U.S. NFP Preview: Stocks at Risk as Recession Fears Top Fed Rate Cut Hopes

U.S. NFP Preview: Stocks at Risk as Recession Fears Top Fed Rate Cut Hopes

By:Ilya Spivak

U.S. jobs data may come out weaker than the markets are expecting. If that spooks stocks despite building Fed rate cut expectations, more trouble is probably ahead.

- Stock markets may be losing their appetite for soft U.S. economic data.

- November’s employment statistics may end up weaker than expected.

- There’s trouble ahead if Wall St. can’t rally on firmer Fed rate cut bets.

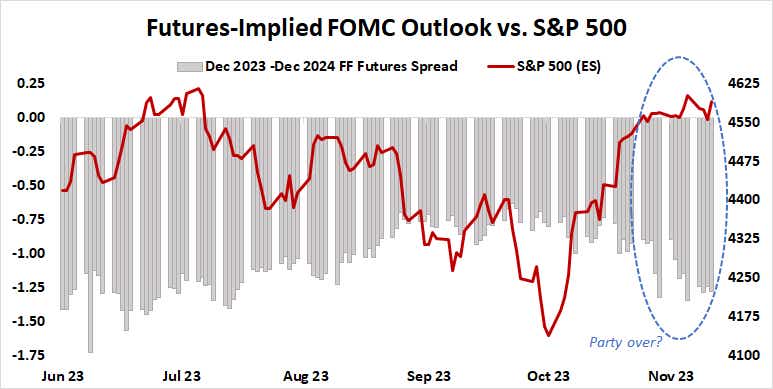

A mere two weeks ago, financial markets might have been expected to loudly cheer at the sight of any economic data that seemed to bring the Federal Reserve closer to cutting interest rates. In fact, November was defined by blistering gains in stocks and bonds together on this very premise.

Last week, something appeared to change. Wall Street was conspicuously unimpressed as bond yields continued to plummet. The U.S. dollar managed a small gain. It seemed the market was no longer content to celebrate cheaper money and starting to wrestle with why it was probably on the way: looming recession.

Stock market and U.S. economic data: defining “good” vs. “bad”

More confirmation seemed to emerge this week. U.S. stocks managed a mere hour of gains after a disappointingly low reading on November’s estimate of private-sector payrolls growth from Automatic Data Processing (ADP). The bellwether S&P 500 then turned promptly lower and finished the day down 0.4%.

The stickiness of these emerging price dynamics was tested again with the weekly jobless claims release. This helpfully showed the process working in reverse. Continuing claims—a gauge of how hard it is for the recently unemployed to find new work–printed notably lower than expected. Stocks roared higher in response.

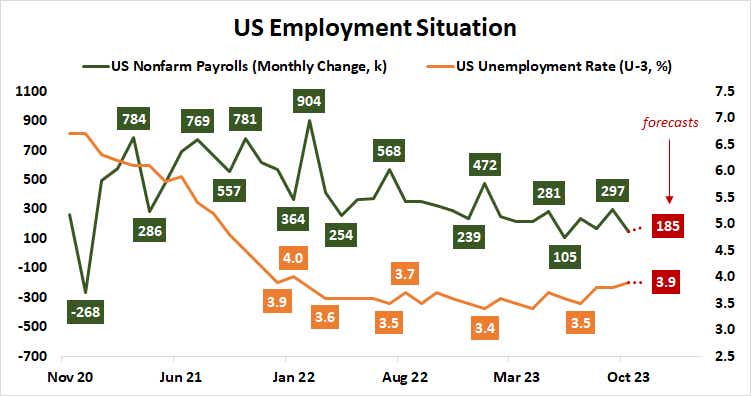

The spotlight now turns to November’s official set of U.S. employment figures. Analysts expect it to show that 185,000 jobs were added to nonfarm payrolls, a mild pick-up from October’s 150,000. The jobless rate is seen steady at 3.9% while average hourly earnings growth—a measure of wage inflation—slows to a 29-month low of 4% year-on-year.

U.S. jobs report: who’s surprised?

Leading purchasing managers index (PMI) data from S&P Global suggests that last month, employment across the manufacturing and service sectors shrank in tandem for the first time since mid-2020. Analog data from the Institute of Supply Management (ISM) was only a touch more encouraging. It put service-sector hiring at near-standstill.

How markets respond if echoes of that weakness are on display in the government’s own numbers may be critical. Soft outcomes will help underpin last month’s tectonic dovish move in the rates outlook. If that spooks stocks as traders see the pain behind the policy pivot, 2023 may well end on a whimper.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices