Stocks May Turn Lower If Consumers Turn Gloomy as Tariff Inflation Surfaces

Stocks May Turn Lower If Consumers Turn Gloomy as Tariff Inflation Surfaces

By:Ilya Spivak

Will stock markets sour on economic growth trends if US consumer confidence gives way?

- US retail sales data topped forecasts, but the second-quarter trend looks dour.

- Financial markets tellingly added to 2026 Fed interest rate cut expectations.

- Consumer confidence data is now in focus for a view into growth dynamics.

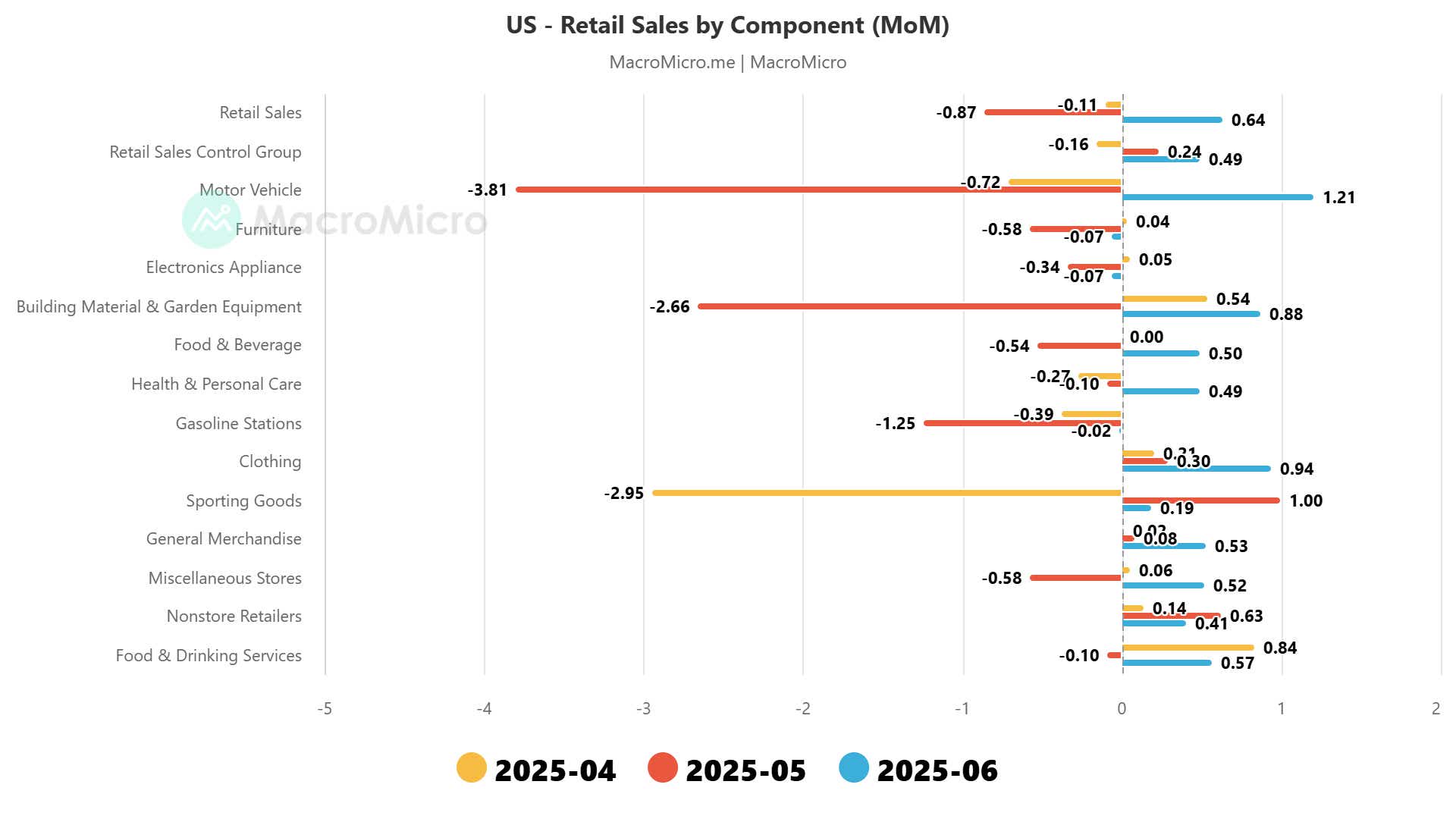

Wall Street cheered after US retail sales data showed receipts rose more than economists expected. The US Census Bureau (USCB) reported that sales posted a monthly rise of 0.6% in June, topping median forecasts calling for a meager increase of just 0.1%. Year-on-year growth sped up to 3.9%, posting the first increase in three months.

Rebounding motor vehicle sales drove the rosy outcome, rising 1.21% from the previous month. However, this follows steep declines in April and May, which recorded losses of 0.72% and 3.81%, respectively. Vehicles make an outsized contribution to overall retail sales, accounting for about 20%-22% of the total.

US retail sales report: less than meets the eye

This looks less encouraging than the headline numbers would suggest. While June’s recovery flatters monthly results, sharp losses in the previous two months leave vehicle sales net down close to 3.3% over the period. Put simply, last month’s rise moderates the degree to which sales retrenched in the quarter, but it does not alter the dour trend.

That seems ominous. Consumption is by far the biggest driver of US economic growth, accounting for close to 68% of overall gross domestic product (GDP). Tariff-induced anomalies in imports and inventories aside, first-quarter data saw the weakest contribution since the second quarter of 2020. The second quarter now looks likely to be soggy, too.

That may explain what happened with Federal Reserve monetary policy expectations following the retail sales report. Fed Funds futures show scope for rate cuts this year was modestly hemmed in, with traders discounting just 38 basis points (bps). The view for 2026 turned more dovish however, calling for 73bps in easing.

Taken together, this amounts to 110bps in stimulus between now and the end of next year, against the US central bank’s latest forecast – issued in June – pointing to just 75bps. The disparity is most acute in 2026, where the Fed sees just one standard-sized 25bps reduction, while the markets have all but fully priced in three of them.

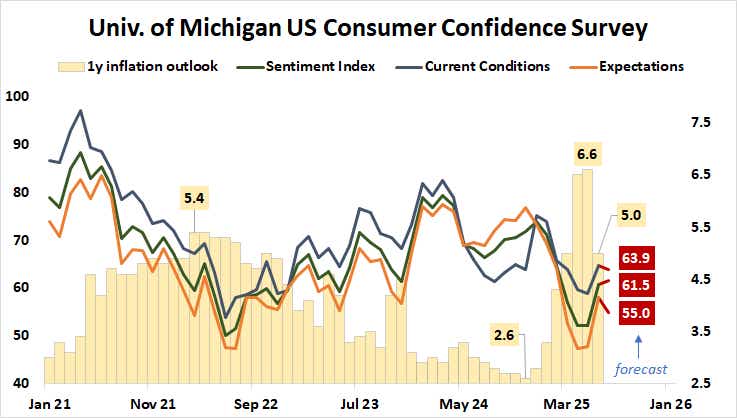

US consumer confidence data: will it spook the markets?

The spotlight now turns to a closely watched survey of US consumer confidence from the University of Michigan (UofM). It is expected to show that sentiment improved a bit this month after a potent jump in June against the backdrop of easing inflation expectations. Respondents’ one-year outlook moderated to 5% from 6.6% in the May edition.

US inflation data published earlier this week showed consumers began to see price growth linked to tariff increases rolled out by the Trump administration. A separate report showed wholesalers at the front end of the supply chain continue to absorb higher input costs into margins, suggesting that underlying price pressures may be mounting.

If this translates into a move upward on inflation expectations in July’s UofM report, the headline sentiment reading may disappoint. That would amount to a gloomy start for where consumption trends are heading in the second half of the year, amplifying concern about growth already on display in first-half price action.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts #Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit #tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices