U.S. NFP Preview: Stocks and Bonds at Risk as Fed Rate Cut Bets Deflate

U.S. NFP Preview: Stocks and Bonds at Risk as Fed Rate Cut Bets Deflate

By:Ilya Spivak

If middling U.S. employment data argues against aggressive interest rate cuts, stocks and bonds may keep falling, gold will struggle and the dollar may mount a comeback

- Stocks and bonds have suffered so far in 2024 as markets question Fed rate cut bets.

- The U.S. employment report is now in focus, with broadly on-trend results expected.

- Middling results might cool stimulus speculation further, feeding the risk-off mood.

Financial markets returned from the New Year holiday in a defensive mood. The bellwether S&P 500 stock index is on track for its first weekly decline since late October, threatening to end a blistering nine-week winning streak. Against this backdrop, Treasury bonds are down as yields march higher across maturities.

Price action tells a similar story in currencies and commodities. The U.S. dollar is rebounding, with an average of the currency’s value against its top counterparts up over 0.8% so far this week as it tries to break a three-week run of losses. Gold is a mirror image of the greenback, trading on pace to snap three weeks of gains with a loss of nearly 1%.

A unifying theme seems to have emerged from the very first trading day of 2024: The markets seem determined to unwind some of the heady moves playing out in November and December amid a euphoric upwell of risk appetite across the asset spectrum. Traders were celebrating as the Federal Reserve appeared to endorse building interest rate cut bets.

All eyes on the U.S. jobs report

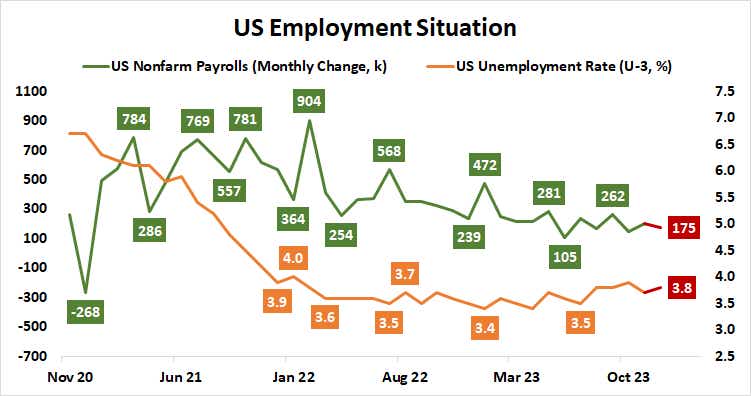

The spotlight now turns to December’s much-anticipated U.S. employment report. It is expected to show an increase of 175,000 in nonfarm jobsd while the unemployment rate edges up modestly to 3.8%. Average hourly earnings are rising 3.9% year-on-year, amounting to the slowest wage inflation since June 2021.

On balance, these would be middling outcomes. The pace of monthly payroll growth would land comfortably within the 105,000 to 262,000 range in place since mid-2023. The jobless rate would look similarly staid within the 3.4% to 4.0% range containing outcomes since January 2022. Even wage growth would be only slightly below the three-month average of 4.1%.

Analytics from Citigroup suggest U.S. economic data outcomes have increasingly converged on consensus forecasts since mid-August as market watchers upgraded growth expectations for 2024. That seems to imply that analysts’ models are relatively well-tuned to economic reality, making sharp deviations from the baseline seem less likely.

This raises a familiar question: if the “slow and steady” vision of the U.S. business cycle remains undisturbed, does it seem plausible the Federal Reserve must issue a blistering interest rate cut cycle in the months ahead?

Fed interest rate cut expectations: too far, too fast?

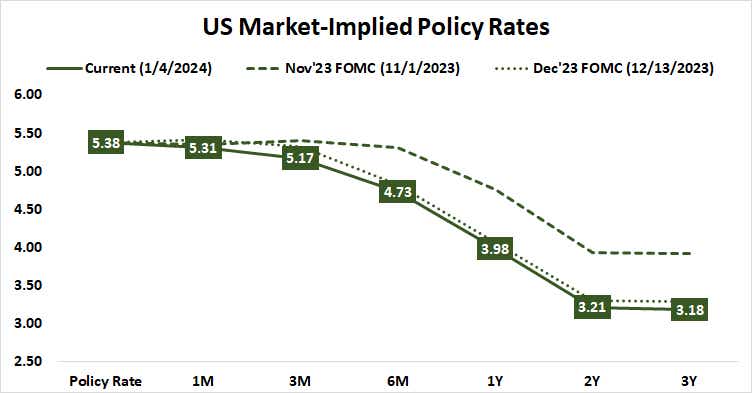

As it stands, the first of five 25-basis-point (bps) rate cuts is priced in to appear no later than May. The probability of a sixth reduction is now penciled in at 55%. This is a climbdown from where speculation peaked in late December, when all six cuts were fully baked into the markets and the likelihood of a seventh stood at 41%.

Faced with employment data arguing against a rapid business cycle swing one way or the other, the markets might reason that a further adjustment to a less hyperactive Fed makes sense. That threatens further follow-through on the week’s risk-off repositioning, hurting stocks and bonds in tandem while gold sinks and the U.S. dollar claws back territory.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices