U.S. Dollar Drops as Euro and Yen Gain in Trade War

U.S. Dollar Drops as Euro and Yen Gain in Trade War

By:Ilya Spivak

The trade war and the resulting uncertainty are taking a toll on the greenback

- The U.S. dollar is suffering steep losses as the global trade war heats up.

- The dollar’s ongoing loss of market share is likely to proceed, if not in a straight line.

- The euro and the Japanese yen will probably continue to outperform.

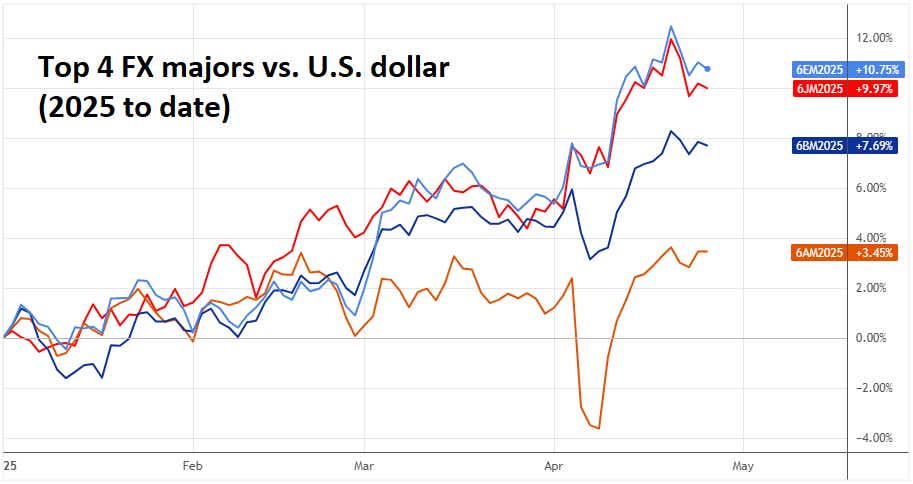

The U.S. dollar is attempting to stabilize after slumping to the lowest level in nearly seven months against an average of its major counterparts. Nevertheless, the greenback has lost nearly 10% of its value since the beginning of the year. This already puts 2025 on pace to be the worst year for the currency since 2017, and the second quarter has only begun.

Perhaps most critically, the dollar’s troubles mark a break from the trading patterns that have guided its performance for nearly 50 years. In April, it pointedly failed to find support from yield appeal as Treasury bond rates surged or from haven demand as the S&P 500 sank to 15-month lows.

Surging term premium—the cost of compensation for duration risk embedded in U.S. government debt—explains why the country’s stocks, bonds and currency have dropped in tandem. It speaks to acute concern about the U.S. fiscal trajectory. It’s a matter of rising sovereign risk after the rocky rollout of a new tariff regime by President Donald Trump.

U.S. dollar will probably keep falling

Flashes of moderation from the White House have helped anchor things a bit for now. Treasury Secretary Scott Bessent said a trade deal with China is inevitable because an embargo at both ends of the world’s most critical supply chain is untenable. In other welcome news, President Trump clarified that he will not try to fire Federal Reserve Chair Jerome Powell.

Nevertheless, the dollar’s troubles are probably not over, even if speculative forces help engineer a rebound in the near term. That’s because the undoing of global trade norms—a goal loudly championed by the Trump administration—will almost certainly reduce cross-border commerce and leave foreigners holding fewer greenbacks.

Growing trade incentivized countries exporting into the world’s largest consumer market to recycle dollar-denominated profits back into U.S. financial markets. That kept the dollar strong and fortified its purchasing power of foreign goods, underpinning demand for imports. With current trends, these inflows may become a trickle.

The euro and the yen seem primed to capture market share

The euro and the Japanese yen have stood apart as the main beneficiaries of dollar weakness so far this year. This seems to make sense: The two currencies occupy the distant second and third place after the dollar in terms of their share of global monetary transactions, according to the Bank of International Settlements (BIS).

_-_2022.png?format=pjpg&auto=webp&quality=50&width=900&disable=upscale)

This relatively deep liquidity is likely to keep the two currencies at the forefront as the dollar loses market share. It will almost certainty retain the top spot on the league tables, thanks to the peerless depth of U.S. financial markets—but with a narrower lead against its rivals.

Friendly central banks may help. The markets are flirting with the possibility of interest rate hikes from the European Central Bank (ECB) next year as a blistering buildout of defense capacity spurs growth and inflation. The Bank of Japan (BOJ) is alone among its peers in hiking rates this year, and markets expect it to continue in 2026.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices