U.S. Dollar Decouples from Treasuries for a Simple Reason

U.S. Dollar Decouples from Treasuries for a Simple Reason

The Dollar Index (DXY) is up +0.44% month-to-date

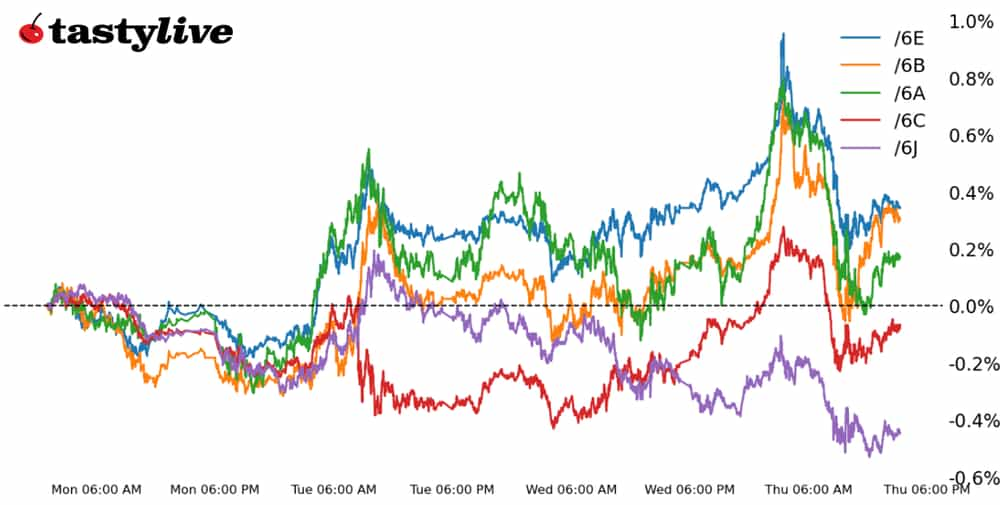

- U.S. Treasury yields are holding near their yearly highs, but the U.S. dollar has traded mostly lower this week.

- While Fed rate-cut odds have undergone a significant shift since the start of the month, other central banks are now just seeing their cut odds pushed back, helping catalyze other major currencies’ strength.

- Near-term U.S. dollar weakness may be worth fading longer-term.

Fed rate-cut odds for March and May are at their lowest levels of the year, helping push up U.S. Treasury yields to multi-month highs in recent days.

But the U.S. dollar is trading mostly lower this week, seemingly detached from a key fundamental driver. There is a reasonable basis for this divergence that may soon be resolved.

Since Jan. 31 Federal Open Market Committee (FOMC) meeting, Fed rate-cut odds have been on a steady trek lower. From Jan. 31 until the middle of February, the retreat in Fed cut odds was a singular effort. Rate-cut odds for the Bank of England, European Central Bank, Reserve Bank of Australia, etc. were little changed.

Investors reevaluate the odds

Starting on Feb. 14, traders began to reconsider their views on the timing of rate-cut cycles for all the other major central banks. Like with the Federal Reserve, traders began to speculate that rate-cut cycles would begin later in the year; declining cut odds from the BOE, ECB, RBA, etc. helped fuel a sell-off in overseas bond markets in what was effectively a ‘catchup trade’ to the move seen in U.S. Treasuries in the first half of February.

Given the economic trajectories of other major economies—Japan and the U.K. in technical recessions and the Eurozone not far behind—it still makes sense that the rest of the world will "out dove" the Fed for most of 2024. The short-term convergence between Fed and non-Fed rate cycle expectations has proved unfavorable for the U.S. dollar, but that catalyst may soon be exhausted.

Any additional weakness by the U.S. dollar may be setting up a "buy the dip" opportunity against a host of major currencies shortly.

/6B British pound technical analysis: daily chart (August 2023 to February 2024)

The British pound (/6BH4) has maintained a sideways consolidation that has been in place since mid-December 2023, ranging mostly between 1.2509 and 1.2833.

There’s little reason to think that the current range will break anytime soon, especially considering that /6BH4 finds itself directly situated between support and resistance. Range trading strategies like short strangles and iron condors remain appropriate, although given the lack of volatility (IV index: 6%; IV rank: 2.7), it’s understandable if traders look elsewhere.

/6E Euro technical analysis: daily chart (July 2023 to February 2024)

The euro (/6EH4) staged a modest rally off the swing lows established in early-November 2023, just north of 1.0700. In turn, it has also reclaimed the uptrend from the October and November 2023 swing lows, which initially provided support at the lows carved out at the start of February.

Does the turn higher constitute a bullish breaking from a falling wedge? It’s possible, and that would suggest that there remains significant space overhead for further gains in the short term. Any additional upside from here would be sought to be faded (perhaps via an ATM put spread).

\/6J Japanese yen technical analysis: daily chart (September 2023 to February 2024)

The Japanese yen (/6JH4) has been perhaps the most frustrating major currency in 2024, though hindsight offers clarity.

The Bank of Japan never delivered on hints that it would alter its policy stance while global bond yields ratcheted higher. While USD/JPY spot rates are hovering below the 2023 lows, /6JH4 has already breached the November 2023 low and has staged a feeble bounce off the lows established Feb. 13, the day the January U.S. inflation report was issued.

With /6JH4 continuing to track its daily five-day exponential moving average (one-week moving average) to the downside–it hasn’t closed above it since Feb. 1–it’s difficult to suggest that the currency has established a tradeable low.

Christopher Vecchio, CFA, tastylive’s head of futures and forex, has been trading for nearly 20 years. He has consulted with multinational firms on FX hedging and lectured at Duke Law School on FX derivatives. Vecchio searches for high-convexity opportunities at the crossroads of macroeconomics and global politics. He hosts Futures Power Hour Monday-Friday and Let Me Explain on Tuesdays, and co-hosts Overtime, Monday-Thursday. @cvecchiofx

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices