Expect a Weak Dollar in 2024 Unless Stocks Drop, Says an Economic Model

Expect a Weak Dollar in 2024 Unless Stocks Drop, Says an Economic Model

By:Ilya Spivak

The U.S. dollar will be weak in 2024 according to a famous economic model, but its fortunes might quickly change if volatility spikes and stocks retreat

- Unrivaled liquidity makes the U.S. dollar different from other currencies.

- Middling U.S. growth relative to G7 peers may spell trouble for the dollar in 2024.

- The strength of the dollar may explode if Fed rate hikes trigger a spike in volatility.

The U.S. dollar occupies a special place in the global financial system. Data from the Bank of International Settlements (BIS)—the so-called “central bank for central banks”—reveals in its tri-annual survey of foreign exchange markets that as of 2022, the currency accounted for 88% of the total average daily turnover of $7.5 trillion.

That makes the greenback uniquely liquid, even when compared to broadly traded counterparts like the euro or the Japanese yen. For traders, this makes for price action dynamics unlike most other currencies. They have been famously illustrated by a model developed by economists Stephen Jen and Fatih Yilmaz called the “dollar smile.”

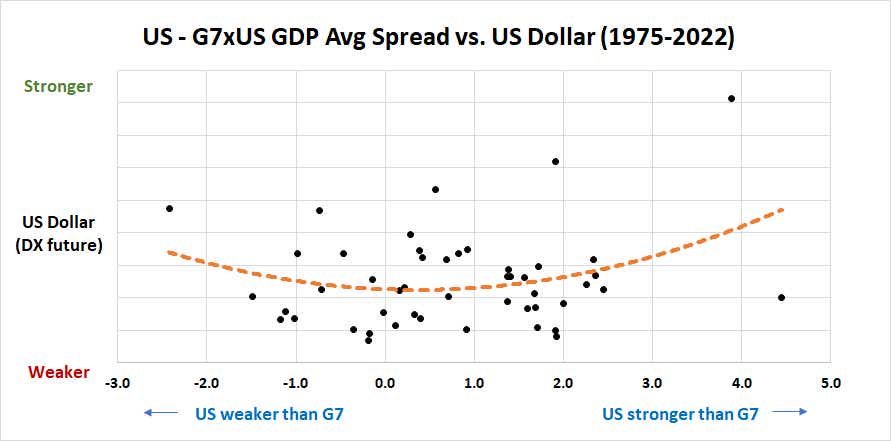

Thriving on extremes: The dollar-smile model

This framework ties the dollar’s performance to the relative strength of the U.S. economy against that of its peers. It reveals the currency tends to rise when U.S. growth either significantly leads or lags compared with average growth in the G7 economies (excluding the U.S. itself).

The right side of the chart tells a familiar story. When the U.S. economy is outperforming, brisk growth is bidding up inflation and pushing the Federal Reserve to raise interest rates. That expands the dollar’s yield advantage against its lagging counterparts and pushes it upward. This is the way most currencies tend to work.

The left side is where the dollar’s unique properties shine. The U.S. is the world’s largest economy. If growth there is lagging in a meaningful way, the knock-on effect on global growth at large is understandably damaging. It isn’t difficult to imagine that markets might turn defensive in such a scenario, with money flowing away from risky assets and toward safety.

It likewise follows that much of this “cashing out” tends to pour into the greenback. Its unrivaled liquidity means that it can absorb large-scale capital inflows with less volatility than the alternatives, which is a clear advantage at a time when investors are in flight mode. Its ubiquity also means that redeploying capital is easier after whatever scare subsides.

Either the dollar is in trouble, or stock markets are

Using this framework to map out where the dollar may be heading in 2024 produces ominous results. A Bloomberg survey of economists gives the U.S. an expected gross domestic product (GDP) growth premium of 0.78%. This lands squarely in the middling part of the smile chart, an area consistent with a weaker currency.

The lurking risk of a market shakeout may yet change this verdict.

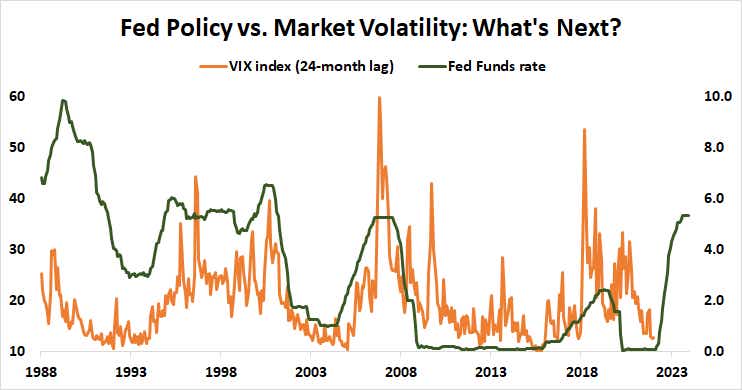

The modern financial and economic order has existed for just about four decades, emerging after the major currencies were untethered from gold convertibility. The VIX index of implied S&P 500 option volatility—investors’ so-called “fear gauge”—was launched in 1993.

Over the subsequent three decades, a sharp spike in the VIX has followed about two years after the start of a Fed tightening cycle. This echoes the central bank’s own estimate of 12-18 months for the economy to absorb a single hike. The latest rate hike cycle started in March 2022, putting the markets squarely in the danger zone as 2024 begins.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices