Filter

Contents

What is a Vertical Debit Spread & How to Trade it?

Contents

What is a Vertical Debit Spread?

A vertical debit spread is an options trading strategy that involves buying and selling two options of the same type (either calls or puts) with the same expiration date but different strike prices. The option that is purchased is worth more than the option that is sold, which is how the trade is a debit transaction. This strategy allows traders to express a directional or volatility view on an underlying asset while controlling potential risks and rewards. The key appeal of vertical spreads is their defined risk, meaning traders know upfront both the maximum amount they can make and the maximum amount they can lose. Vertical spreads can be tailored to fit a variety of market conditions outlooks.

There are two main types of vertical spreads: debit vertical spreads and credit vertical spreads. In a debit vertical spread, the trader pays a net premium to enter the position, typically because the long option (the one purchased) costs more than the short option (the one sold). The profit potential is capped, but so is the loss, which is limited to the amount paid for the spread. Max profit on a debit spread is realized when both options expire in-the-money (ITM). Max loss is realized when both options expire out-of-the-money (OTM).

In comparison, with a credit vertical spread, the trader receives a net premium by selling an option with a higher premium than the one that is purchased. While the profit is capped at the premium received, the potential loss is also defined, calculated by the difference between the strike prices minus the premium received. Max profit on a vertical credit spread is realized when both options expire OTM. Max loss is realized when both options expire ITM. The exact inverse of a vertical debit spread.

Each type of vertical spread offers a different risk-reward profile, with debit spreads generally benefiting from moderate price movements, and credit spreads thriving when the underlying trades in range-bound fashion.

How do Vertical Debit Spreads Work?

Vertical debit spreads are typically employed by options traders who anticipate a moderate price movement in the underlying asset. This strategy involves buying one option and selling another of the same type (call or put) and expiration date, but with different strike prices. By doing so, traders can potentially profit from the asset's price movement.

The trade is structured such that the trader buys a more expensive option (the long option) and sells a less expensive option (the short option) - the latter option helps to offset the cost of the combined position. If the underlying asset moves as expected, the long option gains value while the short option loses value, producing a net profit. Generally speaking, the maximum loss is limited to the premium paid for the spread, and the maximum profit is capped by the difference between the two strike prices, minus the net debit paid, assuming both options expire ITM.

Vertical Debit Spread Basics

The construction of a vertical debit spread involves either a call or a put spread, each with its own specific risk-reward profile.

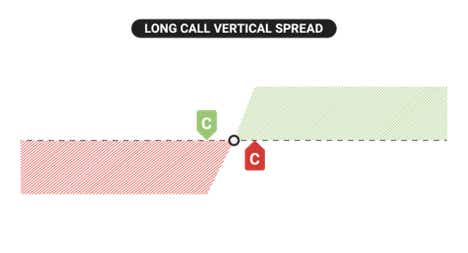

In a call vertical debit spread, the trader buys an in-the-money (ITM) call option and sells an out-of-the-money (OTM) call option. This strategy is typically employed when the trader expects the price of the underlying asset to rise, but moderately. The maximum gain is limited by the distance between the two strike prices. In a put vertical debit spread, the trader buys an ITM put option and sells an OTM put option. This strategy is generally used when the trader expects the price of the underlying asset to decline.

For both strategies, the risk is defined upfront - the maximum loss is the net premium paid to enter the spread, while the maximum gain is capped by the difference in the strike prices minus the total debit. In short, if the underlying fails to move in the desired direction, the trader may lose the capital outlaid to enter the position. The key to a successful vertical debit spread therefore lies in selecting the appropriate strike prices and expiration date, such that they align closely with the trader’s expectations for price movement and volatility.

Additionally, implied volatility can play a role in the outcome of a vertical debit spread. For instance, if implied volatility rises, it can increase the value of the long option. As a result, an uptick in volatility can boost the value of the spread, enhancing its potential for profit. Therefore, when setting up a vertical debit spread, it’s also important to consider the volatility environment, because prevailing volatility conditions can add an extra layer of complexity to the trade.

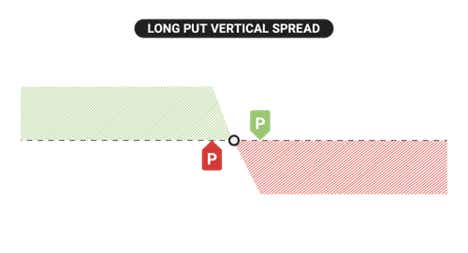

What is a Vertical Put Debit Spread?

A vertical put debit spread is an options strategy where a trader buys an in-the-money (ITM) put option and sells an out-of-the-money (OTM) put option, both with the same expiration date. This strategy is typically used when the trader expects the price of the underlying asset to decline, but moderately. The long put (the one bought) allows the trader to profit from a falling price, while the short put (the one sold) reduces the overall cost of the position by providing some offsetting premium received.

Once again, implied volatility can enhance the performance of the spread—if volatility rises, it can increase the value of the long put option, providing a net benefit to the trader. The maximum risk for a vertical put spread is the net premium paid for the spread, while the maximum gain is capped by the difference between the strike prices minus the debit paid. Vertical put debit spreads are generally used when a trader wants to limit both risk and costs while expressing a bearish outlook on the underlying asset.

Vertical Call Debit Spread Example

Imagine XYZ stock is currently trading at $100 per share, and a trader is moderately bullish on the stock. The trader expects XYZ to rise to around $105 per share by the options expiration date, but not significantly higher. To capitalize on this move while limiting risk, the trader could deploy a vertical debit call spread.

This strategy involves buying a call option with a lower strike price and selling a call option with a higher strike price, both within the same expiration cycle. By doing so, the trader can benefit from a moderate upward move in the stock while controlling the cost and risk of the trade.

Trade Setup

- Buy a $95 strike call (in-the-money, ITM) for $6.00

- Sell a $105 strike call (out-of-the-money, OTM) for $3.00

- Net Debit: $6.00 (buying the $95 call) - $3.00 (selling the $105 call) = $3.00

Potential Outcomes

- Maximum Loss: The maximum loss is the net debit paid to enter the trade, which is $3.00. This occurs if XYZ stock is at or below $95 at expiration, and both calls expire worthless.

- Maximum Gain: The maximum gain is the difference between the strike prices minus the net debit paid. In this case, the difference between the strikes is $10 ($105 - $95). Subtract the $3.00 paid for the spread, and the maximum gain is $7.00. This occurs if XYZ stock is at or above $105 at expiration.

- Breakeven: The breakeven price at expiration is the lower strike price ($95) plus the net debit paid ($3.00). Therefore, the breakeven is $98 ($95 + $3).

Vertical Put Debit Spread Example

Imagine stock ABC is currently trading at $80 per share, and a trader is moderately bearish on the stock. The trader expects ABC to fall to around $70 per share by the options expiration date, but not significantly lower. To capitalize on this move, the trader could deploy a vertical debit put spread. This strategy involves buying a put option with a higher strike price and selling a put option with a lower strike price, both within the same expiration cycle. By doing so, the trader can benefit from a moderate downward move in the stock, while controlling the cost and risk of the trade.

Trade Setup

- Buy a $85 strike put (in-the-money, ITM) for $7.00

- Sell a $70 strike put (out-of-the-money, OTM) for $1.50

- Net Debit: $7.00 (buying the $85 put) - $1.50 (selling the $70 put) = $5.50

Potential Outcomes

- Maximum Loss: The maximum loss is the net debit paid to enter the trade, which is $5.50. This occurs if ABC stock is at or above $85 at expiration, and both puts expire worthless.

- Maximum Gain: The maximum gain is the difference between the strike prices minus the net debit paid. In this case, the difference between the strikes is $15 ($85 - $70). Subtract the $5.50 paid for the spread, and the maximum gain is $9.50. This occurs if ABC stock is at or below $70 at expiration.

- Breakeven: The breakeven price at expiration is the higher strike price ($85) minus the net debit paid ($5.50). Therefore, the breakeven is $79.50 ($85 - $5.50).

How Do You Close a Vertical Debit Spread?

To close a vertical debit spread, you execute the opposite of the original trade, using the same number of contracts. This involves selling the long option (the one you bought) and buying back the short option (the one you sold), both within the same expiration cycle.

Example

- Original Trade: Buy 1 contract of the $85 strike put for $7.00, sell 1 contract of the $70 strike put for $1.50 (net debit = $5.50).

- To Close: Sell 1 contract of the $85 strike put and buy 1 contract of the $70 strike put. The price you receive for selling the long put and the cost to buy back the short put will determine your profit or loss.

tastylive Approach

For both put and call vertical debit spreads, our setup preference is the same. Ideally we purchase an ITM option and sell an ATM/OTM option against it to reduce the cost basis of our long option.

To make sure we have a surplus of extrinsic value, the short option must have more extrinsic value than the long option. If we achieve this, our breakeven will be better than the stock price for the spread.

For call debit spreads, that means the breakeven will be below the stock price. This means we have some wiggle room to the downside if our bullish assumption is wrong. For put debit spreads, that means the breakeven will be above the stock price. This means we have some wiggle room to the upside if our bearish assumption is wrong.

In both cases, a breakeven improvement from the current stock price translates to a trade that has a higher than 50% probability of profit.

This creates a higher probability of profit, but does not guarantee profit as you still need a moderate move in your favor with the stock price to see substantial profitability. If both options start OTM, the cost of the trade will be lower, and the max profit will be higher. The trade-off here is that you have a lower probability trade, as you now need the stock to move even more to reach your breakeven price.

Vertical Debit Spread vs. Vertical Credit Spread: What is the Difference?

A debit vertical spread is typically initiated by a trader who has a strong directional view on the market. They expect the underlying asset to move significantly in a particular direction—up for a call debit spread, or down for a put debit spread—within a defined time frame. In both cases, the trader is willing to pay a net premium upfront because he/she believes that the price movement will be large enough to not only cover the cost of the spread, but also to produce a profit.

In contrast, a credit vertical spread is usually initiated by traders with a more neutral directional view. In these cases, the trader typically expects the price of the underlying asset to stay within a specific range. By selling an option that’s ITM, and buying an OTM option, the trader receives a premium for entering the position. This premium represents the potential profit, which is realized if the underlying asset remains range-bound, and the options expire worthless.

Vertical spreads can exhibit similar risk profiles, like an ITM call debit spread, and an OTM put credit spread. In these cases, we always opt for the strategy that has better liquidity and more narrow bid-ask spreads, which typically aligns with OTM strikes.

In summary, the decision to initiate a debit vertical spread typically stems from a belief that the market will experience a significant price movement in a specific direction, while a credit vertical spread is often employed when the trader expects the market to remain within a certain range. The difference lies in the trader’s view of volatility and price movement, as well as their approach to managing risk and reward.

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2025 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.