BoE Meeting: After the Fed and the ECB, All Eyes Turn to the Bank of England

BoE Meeting: After the Fed and the ECB, All Eyes Turn to the Bank of England

By:Ilya Spivak

The markets punished the Fed but praised the ECB as both central banks pressed on with rate hike plans to fight inflation despite banking crisis fears. How will the Bank of England fare?

- The Bank of England is next up to face the inflation, bank crisis trade-off

- Markets all-but certain that a 25bps rate hike is coming, but what’s next?

- Will the BOE be praised like the ECB or punished like the Federal Reserve?

BOE next up to reconcile inflation fight, banking crisis

The time has come for the Bank of England (BOE) to take its turn at trying to reconcile an ongoing battle against inflation with a banking crisis that ripped through global markets this month. The panic took down Silicon Valley Bank (SVB) and Signature Bank in the US while forcing UBS into a shotgun marriage with Credit Suisse in Switzerland.

The ECB and the Federal Reserve paved the way. Both stuck to their guns on interest rate hikes, for the most part. The Eurozone took a somewhat harder line last week, raising rates by the 50 basis points (bps) it all-but-promised in February while assuring investors that it could deal with any unsavory side effects as a separate matter. The Fed delivered the 25bps hike needed to credibly stay in the game but somewhat softened its messaging about on-going increases. Nevertheless, Fed Chair Jerome Powell strenuously claimed that fighting inflation is the top priority for policy.

The BOE has been treated to a timely reminder of the price growth problem just earlier this week. Data published on Wednesday put yearly CPI inflation at 10.4 percent in February, an unexpected rise from the 10.1 percent recorded in the prior month. Economists penciled in a decline to 9.9 percent ahead of the release. Core CPI excluding volatile food and energy prices rose 6.2 percent, topping January’s 5.8 percent. Here too, a decline was anticipated.

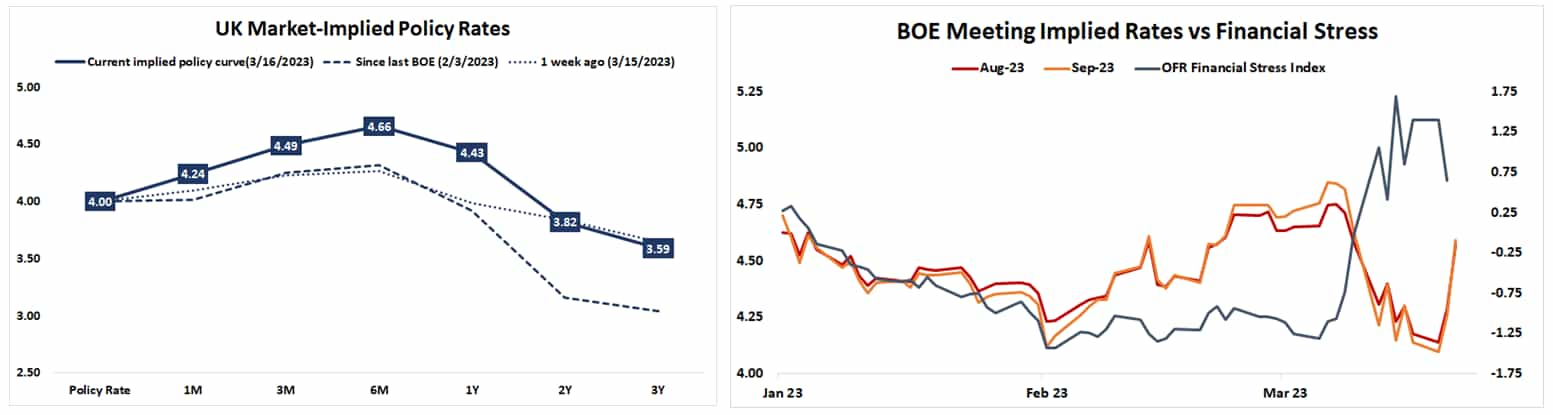

Letting the hawks fly

Data source: Bloomberg

The markets seem to be giving Governor Andrew Bailey and company a clear path forward. The yield curve has shifted meaningfully higher compared with a week ago. Market-implied rates for the current cycle’s anticipated peak in the third quarter have shot up as banking crisis fears receded and credit markets eased.

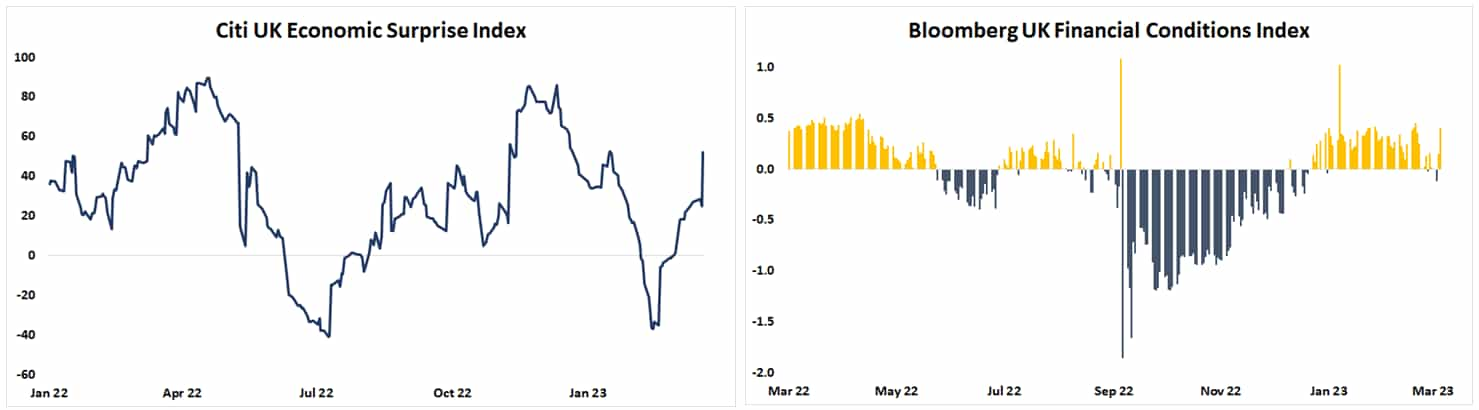

Aside from double-digit CPI growth, the economic backdrop is helpfully compliant. UK economic data outcomes have sharply improved relative to baseline forecasts in recent weeks, according to figures from Citigroup. Meanwhile, a Bloomberg gauge of financial conditions shows that – but for a blip amid the initial outbreak of the SVB fiasco – credit remains plentiful and accessible.

Data source: Bloomberg

More like the Fed or the ECB?

All this is almost certainly baked into asset prices, however. Indeed, the probability of a 25bps rate hike is priced in at a commanding 88 percent. This means that the market-moving portion of the announcement will concern what happens next, and here there is some controversy.

The BOE signaled in February that it is now treating each policy call as a stand-alone matter, with the decision dependent on how the data evolves between meetings of the rate-setting MPC committee. The markets are now priced for one more rate hike before the end of the year if today’s increase goes forward. Officials may not be ready to endorse such a thing, especially after the recent troubles in the banking sector.

The markets rewarded the ECB for going through with its rate hike with a brave face on: European bank shares rose alongside the Euro. They punished the Fed for even an inkling of caution: stocks fell on Wall Street and the US Dollar broadly weakened. If the BOE seems like it might pull the brakes after this outing, it too may be rebuked by investors.

Ilya Spivak is the Head of Global Macro at tastylive, where he hosts Macro Money every week, Monday-Thursday.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices