When Will Stocks Notice Warning Signs Blinking in Bond Markets?

When Will Stocks Notice Warning Signs Blinking in Bond Markets?

By:Ilya Spivak

When will the markets start to care about risks to global economic growth?

- Fed Chair Powell sticks to a familiar script in first day of Congressional testimony.

- The markets still see a more dovish path, hinting at lingering global growth fears.

- Soggy US data flow warns recession fears may return, and bonds have noticed.

Federal Reserve Chair Jerome Powell struck a familiar tone in the first day of semi-annual testimony before the U.S. Congress. The central bank chair appeared in the House of Representatives today and is slated for a repeat performance in the Senate tomorrow.

In his prepared remarks, Powell repeated the now-familiar refrain that the Fed is well-positioned to wait and see how the tariff regime rushed out by the White House will impact the path for growth and inflation before acting on interest rates. He added that the base case remains that the duties are likely to lift inflation and hurt economic activity.

In the Q&A session that followed, Powell reiterated that “a significant majority of policymakers think it will be appropriate to reduce rates later this year.” However, he also warned that the reason rates are not coming down now is that consensus forecasts expect a “meaningful increase in inflation this year.”

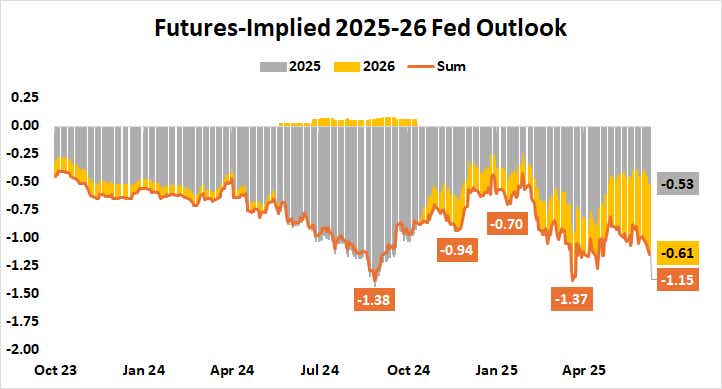

The markets and the Fed remain at odds after Chair Powell testimony

Last week, the Fed’s policy-steering Federal Open Market Committee (FOMC) kept its interest rate target unchanged, matching widely held expectations. Officials revised down their expectations for economic growth while marking higher the outlook for inflation, as anticipated.

On the path of interest rates, the FOMC kept its call for 50 basis points (bps) in rate cuts in 2025. Next year’s median forecast rate was raised from 3.4% to 3.6%, implying a downgrade from two standard-sized 25bps cuts to just one. This may reflect the idea that President Trump’s twin 90-day pauses of full tariff implementation will delay their impact.

It also marks a widening departure from what the markets have priced in. Benchmark Fed Funds futures are now pricing 54bps in interest rate cuts this year and 61bps in 2026. This means that traders are aligned with the Fed for the immediate term but see a far more dovish trajectory thereafter.

The bond market echoes investors’ thinking. Prevailing inflation expectations baked into Treasury pricing – so-called “breakeven rates” – have trended pointedly lower since mid-May. That suggests the markets are more worried about a disinflationary economic downturn than a sticky price shock from the tariffs.

Will global growth concerns return after the markets cheer US-Iran ceasefire?

For now, markets seem happy to celebrate after the Mr. Trump announced a ceasefire between the US, Israel and Iran. This comes after the US struck Iranian nuclear targets over the weekend, followed mutual efforts to de-escalate. Israel launched a surprise attack on Iran last week.

In the meantime, data from Citigroup warn that US economic data outcomes have increasingly disappointed relative to consensus forecasts over the past month. Purchasing managers index (PMI) data from S&P Global showed this week that the US remains the lone pillar of global growth, while the Eurozone and China idle.

This makes for a single point of failure for worldwide economic growth, along with some preliminary evidence suggesting it is under pressure. That comes at a time when the Fed sounds resistant to act, despite market pressure to the contrary. When asset prices decide to notice the risks therein – as bond markets seemingly have – remains unclear.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts #Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit #tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices