Battered Stock Market May See Good News in Gloomy Economic Reports

Battered Stock Market May See Good News in Gloomy Economic Reports

By:Ilya Spivak

Underwhelming U.S. GDP data and downbeat guidance from the Bank of Canada may signal cuts in interest rates next year

- U.S. GDP growth is expected to accelerate in Q3, but the pickup may be lackluster.

- A dour economic outlook from the Bank of Canada may indicate weakening U.S. demand.

- Stock markets may cheer outcomes signaling no further delay of Fed interest rate cuts.

The Federal Reserve left markets reeling with its policy update on Sept. 20, signaling in its Summary of Economic Projections (SEP) that interest rates will be higher by about 50 basis points (bps) next year than they were thought to be in June. Stocks fell as swelling term premium pushed up longer-term Treasury yields, pointing to rising uncertainty.

Speaking last week at the Economic Club of New York, Federal Reserve Chair Jerome Powell signaled this surge in borrowing costs may have already delivered the tightening that policymakers wanted, allowing hikes to stop. The key question from here is how long the U.S. central bank intends to hold rates at the highs before a round of cuts begins.

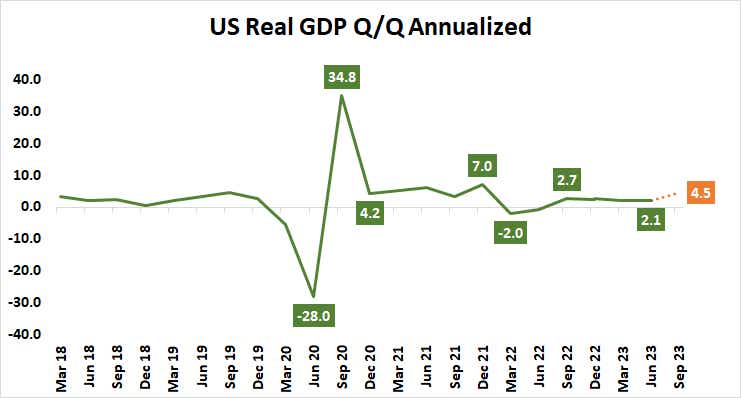

As it stands, the markets are pricing in the arrival of the first standard-issue 25bps reduction no later than July 2024. Another leg lower is penciled in by November. The probability of a third by year-end is assessed at 84%. This week’s arrival of third-quarter U.S. gross domestic product (GDP) data as well as a monetary policy announcement from the Bank of Canada (BOC) will test how this holds up.

U.S. economic growth trends: where are we going?

The GDP report is expected to show economic growth accelerated with gusto, pushing the annualized rate to 4.5% from the 2.1% recorded in the three months up to June. Leading surveys of purchasing managers (PMI) suggest economic activity has slowed more recently, warning that the heady uptick might be too backward-looking to sway Fed officials.

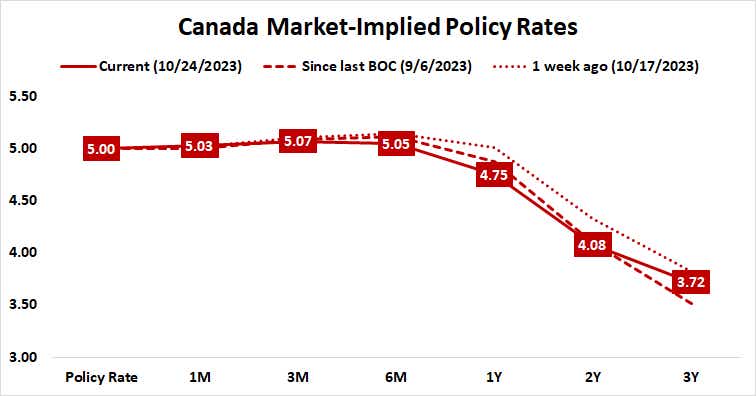

Meanwhile, the BOC is expected to keep its target interest rate unchanged at 5%. As with the Fed, the markets think July’s rate increase was this cycle’s last. From here, Canada’s central bank is priced in to remain on hold for the better part of a year, with cuts starting to appear in the closing months of 2024.

Nearly 80% of Canada’s exports are bound for the U.S. What’s more, a shock GDP contraction in the second quarter was driven by slumping external demand overpowering domestic growth. That means whatever BOC officials have to say about the way forward will be potent insight into economic conditions south of the Canadian border.

The trend in the second half of 2023 points to continued weakness. Exports continued to fall in July and August compared to the prior year, while PMI data suggests the manufacturing sector—ground zero for the influence of US-driven supply chains—shrank at an accelerating pace. The third quarter may be even softer than the second.

Financial markets are pining for Fed rate cuts

Taken together, the picture painted here might prove curiously supportive for financial markets.

The jump in GDP might be underwhelming. The outcome would need to overcome economists’ already rosy expectations to alter the Fed’s calculus meaningfully, which seems unlikely. What’s more, a soggy outlook from the BOC would bolster the sense that signs of strength are stale, lagging a subsequent downturn that is already underway.

Stock markets might have hopes for the shortest possible delay before the arrival of monetary stimulus. In tandem, a pullback in bond yields may be accompanied by a retreating U.S. dollar as the window for further expansion of the currency’s yield advantage against its major peers is shuttered.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices