Stocks at Risk on PMI Data, NVDA Guidance, Hawkish Fed: Macro Week Ahead

Stocks at Risk on PMI Data, NVDA Guidance, Hawkish Fed: Macro Week Ahead

By:Ilya Spivak

Stock market turmoil may continue with PMI data, NVDA earnings and the Fed’s Jackson Hole Symposium in focus

- U.S. stocks down again as U.S. dollar gains, while investors eye “higher for longer” Fed rates outlook.

- Telltale Japanese yen rebound signals global recession fears may be gathering steam.

- PMI surveys, NVDA earnings, Powell speech at Jackson Hole Symposium now in focus.

Sellers held sway again last week on Wall Street. The benchmark S&P 500 stock index fell 2.2%, hitting a two-month low. The U.S. dollar marched higher for a fifth consecutive week while gold prices slid a third one and the yield curve steepened, with borrowing costs higher across maturities.

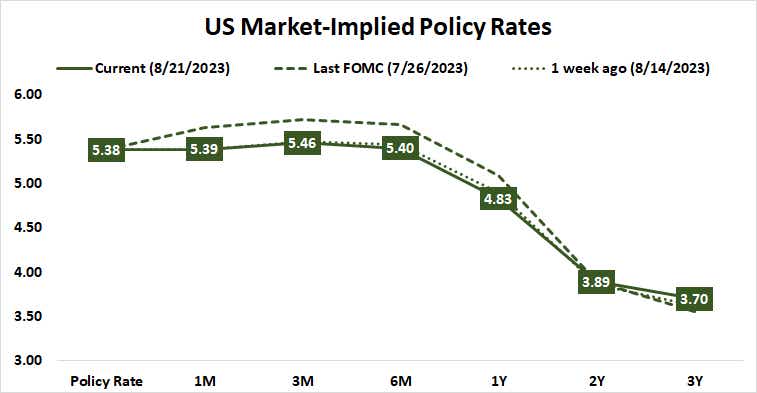

Scanning the headlines, all this seems to have been chalked up to speculation about a “higher for longer” repricing of Federal Reserve interest rate expectations. Some of this is almost certainly afoot, but the adjustment has been modest at best.

Futures markets now price in a Fed Funds rate of 4.33% at the end of next year, up from 4.0% flagged three weeks ago when the risk-off sweep began. That speaks to a slightly reduced scope for easing in 2024, to the tune of about one standard sized 25-basis-point (bps) rate cut. The probability for another hike this year has not meaningfully changed. The rate expected by the end of 2023 has limped upward from 5.38% to 5.43%, a meager five bps.

There seems to be more to the story. A telltale rise in the Japanese yen toward the end of last week—a move that left the dollar well-supported while bonds held back from breaking below trend-defining price levels—suggests markets are beginning to worry about more than just a longer-lasting headwind from a hawkish U.S. central bank.

With China struggling to reboot its economy after scrapping COVID-era lockdowns and the Eurozone dipping into recession, the worry seems to be that Fed hawks will kick out the last bit of support upholding global growth and trigger a broad-based slump.

Here are the key macro waypoints shaping the story in the week ahead:

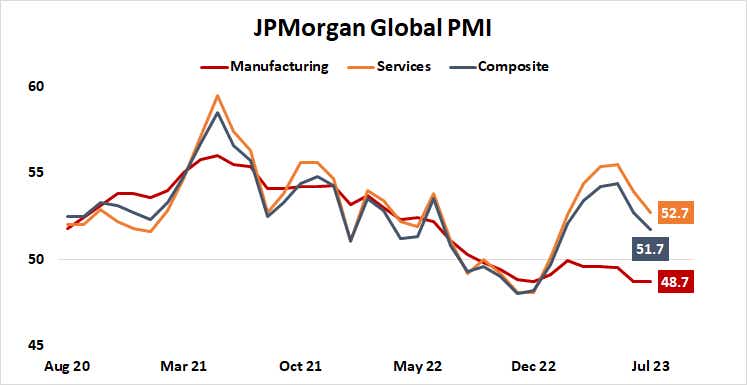

PMI surveys

A slew of Purchasing Managers' Index (PMI) surveys—a timelier approximation of economic growth trends than gross domestic product (GDP) numbers, which tend to be released with significant time lags— seems set to show the global economy continued to slow in August.

Eurozone manufacturing- and service-sector activity is expected contract for a third month straight while growth in the U.S. slows to the weakest since February. Numbers tracking Australia, Japan, and the U.K. are also due. Soft results may amplify global recession fears, hurting stocks and underpinning bonds while the U.S. dollar and Japanese yen outperform against other major currencies.

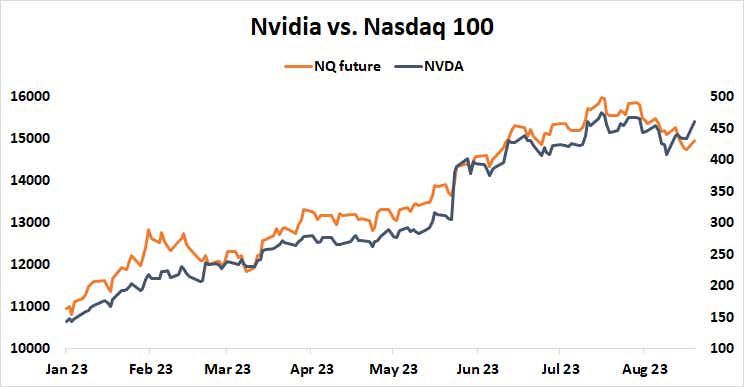

Nvidia (NVDA) Q2 earnings report

The darling of the artificial intelligence (AI) frenzy in the global tech sector smashed forecasts when it reported first-quarter results, helping to kick off a blistering rise in the technology-heavy Nasdaq 100 stock index.

A strong showing is expected, but markets will be paying close attention to the guidance on offer alongside results, particularly vis-à-vis the firm’s sensitivity to China. Worries about mounting uncertainty and tepid demand as the world’s second largest economy attempts to regain momentum might sour sentiment, adding to the impetus for liquidation across equity markets.

Jackson Hole Economic Symposium

The annual gathering of Federal Reserve officials and other monetary policy and macroeconomics bigwigs in Wyoming will begin on Thursday, but all eyes are on the speech from Jerome Powell, Fed chair, on Friday.

U.S. central bank leaders often use the gathering as an opportunity to paint a broad-based picture of where they intend to steer in the 12 months ahead. This establishes the lens through which financial markets ought to be interpreting incoming information and applying it to policy expectations. Rhetoric signaling a willingness to stay in the fight against inflation even at the cost of enduring a recession may bolster the possibility of another rate hike in 2023 and reduce the projected scope for easing in 2024, cooling risk appetite across the asset spectrum.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices