Stocks May Fall with the U.S. Dollar as PMI Data Fuels Recession Fears

Stocks May Fall with the U.S. Dollar as PMI Data Fuels Recession Fears

By:Ilya Spivak

The markets fear that failing U.S. economic strength may bring on global recession

- S&P Global PMI data showed the U.S. economy slowed to near-standstill in February

- Weakness in the service sector looks especially ominous despite manufacturing uptick

- Stocks may fall further with yields and the dollar amid building global recession fears

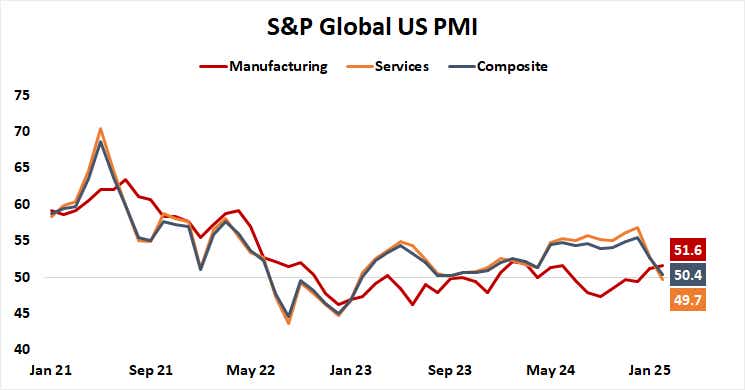

The global economy is losing the last line of defense against the onset of recession. That’s the message emerging out of sobering purchasing managers index (PMI) data from S&P Global that showed U.S. economic activity growth nearly stalled in February. The pace of expansion slowed sharply to the weakest in 17 months.

Perhaps most ominously, the weakness came from the mission-critical service sector. The PMI gauge tracking its performance fell below the “50” boom-bust level separating expansion from contraction for the firs time in 25 months. New orders growth fizzled, and business sentiment soured, reflecting “uncertainty [about] government policies.”

PMI data warns that U.S. economic strength is unraveling

Manufacturing activity picked up a bit, accelerating for a second month after launching sharply higher in January. This month’s result marks the fastest growth since June 2024. The PMI report struck a cautious tone however, warning that part of this strength reflected the front-running of tariffs and so appeared to be temporary.

All the same, it is the service sector that matters most because of its outsized contribution to U.S. employment and overall economic growth. At close to 70% of overall gross domestic product (GDP), it far outweighs the impact from manufacturing and agriculture. Demand dynamics after the COVID-19 pandemic have seen it dominate still further.

The latest consumer price index (CPI) data from the Bureau of Labor Statistics (BLS) reveals two critical insights. First, that 2.62 percentage points (ppt) of January’s 3% year-on-year inflation rate was contributed by core services, while the goods side shaved off 0.03ppt. This implies that demand is overwhelmingly skewed to the service sector.

Stocks and the U.S. dollar may fall as global recession worries build

Second, despite accounting for a dominant 87% of January’s headline CPI reading, services’ contribution declined from 93% in the prior month and marked the lowest share of the total since April 2023. This echoes the message on display in the PMI report, warning that the indispensable engine powering U.S. economic growth is misfiring.

.png?format=pjpg&auto=webp&quality=50&width=751&disable=upscale)

In turn, this means that global recession risk is building. Throughout the second half of 2024, the U.S. stood alone as a pillar of economic strength while the other major drivers of worldwide growth – the Eurozone and China – slumped toward standstill. They remain there still, even as the U.S. converges on their weakness.

Financial markets offered a telling response last week. Stocks fell alongside Treasury yields and the U.S. dollar while bonds, gold, and the perennially anti-risk Japanese yen recorded potent gains. Analytics from Citigroup warn that U.S. data outcomes now tend toward underperformance relative to forecasts, warning more of the same is ahead.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices