conviction in either direction. The US dollar traced the same arc, dumping toward the bottom of its recent range on the data before recovering as Warsh spoke.

A downside surprise the market refused to trust

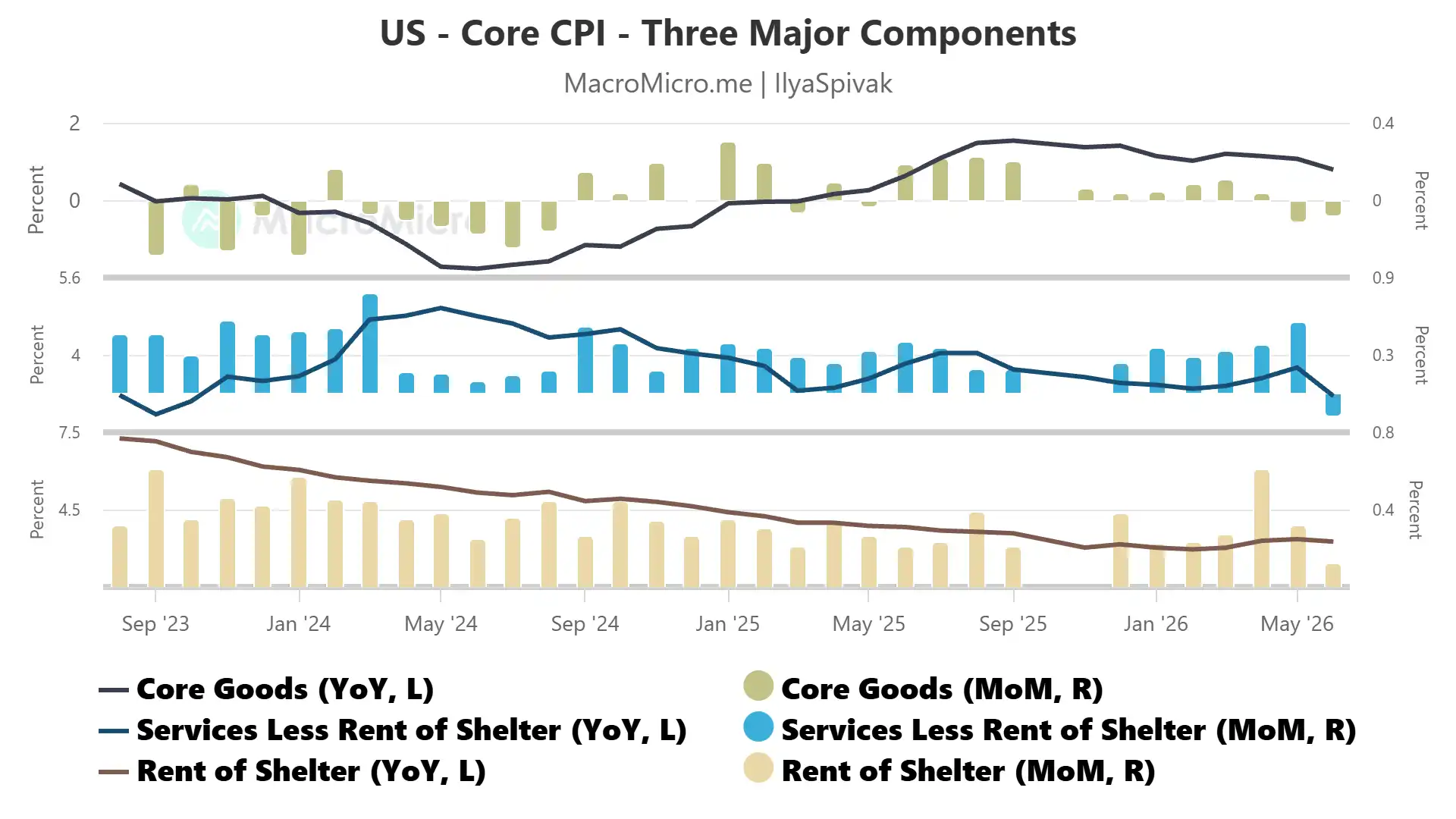

The US consumer price index (CPI) report was a genuine shock to the downside. Headline inflation slowed to 3.5% year-on-year against the 3.8% expected, but the core measure that strips out food and energy was the eye-opener, easing to 2.6% from 2.9% when forecasters looked for barely a wiggle.

On a monthly basis, consumer prices actually fell, marking the first outright decline since the onset of the COVID-19 pandemic. After months spent debating how much the war and the artificial intelligence (AI) boom would stoke inflation, a drop was not on most market-watchers’ scorecards.

Yet the market acknowledged the surprise and then pointedly waved it off. Part of the reason is that the data already looks stale. A cooldown in the energy component thanks to a sharp drop in oil prices in May and June was widely expected. That came alongside disinflation in core services, much of which may owe to categories tied to fuel. The cost of transportation services fell for a second month, for example.

With oil now surging again on renewed conflict near the Strait of Hormuz, improvements in these knock-on areas of sensitivity may reverse. The market smelled good news and declined to trust it as events on the ground unfolded.

A hawkish Fed with unfinished business

The bigger reason for the dismissal sat in the witness chair. Warsh could hardly have sounded more hawkish, telling lawmakers the Fed still has work to do, that higher inflation is not acceptable, and that its job is to keep isolated price changes from broadening out. He acknowledged the softer CPI report as a good step, then called it insufficient with much more work ahead. He too seemed to have seen the data and resolved to look past it.

Markets took the message. Futures still price at least one rate hike this year, and the outlook for 2027 lurched hawkish, with the odds of a hike by the end of next year climbing toward even money where traders had expected the tightening bias to fade quickly. The read-through is higher rates for longer, with cuts pushed well over the near-term horizon.

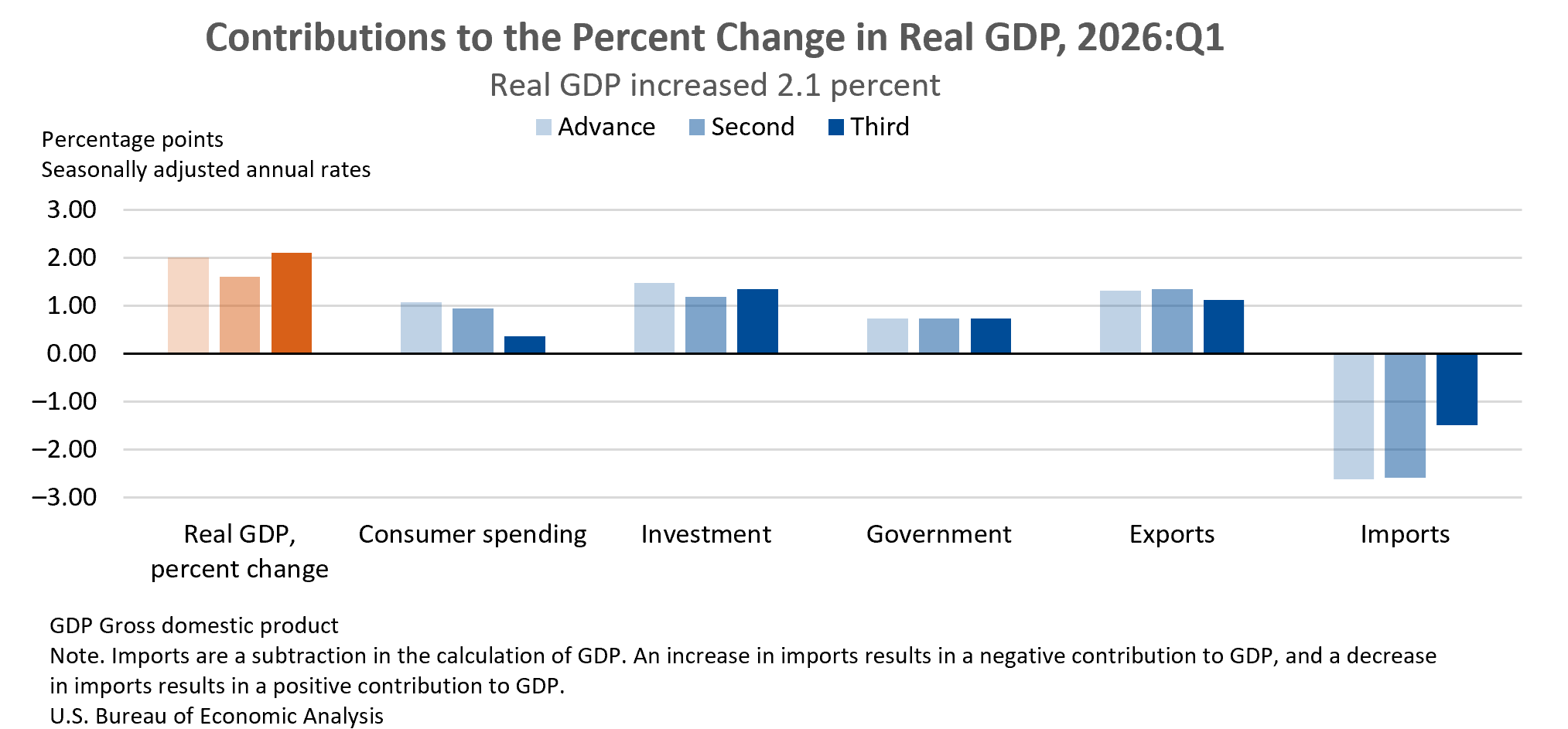

Minutes from last month’s Fed policy meeting put strong AI-related demand at the top of the list of culprits. The growth data shows why. First-quarter gross domestic product (GDP) rose 2.1%, yet the consumer — 68% of the economy — barely contributed, while business investment a fraction of its size did the heavy lifting, powered by the data center buildout and running north of a 10% annualized pace.

Growing that way is inherently inflationary, overclocking a small engine of demand at blistering speed while the far larger one stalls. That throws off inflation that squeezes households directly. That is a more durable threat than the on-and-off-again US-Iran war.

Incoming producer price index (PPI) data is the next test: core wholesale inflation is seen climbing to 5.2% from 4.9%. If the gain owes more to AI-driven demand than to oil, that will suggest that pressure on the consumer will continue to build from here.

The risk of a Fed too slow to turn

The setup looks precarious. The AI investment boom generating all this inflation is also draining households. Consumption is so much larger than investment that even a modest retreat in the former could overwhelm the uplift from the latter and drag growth into reverse.

The template is already on display abroad: June’s S&P Global purchasing managers index (PMI) survey data show manufacturing expanding across Australia, the Eurozone, and the UK even as those economies shrink, their dominant service sectors buckling amid a price squeeze. The US has not arrived there, but the mechanism on display is a cautionary tale.

A Fed this determined to break inflation may be slow to respond if that consumer-led downturn took hold, fixated on one side of its mandate, while the other quietly gave way. That delay is exactly the kind of policy error that leaves room for a painful slide in growth, and for the markets to reprice sharply once they see it coming. That may be why gold refuses to fall even as the dollar and bonds lean the other way, and why the consumer spending data due later this week suddenly carries real weight.

Traders were handed a soft inflation number today and chose to look through it. The greater danger is that the Fed, having done the same, also ends up looking through the slowdown until it is too late.

Ilya Spivak, tastylive Head of Global Macro, has over 15 years of experience in trading strategy. He specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices