Stock Markets Face Rude Awakening as PMI Data Flags Recession Risk and China Struggles to Grow

Stock Markets Face Rude Awakening as PMI Data Flags Recession Risk and China Struggles to Grow

By:Ilya Spivak

Global stock markets are roaring higher to end 2023 as the Fed’s embrace of interest rate cuts drives runaway gains. A rude awakening looms as PMI data warns of inescapable recession.

- PMI data will show China’s economy is still struggling a year after its post-COVID reopening.

- Taken together with a slow U.S. and shrinking Eurozone, recession seems inescapable.

- Gravity-defying stock markets face a rude awakening as Fed rate cut hopes are priced in.

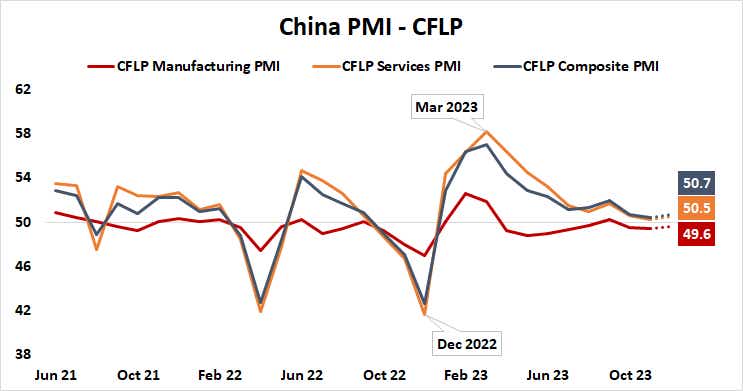

2023 will end with a whimper for China’s economy. The purchasing managers’ index (PMI) data due for release in the final hours of the year is expected to put the world’s second-largest growth engine at a near-standstill in December.

Activity in the manufacturing sector is seen shrinking for a third consecutive month, and the eighth in contraction mode this year. Tepid growth on the services side is seen pulling the overall economy forward, but at a snail’s pace. The fourth quarter is on pace for the weakest performance in a year.

Long COVID: China is struggling a year after reopening

That is an ominous sign because it was in December 2022 that collapsing growth and swelling public outrage finally pushed the authorities in Beijing to abandon restrictive “zero-COVID” policies and begin reopening the economy. It proved to be too little, too late as demand at home and abroad lagged behind pre-pandemic vigor.

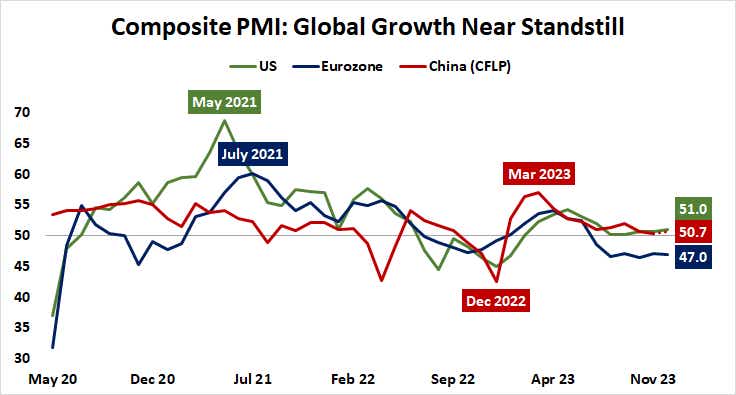

This is most unwelcome for a global economy struggling to find a way to avoid recession.

PMI readings from the United States and the Eurozone paint a bleak picture. As with China, U.S. growth has slowed to its weakest since the fourth quarter of 2022. Meanwhile, the single currency bloc was in contraction mode for a sixth month straight in December, shrinking at the fastest pace in three years.

Taken together, these three economies account for half of global output growth. That is before considering that the remaining half are mainly vendors servicing demand from the three behemoths, making them still more impactful on the worldwide business cycle. Skirting recession while they struggle seems all but impossible.

Stock market vs. global recession risk: no exit?

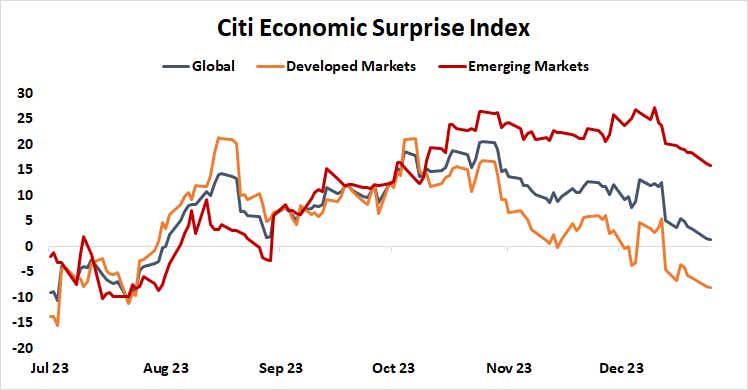

Analysts have taken notice. A Bloomberg survey of economists reveals that forecasts for global economic growth in 2024 and 2025 have drifted mercilessly lower for most of the year. Data from Citigroup warns that even this looks overly optimistic as economic outcomes fizzle relative to baseline forecasts.

This stands in stark contrast with booming stock market optimism. November and December have seen a blistering recovery, erasing three months of disappointment and pushing the Morgan Stanley Capital International (MSCI) World Stock Index (ACWI) toward a 12% gain for the year. Runaway strength in the U.S. is in the driver’s seat as Wall Street averages hit record highs.

In turn, that is being powered by an embrace of interest rate cuts at the Federal Reserve. Optimism seems fragile with six 25-basis-point (bps) interest rate cuts—plus a non-negligible 42% probability of a seventh—already priced into the markets for 2024.

This warns that trouble is brewing as the calendar prepares to turn to 2024. As hopes for Fed accommodation transition from speculation to a new central-bank-approved baseline discounted by the markets, weak growth and its inherent risks—especially for financial stability—seem likely to surface.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices