Euro May Rise as EU Defense Splurge Offsets Tariffs: ECB Preview

Euro May Rise as EU Defense Splurge Offsets Tariffs: ECB Preview

By:Ilya Spivak

The euro may rise even as the ECB cuts rates again if an EU defense spending binge beckons a hawkish tone

- The ECB is widely expected to cut interest rates again, hitting a 2% target rate.

- Markets are priced for a mildly dovish bias in ECB guidance amid tariff worries.

- The euro may rally if EU defense spending plans bring on a hawkish tone shift.

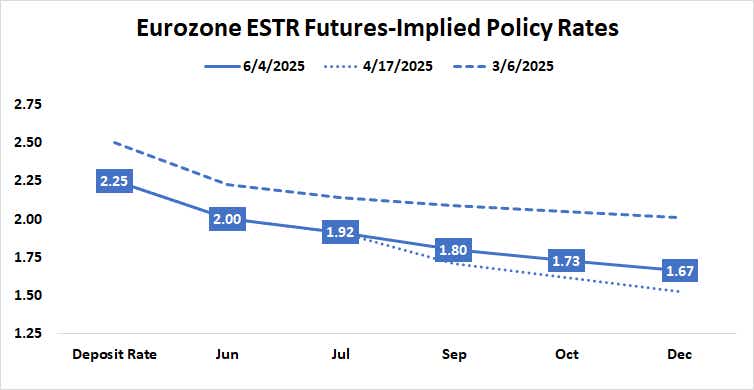

The European Central Bank (ECB) is expected to cut its target interest rate again this week. A reduction of 25 basis points (bps) in the benchmark deposit rate from 2.25% to 2% has been fully priced in by the markets, according to benchmark ESTR rate futures. For traders, this puts the spotlight on what the central bank is likely to do next.

As it stands, the markets are envisioning 34bps in further cuts this year, beyond this week’s adjustment. This comes to 25bps in additional easing along with a 36% probability of a third cut. Rates are expected to remain on hold next year. A modest tightening bias is reflected in markets are pricing in a 5bps uplift, which implies a 20% probability of a hike.

An ECB rate cut is coming, but what will happen next?

ECB watchers will have plenty to chew on as they consider whether this outlook still makes sense. Beyond the usual release of a policy statement from the Governing Council and a press conference with President Christine Lagarde, the central bank will issue the quarterly update of its economic forecasts.

Conflicting forces are at play. On the economic growth front, the currency bloc seems to be in dire straits. Purchasing managers index (PMI) data from S&P Global revealed that the manufacturing and services sectors both contracted in May. For the latter, this was the first decline since November. Taken together, this left the economy at a standstill.

Against this backdrop, inflation has fallen back to the ECB target. Preliminary figures for the consumer price index (CPI) said it grew 1.9% year-on-year in May, the lowest since a brief spike down to 1.7% in September. A rebound in energy’s contribution to overall price growth then pushed inflation up to 2.5% by January.

The euro may rise as the ECB eyes EU defense spending

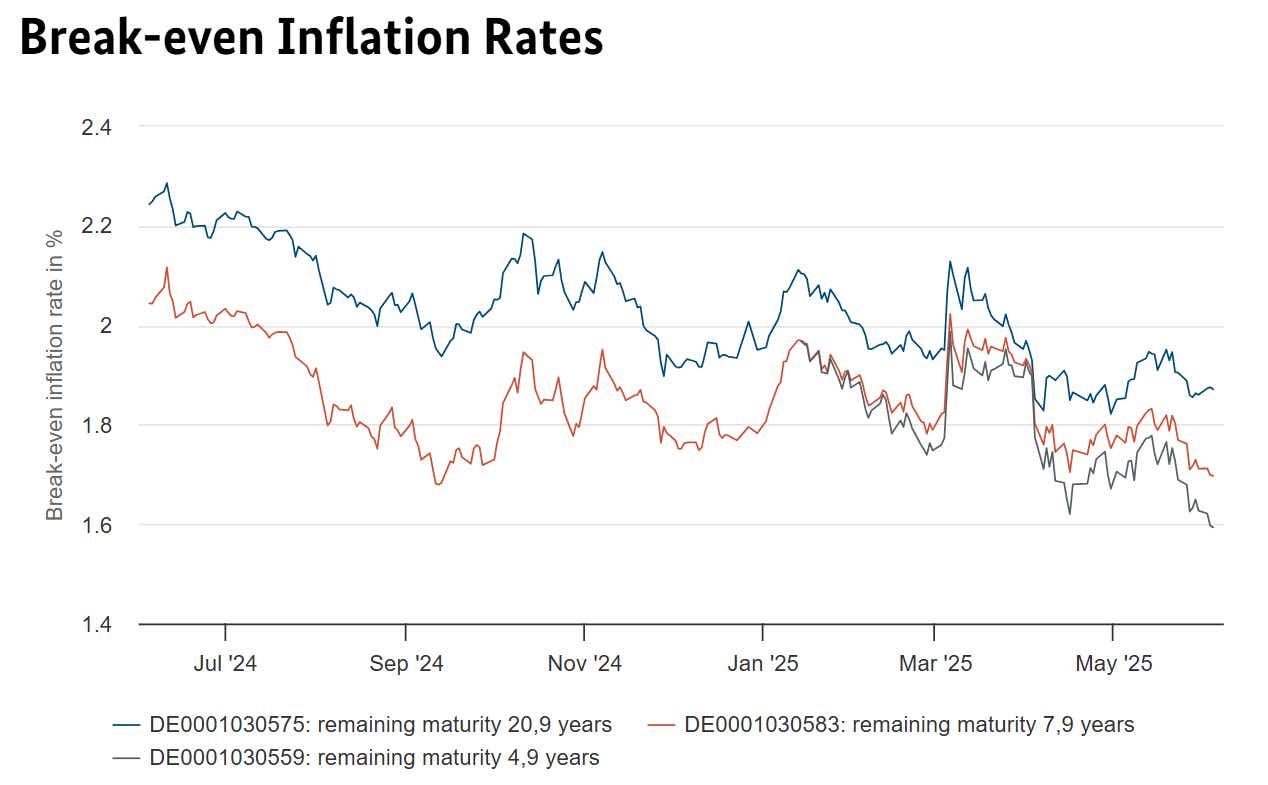

The markets seem to envision that weakness will persist from here. Inflation expectations priced into German bonds have been falling since recently, with the benchmark 5-year rate sinking to levels unseen in over a year a well below the ECB target. This points to expectations for weak demand ahead.

It seems to make sense that this could foreshadow downward revisions in ECB growth and inflation forecasts. The March edition did not the majority of the US tariff shock that has since emerged. The Eurozone is a net exporter to the US, so the central bank may conclude that higher trade barriers will amount to a greater headwind than expected.

However, the slide in breakevens suggests the markets might have already priced in as much. On the other hand, the vast European Union rearmament plan envisioning 800 billion euro in additional defense spending represents an upside shock to both growth and inflation. Its first 150 billion euros were just approved by the European Council last week.

If the ECB takes a more hawkish stance with this in mind. That need not be dramatic, since the markets already expect tariff-related issues front and center. If baseline forecasts reflect countervailing concerns about reflation risk as growth gets a shot in the arm from fiscal largesse next year, the euro may get the green light for a rally.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts #Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit #tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices