China's Economy is Weaker Than it Seems. Here is How to Trade It

China's Economy is Weaker Than it Seems. Here is How to Trade It

By:Ilya Spivak

China’s first-quarter GDP data is less rosy than it seems, with a familiar growth strategy seemingly misfiring. Traders may look to the Australian dollar rather than stocks to take a view.

China’s GDP data hints at a pickup, but trouble lurks under the surface

A familiar Beijing strategy of growth by decree might not work anymore

Traders betting on China’s weakness may look to the Australian dollar

Look on the surface, and China’s economy performed better than market-watchers expected in the first quarter. Gross domestic product (GDP) grew 5.3% year-on-year, marking the fastest expansion since the second quarter of 2023 and the third consecutive period of acceleration. The outcome topped forecasts penciling in a rise of 5%.

That rosy vision is quickly tarnished, however. For the fourth quarter straight, China’s real GDP growth outpaced the nominal side. The implications are ominous. Real GDP is calculated by subtracting inflation from the nominal reading. If the former is printing higher than the latter, the price growth coefficient is negative.

China’s economy: less than meets the eye

What’s more, the deflationary gap is widening. In the first quarter, it registered at a hefty 1.2 percentage points, the largest since the measure turned negative in the three months to June 2023. This speaks to anemic economy-wide demand. Prices fall when absent uptake forces discounting.

_april_18.png?format=pjpg&auto=webp&quality=50&width=1000&disable=upscale)

Put simply, the cost of goods and services rises when supply is unable to keep up with demand and buyers must compete on price for access. When the opposite occurs, it speaks to sellers awash in unwanted supply, so prices are slashed as they try to tempt would-be buyers to clear inventories.

Retail sales and industrial production figures released alongside the GDP report underscore the problem. The former grew just 3.1% year-on-year in March, slower than the 4.5% expected and the weakest since July 2023. The latter added 4.5% over the same period. That undershot bets on a rise of 5.4% to post the slowest rise in four months.

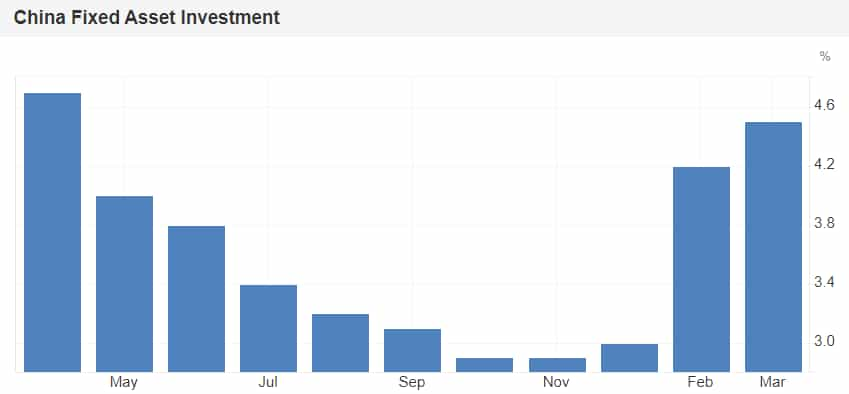

A familiar game: can China still grow by decree?

The standout came from fixed asset investment. That grew 4.5% year-on-year in March, the fastest since April 2023. In fact, capital expenditure (CAPEX) has sharply accelerated in the first two months of the year, marking a stark departure from the shallow downtrend carved out since February 2022.

This hints that China is attempting to return to a familiar growth hack: a centrally mandated buildout of fixed assets – roads, bridges, train lines, airports, and even whole cities – that pours demand on the economy by decree.

However, unlike the strategy’s heyday in the three decades before the COVID-19, the capital flows to sustain it are now mostly absent.

China depended on its role as the go-to middle step for value-add production in the global supply chain to generate large capital inflows, creating an offset for Beijing’s largesse. That well is running dry because China’s belated reopening after the pandemic and its more assertive geopolitical stance have encouraged business to diversify elsewhere.

Exports and imports have been trending lower for three years. Both recorded negative year-on-year growth readings in March. Meanwhile, foreign direct investment (FDI) is shrinking rapidly, down nearly 20% year-on-year in February. That is the largest decline on record since at least 2015.

On balance, this warns that the artifice of Chinese economic reacceleration may quickly unravel.

Trading that thesis with a bet against local stock markets seems dangerous, however: Beijing has directed the investment arm of its sovereign wealth fund to buy domestic shares, manufacturing a brisk recovery. The FXI ETF tracking large-cap Chinese stocks is up nearly 15% from its lows in late January.

Trading China’s economic weakness: the Australian dollar

An alternative vehicle to express a view may be the Australian dollar. It is highly sensitive to China’s business cycle because the East Asian giant is Australia’s biggest export market and a key buyer of the country’s mining output, a critical engine of growth and inflation.

The so-called “aussie” has broken range support at 0.6450 that was arresting losses since mid-February. That seems to open the door for a decline to test the October-November 2023 floor clustered around the 0.6300 figure. Reclaiming a foothold back above 0.6500 might invalidate the bearish narrative, at least in the near term.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices