Vulnerable Stocks, Big-Box Store Earnings and Recession Risks Resurface

Vulnerable Stocks, Big-Box Store Earnings and Recession Risks Resurface

By:Ilya Spivak

Macro events that may move the markets this week

- Stocks down, U.S. dollar up as markets see “higher for longer” Fed rates path.

- Cooling momentum in U.S. economic data flow warns of global recession risk.

- U.S. retail sales, big-box stores’ Q2 earnings, July FOMC meeting minutes due.

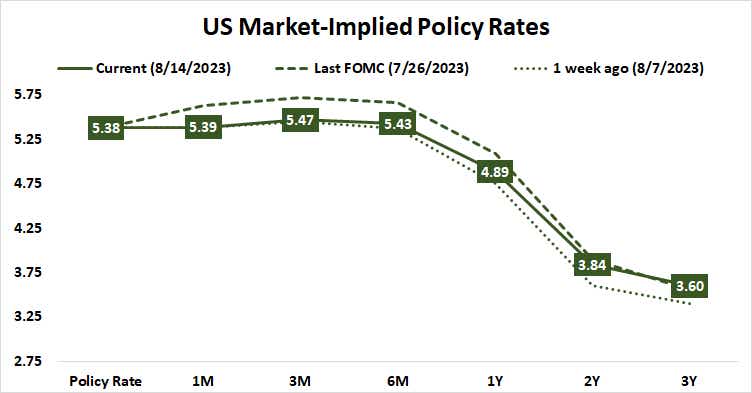

Stocks fell on Wall Street while the U.S. dollar rose last week, as expected. Repricing Federal Reserve policy expectations to a “higher for longer” interest rate path seems to be the most often cited explanation swirling around the markets.

That makes some sense. While the probability of another rate hike in 2023 hasn’t budged – the markets still see July’s 25-basis-point (bps) rise as having capped the tightening cycle – the projected timing and scope of the easing to follow have shifted to a relatively less dovish setting.

The rates trajectory implied in Fed Funds futures shows the probability of a cut in March 2024 has nearly halved, falling from 79% to 42%. The rate expected by year-end has risen from 3.9% to 4.23%. In all, traders shaved off about one standard-sized rate cut from the forecast.

The bond market adjusted accordingly. The ten-year Treasury bond fell 0.86% while five- and two-year paper fell 0.57% and 0.18% respectively. This echoes the sense that most of the adjustment impacted longer-dated rates view rather than expectations for the U.S. central bank’s immediate next steps.

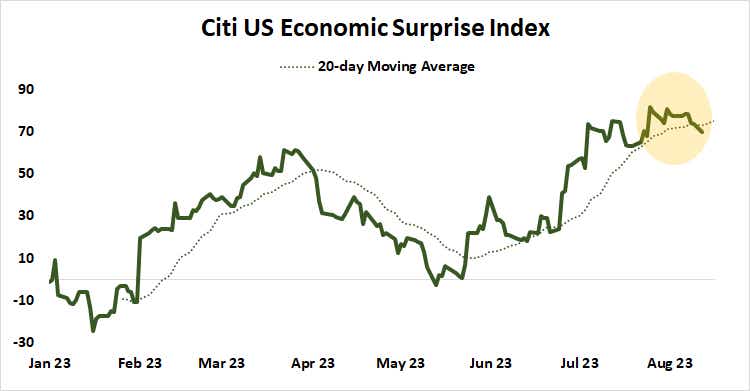

Fed rates outlook steepens even as US economic momentum slows

A look at the economic data flow crossing the wires alongside this repricing makes for a murkier picture. July’s U.S. employment report offered mixed results: nonfarm payrolls disappointed but the jobless rate ticked a bit lower. The headline consumer price index (CPI) inflation print was a bit softer than expected.

Data from Citigroup reveals that – while US economic outcomes still have an overall tendency to print north of economists’ median forecasts – momentum peaked in late July and has now cooled for two consecutive weeks. That seems to run counter to an upshift in the expected Fed rates path unless the markets were primed for something worse.

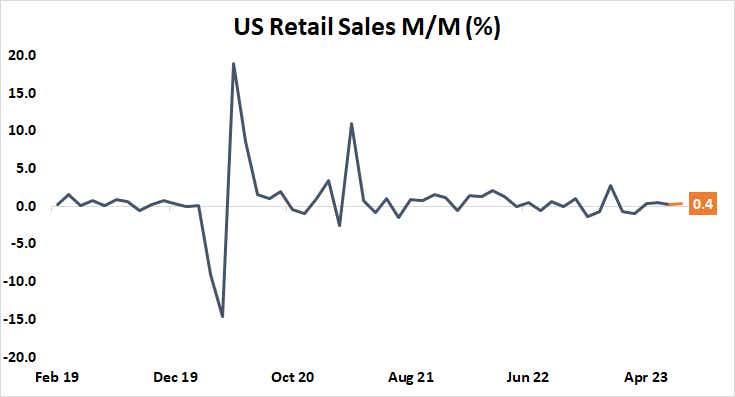

U.S. retail sales data, key earnings reports eyed

This weakening comes amid a dour backdrop elsewhere. The Eurozone—collectively about 15% of the global economy—is flirting with recession, if not already in one. China—the world’s second-largest economy at close to 18% of the worldwide whole—is still struggling to recover after reopening from “zero-COVID” restrictions in December.

That makes United States the last line of defense against global recession, putting the burden squarely on U.S. consumers. With that in mind, traders will probably have keen interest in July’s retail sales report. Receipts are expected to rise 0.4% from the prior month. Meanwhile, a trio of top retailers—Home Depot (HD), Target (TGT) and Walmart (WMT)—are set to report second-quarter earnings.

Stocks may continue lower as the greenback gains if sales data prints on the soft side while forward guidance from big box stores points to ebbing appetite from US consumers. The “higher for longer” overlay may fade however, giving way to a more overtly risk-off tone where Treasury yields decline and the defensively minded Japanese yen rebounds.

Fed vs. markets on interest rate expectations

Minutes from last month’s meeting of the Federal Reserve’s policy setting FOMC committee are also likely to command attention. Traders will be keen to gauge the extent to which Chair Jerome Powell and company perceive and are worried about the risk of a downturn in the U.S. business cycle, and how that aligns with their focus on delivering disinflation.

The Fed estimates it can take 12 to 18 months for the impact of a single rate rise to be fully absorbed into the economy. So, pressure from the bulk of last year’s outsized 50- and 75-basis-point rate hikes ought to be appearing right about now. Markets still see rate cuts appearing in the second quarter of next year. If they seem like a more distant prospect for central bank officials, risk appetite may be eroded still further.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices