Kelly's Criterion Explained: A Q&A Guide for Options Traders

Kelly's Criterion Explained: A Q&A Guide for Options Traders

By:Kai Zeng

It helps determine the right amount of cash to risk on a trade

This is part 1 of a 3-part series. Part 1, Never Go Broke: The Kelly Formula Explained, can be found here.

Many readers wrote in with questions to Part 1, which prompted this series.

The Basics

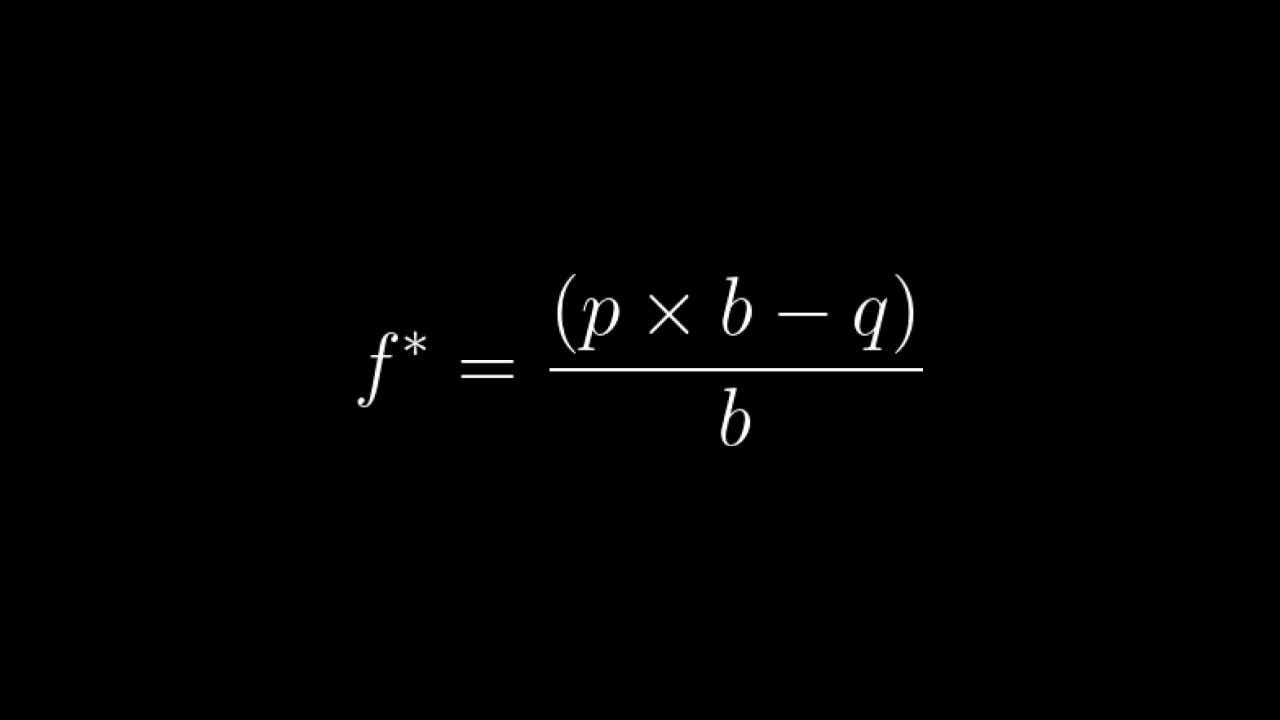

Q: What is Kelly's criterion and how is it calculated?

A: Kelly's Criterion determines the optimal percentage of your capital to allocate to a trade:

Where:

f* = optimal bankroll percentage to allocate- p = winning probability

- q = losing probability (1-p)

- b = net odds received (amount won per dollar bet)

Profitability Assessment

Q: Is there a quick way to determine if a strategy can be profitable long-term based on Kelly's calculation?

A: Kelly's formula can be simplified as:

.jpg?format=pjpg&auto=webp&quality=50&width=1280&disable=upscale)

We can set f to 0 as a threshold and evaluate whether our received odds exceed the theoretical requirement for a given POP or success rate.

When f = 0%, the formula changes to:

.jpg?format=pjpg&auto=webp&quality=50&width=1280&disable=upscale)

In our iron condor example, with p = 0.85 (success rate) and q = 0.15 (losing rate), the odds (b) must exceed 0.15/0.85 = 0.176 for the strategy to be potentially profitable in the long run.

.jpg?format=pjpg&auto=webp&quality=50&width=1280&disable=upscale)

Position Management

Q: When managing positions at 50% profit, should I reference POP or P50 on the tastytrade platform? What about managing at 21 DTE?

A: The p (probability of profit) in the calculation of Kelly should match the way we manage the positions. If the position is managed at 50% winners, P50 is better than POP.

However, the realized success rate is even more accurate than the theoretical POP or P50. Traders can find the success rate of managing at 21 DTE or any other mechanics by running the lookback program on tastytrade or from our Market Measures.

Capital Allocation

Q: Does the Kelly number change based on the fluctuation of the bankroll (net liq) in the account?

A: Kelly represents the percentage of capital allocation of a certain portfolio. In our analysis, we keep this number constant, but the net liq can fluctuate after trading. Keeping the Kelly at the same level, we should expect to see more committed capital per trade if the net liq increases.

Calculating Odds

Q: How are net odds calculated?

A: Odds (b) = expected win/expected loss.

It’s better to use the realized average win/average loss in this calculator. We can get these values after analyzing long-term data (lookback or from Market Measures). Using max profit/max loss is not so reliable because, in premium selling strategies, we often experience partial winners and losers.

For probability, we should use either P50 or the realized success rate when managed at 50% winners.

Kelly Fractions

Q: What's the importance of using a fraction of the calculated Kelly in real trading?

A: The Kelly number, or what we call full Kelly, is the scenario to optimize the return without considering the volatility. In practice, the half-Kelly (50% of the full Kelly) strategy can capture nearly 71% of the optimal returns with only about 38% of the volatility.

.jpg?format=pjpg&auto=webp&quality=50&width=1280&disable=upscale)

The relationship is not linear. The half Kelly thus has a higher risk-adjusted return. Using a Kelly fraction provides a better balance between returns and risk.

Risk of Ruin

Q: Does a 0% ruin rate mean that the strategy is completely safe from losing all capital?

A: If the Kelly is positive, traders should theoretically be able to avoid depleting their capital. However, perfect sizing is difficult to achieve in real trading. Also, a streak of losing events is possible. These would cause the portfolio to achieve the expected return in a longer period of time.

Kai Zeng, director of the research team and head of Chinese content at tastylive, has 20 years of experience in markets and derivatives trading. He cohosts several live shows, including From Theory to Practice and Building Blocks. @kai_zeng1

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices