Macro Week Ahead: Federal Reserve Policy Meeting, U.S. and China Inflation Data

Macro Week Ahead: Federal Reserve Policy Meeting, U.S. and China Inflation Data

By:Ilya Spivak

Stock markets are at risk if recession fears return even as sticky inflation delays Federal Reserve interest rate cuts

- Another week of gains for technology stocks masks worries about slowing growth

- Global recession fears may build if Chinese inflation data undershoots expectations

- May U.S. CPI report, Fed monetary policy update in the spotlight for the markets

At first blush, Wall Street seemed to be in good spirits last week.

The bellwether S&P 500 stock index as well as the tech-leaning Nasdaq 100 scored strong gains, adding 1.1% and 2.4% respectively. For the former benchmark, it was the strongest performance in three weeks. For the latter, it was the biggest week of upside progress since mid-April.

Look elsewhere however, and the picture seems bleaker. The blue-chip Dow Jones Industrial Average traded nearly flat, adding just 0.17%. The small-cap Russell 2000 shed 2.24%, its biggest loss in seven weeks. As much was echoed at the sector level. Technology led the way higher, while losses were centered on energy, industrials, materials and utilities.

All this seems to hint that equity markets are beginning to consider a business cycle downturn. At the same time, a worrying sign emerged from the bond market: 10-year Treasury yields fell while the two-year rates held broadly steady. This is evocative of a “bull flattener” yield curve dynamic, which often appears in the runup to recession.

How might investors reconcile a slowing economy with a U.S. central bank that appears hamstrung by slow progress toward lower inflation?

Here are the macro waypoints that are likely to shape price action in the week ahead.

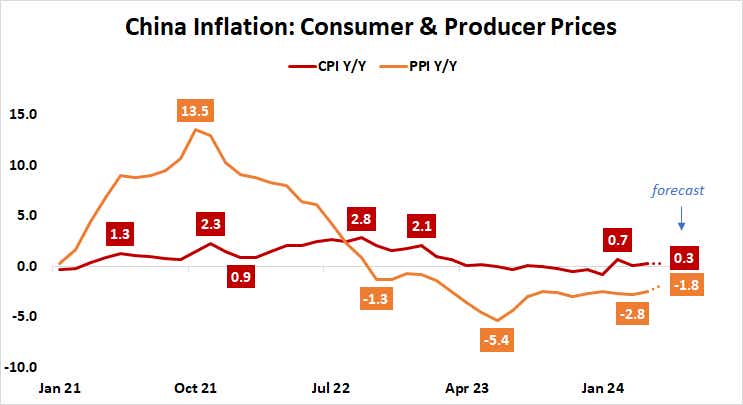

Chinese inflation data

China’s consumer price index (CPI) measure of inflation is expected to have risen 0.3% year-on-year in May, matching April’s outcome. The producer price index (PPI)–a measure of wholesale inflation—is expected to remain in negative territory at -1.8% year-over-year.

Analytics from Citigroup show that Chinese economic data outcomes have gradually deteriorated relative to baseline forecasts over the past two months. That might set the stage for disappointing outcomes that underscore anemic conditions in the world’s second-largest economy. Renewed global recession fears may follow.

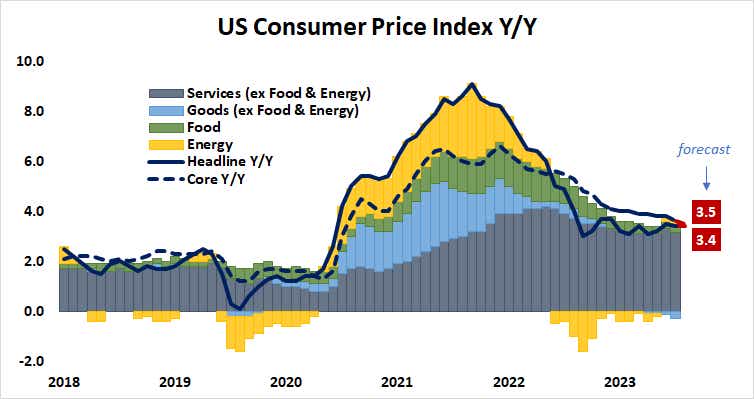

U.S. consumer price index (CPI) data

Core inflation in the U.S. is expected is expected to continue cooling in May, according to consensus forecasts. CPI excluding volatile food and energy prices—the version of the closely-watched inflation measure that is seen as most relevant for Federal Reserve officials–is set to inch down to 3.5% year-on-year.

That would mark the lowest reading in over three years. The headline measure is penciled in at 3.4% year-on-year, unchanged from April.

While the downtick at the core represents welcome progress, it seems unlikely to imbue central bank officials with the confidence needed to cut rates faster than is currently anticipated. In any case, traders will probably reserve judgement until the Fed issues its latest policy update mere hours after the data comes across the wires.

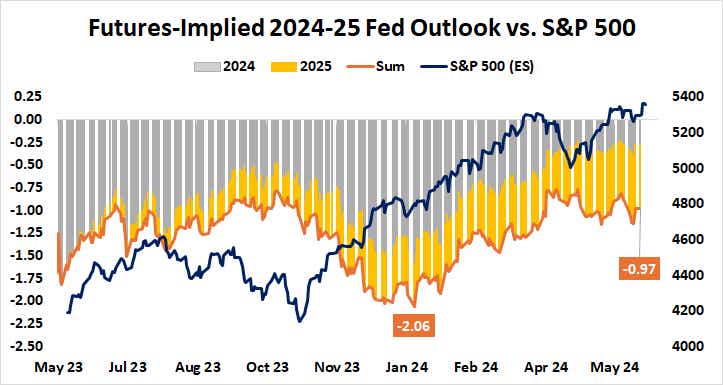

Federal Open Market Committee meeting

The Federal Reserve’s policy-steering group, the Federal Open Market Committee, is widely expected to keep the target range for the fed funds rate unchanged at 5.25-5.50%. The markets have priced in 28 basis points (bps) of stimulus this year, implying one standard-sized 25 bps reduction and a meager 12% probability of a second one. A move is expected in November or December.

With no rate changes on the menu this time around, traders are likely to focus on the updated Summary of Economic Projections (SEP) from central bank officials. Their March call for three cuts in 2024 will almost certainly get revised down to a setting closer to the markets’ 1-2 cut baseline.

How the view for 2025 is adjusted may be more interesting. As it stands, traders are anticipating 70bps in cuts next year. That is squarely in line with the Fed’s last update. They may be most interested to see if a “higher for longer” stance this year pushes additional cuts into next year’s tally. If not, a wave of disappointed de-risking might weigh on stocks.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices