Have the U.S. and China Cancelled Recession? No So Fast: Macro Week Ahead

Have the U.S. and China Cancelled Recession? No So Fast: Macro Week Ahead

By:Ilya Spivak

Markets applaud as the U.S. and China try to walk back the trade war, but recession risk remains

- Stock markets surge as the U.S. and China leap to de-escalate the trade war.

- Beyond exuberant headlines, consumers still face sharply higher tariff rates.

- All eyes now turn to U.S. inflation, retail sales, and consumer confidence data.

Stock markets stalled last week. The bellwether S&P 500 and the tech-tilted Nasdaq 100 tested the highest levels in nearly two months but failed to sustain momentum, closing down 0.5% and 0.3% respectively. Bonds continued to leak modestly lower, with two- and ten-year Treasury yields inching higher. The U.S. dollar followed suit.

This cautious calm was shattered at the start of this week amid would-be signs of rapid de-escalation of the U.S.-China trade war. A series of weekend meetings between Treasury Secretary Scott Bessent, Trade Representative Jamieson Greer, and a senior Chinese delegation produced what President Trump hailed as a “total reset” of trade relations.

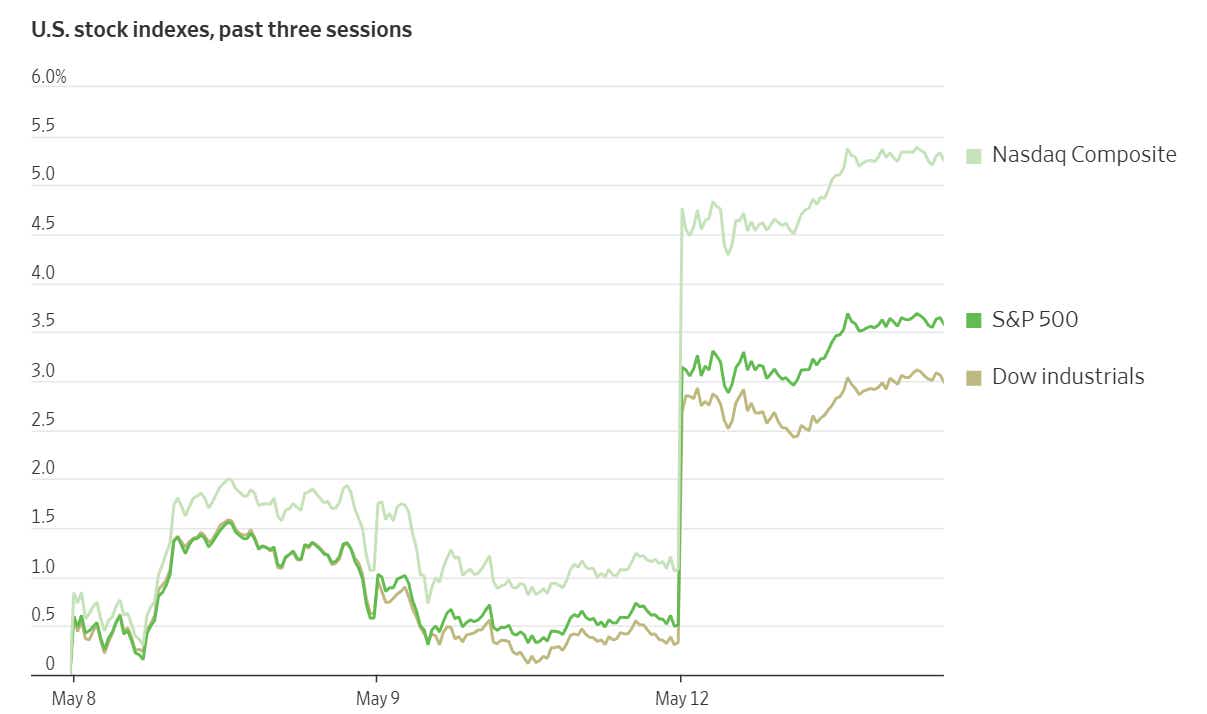

Stock markets surge as the U.S. and China wind back tariffs

The meatiest part of the outcome was a 90-day pause of reciprocal tariffs above 10% by both sides. A carve-out for the so-called “fentanyl” tariffs left them in place on the U.S. side, translating into a swing in the duty rate from 145% to 30%. On China’s side, levies came down from 125% to 10%.

The markets roared with approval. The S&P 500 is on pace for its best single-day performance since April 9, when President Trump issued the first 90-day reprieve from “Liberation Day” tariffs above 10% for countries excluding China. Treasury yields have moved higher across maturities, and the U.S. dollar is up close to 1% against the major currencies.

The key question now is whether this enthusiasm survives beyond traders’ initial exuberance. If the moderation with China sticks beyond the 90-day negotiation window and last week’s agreement with the U.K. are indicative, then there is indeed a 10% floor on U.S. tariff rates. That is a five-fold increase from an average of 2% before this year.

Are U.S. consumers ready to cancel the onset of recession?

This means that – in the best case scenario – consumers will still face sharply higher prices. While importers will probably rush to grow inventories for another quarter to front-run the possibility that the 90-day reprieve is not extended, it is less clear whether shoppers will absorb extra costs and keep buying as usual.

Indeed, tariff distortions aside, U.S. gross domestic product (GDP) data showed the slowest consumption growth slowed to the weakest in almost two years in the first quarter of this year. That part of the equation accounts for 68.5% of overall economic growth. If it remains soggy, the march toward recession is likely to continue.

With that in mind, incoming U.S. inflation, retail sales, and consumer confidence data will be closely watched. Optimism at the weekly open may struggle for follow-through if price growth dynamics reveal rising pressure on the goods side while weakening demand is a cooling agent on the services side, all as sales stall and sentiment darkens further.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit #tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices