Fed, BOE and BOJ Outcomes Threaten Stock Markets: Macro Week Ahead

Fed, BOE and BOJ Outcomes Threaten Stock Markets: Macro Week Ahead

By:Ilya Spivak

Stocks face deeper losses, and the yen may rise as central banks in the U.S., U.K. and Japan issue policy updates

- The Fed is widely expected to keep policy unchanged, with a focus on updated forecasts.

- The Bank of England may follow the ECB lead with a “dovish hike”, hurting the pound.

- The Japanese yen may rise even as the Bank of Japan resists “sea change” speculation.

Last week, the European Central Bank (ECB) joined a growing cohort of top monetary authorities signaling the approaching end of a blistering global rate hike cycle, as expected. The Reserve Bank of Australia (RBA) and the Bank of Canada (BOC) have offered similar guidance as a worldwide recession takes shape on the horizon.

More of the same may be ahead as three more powerhouse central banks offer up policy updates in the week ahead.

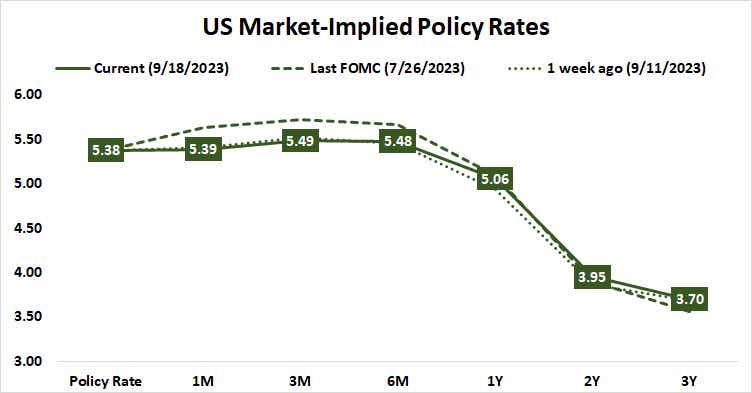

The Federal Reserve policy meeting

Fed Chair Jerome Powell and company are overwhelmingly expected to keep policy rates unchanged at September’s meeting of the rate-setting Federal Open Market Committee (FOMC) committee. The priced-in probability of a 25-basis-point (bps) increase is a mere 0.8%. The cumulative likelihood of such an increase peaks in December at 47%.

Rate cuts are on the menu thereafter in the second half of 2024. The first 25 bps reduction is penciled in with a 61% probability in June. It is fully priced in by July. Three cuts over the subsequent half-year are already in the market, with an 8% probability of a fourth one before the calendar turns to 2025.

Guidance to fine-tune this latter part of the outlook is probably the most market-moving aspect of the incoming announcement. The Fed will publish an updated set of forecasts for key economic indicators including growth and unemployment as well as policymakers’ own interest rate projections.

The balance of risks for adjusting the rates outlook seems adversely tilted to stocks and similar-minded assets. An upshift signaling a “higher for longer” stance might spook investors worried about the gathering threat of global recession. A downshift may be read as a sign of endorsing those very fears. The “risk-on” space in between seems narrow.

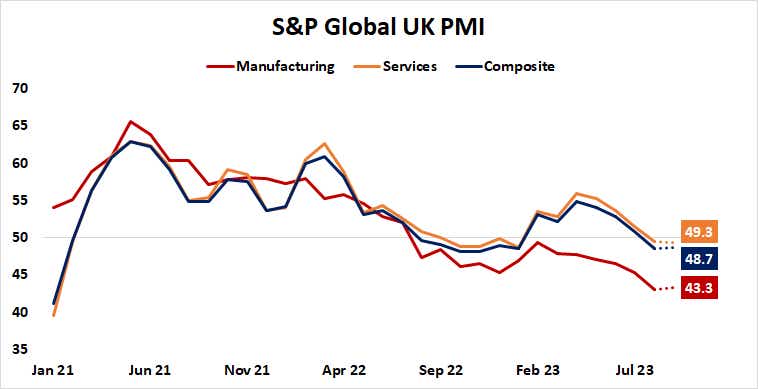

Bank of England (BOE) interest rate decision

Market pricing reflects an 80% probability of another BOE rate hike at this week’s policy meeting. The move is fully baked in by November. What happens thereafter seems to be a toss-up. The likelihood of another increase to follow peaks at 49% in February 2024, then fades. No rate cuts are seen on the menu at least through August.

The U.K. central bank finds itself in much the same situation as the European Central Bank (ECB). Here too, food prices are the largest remaining contributor to inflation as the impact of last year’s energy price spike filters out. Meanwhile, Purchasing Managers Index (PMI) data suggests the economy is shrinking.

On balance, this sets the stage for a “dovish hike”, where officials accompany another 25bps uptick with guidance hinting that the cycle is probably over. The ECB offered up as much last week and sank the euro. The British pound saw some sympathy weakness with that move. It could face still more pain as the BOE follows suit.

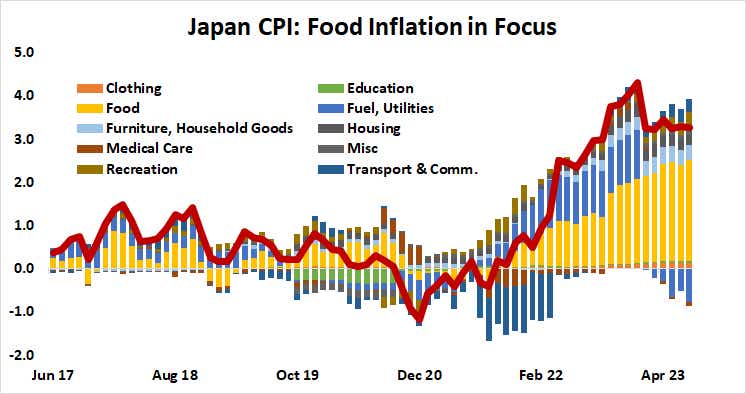

Bank of Japan (BOJ) monetary policy meeting

Despite rabid speculation about an imminent policy “sea change,” the calculus at the BOJ is hardly altered. Traders made much of a comment from Kazuo Ueda, BOJ's governor, suggesting that the central bank’s ongoing policy review may yield enough data to make some big decisions by year-end. The direction of travel for such changes is being assumed as hawkish.

Markets are bracing for the end of yield curve control (YCC)—a policy capping 10-year Japanese government bond (JGB) yields—as a precursor to lifting the policy interest rate out of negative territory. BOJ sources have tried to water down such bet-making since Ueda spoke, pushing investors to a more balanced stance.

As it happens, the BOJ faces a comparable situation to that of the ECB and BOE. Food inflation is the banner issue, and like its European counterparts, there isn’t much the central bank can do here by fiddling with monetary levers.

A gauge of global food prices from the United Nations (UN) suggests they fell to a 28-month low in August after peaking last year. It tends to lead price growth trends by about seven months. So, some progress is already on display, and more is signaled ahead. This might allow the BOJ to bide its time for now.

How the Japanese yen reacts if Ueda and his colleagues opt for stasis may be telling. The end of the global tightening cycle outside Japan seems to be drawing closer and looks likely to boost the perennially low-yielding currency as rate differentials stop expanding against it. If this allows for gains without BOJ action, follow-through seems likely.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices