Weak Inflation Data Shows the Economy in China Remains in Trouble

Weak Inflation Data Shows the Economy in China Remains in Trouble

By:Ilya Spivak

China’s economy is in trouble, and Beijing is not doing enough to fix it.

- Weak inflation data shows China’s economy remains in the doldrums.

- Traders are eying the March NPC meeting with hope, but the markets remain weak.

- China must go beyond its “bait-and-switch” fiscal policy to woo investors.

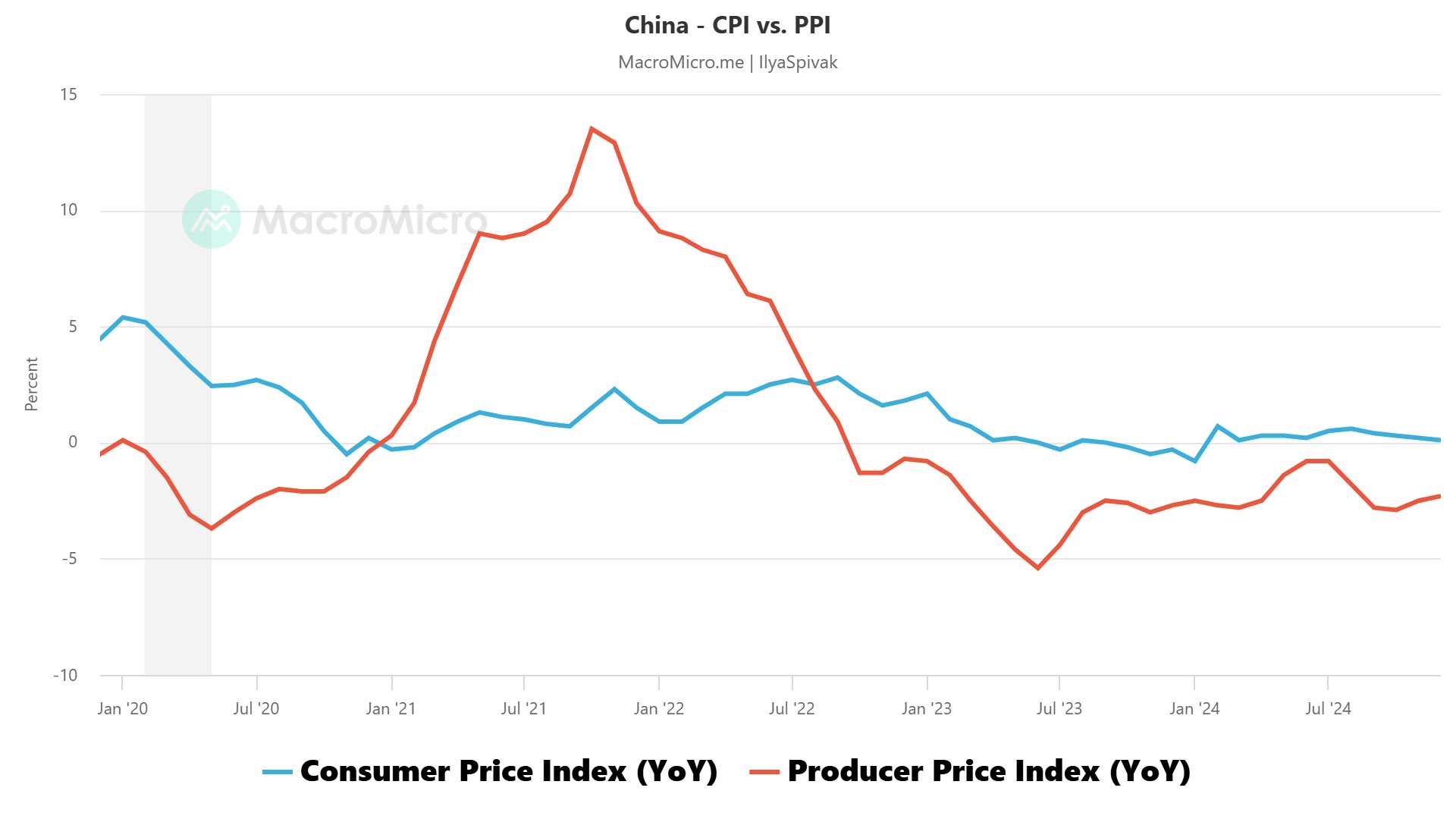

China reported another set of anemic inflation data, signaling the world’s second-largest economy remains in the doldrums. Consumer prices (CPI) grew just 0.1% year-on-year in December, the slowest in nine months. Producer prices (PPI)—a wholesale inflation gauge—fell 2.3% year-on-year, a limp uptick after a 2.4% drop in November.

More broadly, Chinese inflation has been all-but nonexistent since April 2023. This speaks to the absence of demand that has plagued the economy since it emerged from “zero-Covid” lockdowns in late 2022. Purchasing managers’ index (PMI) data reveals an upswell of activity in the first quarter of 2023, followed by a rapid return to a near standstill.

Weak inflation speaks to absence of demand in China

Indeed, real gross domestic product (GDP) growth has outpaced nominal expansion for six consecutive quarters. This implies negative price growth at the economy-wide level to the tune of 0.9 percentage points of gross domestic product (GDP) on average since would-be “reopening” momentum fizzled. A dizzying array of stimulus measures has failed to work so far.

Financial markets have long hoped that China will come around to delivering a big dose of demand-replacing fiscal stimulus to kickstart activity. They roared with approval in September when the Politburo—the country’s steering committee of 24 officials including President Xi Jinping—hinted at such a possibility. Concrete steps are yet to materialize.

Markets will be watching the annual session of China’s broader parliament—the National People’s Congress (NPC)—in early March to see if Beijing is finally ready for some heavy lifting. The target for the year’s budget deficit may be especially telling, according to a report from Reuters. A rise from 3% to 4% may signal expansionary intent.

China needs to get serious about fiscal policy

Meanwhile, The Economist reports that persistent economic malaise is straining the social order. Random acts of violence—so-called “revenge on society” attacks, like knifings and cars driven into crowds—increased in 2024. The rise was large enough that officials promised a harsh crackdown. Ironically, that might dampen consumer confidence further.

.png?format=pjpg&auto=webp&quality=50&width=1920&disable=upscale)

Tellingly, China’s CSI 300 stock benchmark, an index of the top issues in Shanghai and Shenzhen, is starting 2025 pinned to three-month lows. Among the standby “China proxy” assets, the Australian dollar has slid to the weakest point since October 2022. Copper has bounced from recent lows, but a Bloomberg report chalks this up to U.S. tariff fears.

Bargain-hunting investors pounce on beaten-down assets when the stock of bad news seems to be exhausted, long before evidence of improvement can be seen in earnest. That may eventually make Chinese and related markets an attractive opportunity, but any such move will struggle if the “bait-and-switch” approach to fiscal policy persists.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices